Only Question for Erdogan Is Which Economic Taboo to Break

Only Question Left for Erdogan Is Which Economic Taboo to Break

(Bloomberg) -- Ideas that a few months ago would have seemed anathema to President Recep Tayyip Erdogan are gaining traction as Turkey runs dangerously low on foreign-currency reserves and its economy succumbs to a recession amid the coronavirus pandemic.

A pro-government newspaper has broached the possibility of borrowing from the International Monetary Fund, helping give legitimacy to what officials have long publicly regarded as a non-starter. When asked Thursday how the IMF might assist Turkey, the fund’s chief said the institution has “a very constructive engagement” with it. The lira climbed sharply against the dollar.

And despite Turkey’s history of runaway inflation, economists have mentioned the option of printing money to help shoulder the burden of the stimulus needed to prop up growth. It’s a path that looks more tenable now that the central bank is soaking up sovereign bonds from the secondary market and saying it could scale up the size of such operations if necessary.

The stigma that both such choices once carried may be fading after Turkey emptied much of its arsenal of options. And as the deepest peacetime recession since the 1930s takes hold of the global economy, it’s forcing policy makers around the world to bend rules in ways once almost unthinkable.

“Ankara needs to figure out a way of bailing out the economy without causing a balance-of-payments crisis,” Global Source Partners economists including Murat Ucer in Istanbul said in a report. “And because this is so difficult to do on its own, the only practical solution, normatively speaking, is an IMF program -- no matter how unrealistic the politics of it may sound.”

Besides turning to the IMF, another option for Turkey could be to impose capital controls, according to Per Hammarlund, chief emerging-markets strategist at SEB AB in Stockholm, who says the government is more likely to seek bilateral support from the U.S., China or the European Union to restore confidence.

Erdogan on Wednesday spoke with Chinese President Xi Jinping, who promised to assist Turkey in its fight against the pandemic, according to a Xinhua report.

Capital Controls?

“Capital controls are a double-edged sword as they also keep sorely needed capital out of the country,” Hammarlund said. Turkish officials have in the past given assurances that capital controls weren’t an option even when they struggled to stabilize the currency.

The cost of doing nothing may be far too expensive. Should authorities drain reserves so much they could no longer defend the lira, Turkey would be at risk of a depreciation that might especially damage companies dependent on external financing, said Henrik Gullberg, a macro strategist at Coex Partners Ltd in London.

Turkey’s impasse is largely of its own doing. Erdogan’s drive for ever-lower borrowing costs eroded Turks’ confidence in their own currency, fueling a steady dollarization of the economy.

Meanwhile a slew of measures designed to penalize hedging against or betting on currency losses scared away international capital, while state banks have continued to prop up the lira by selling dollars. Foreign outflows from bonds and stocks reached $6.4 billion in the first three months of the year, a record quarterly amount in data going back to 2005.

People with direct knowledge of the matter said Turkish officials haven’t yet reached out to the IMF with any request for help, either under an emergency aid program available to cope with the virus outbreak or by way of talks on a larger loan that would require a stand-by agreement.

“We have a very constructive engagement with the whole membership, including Turkey,” the fund’s managing director, Kristalina Georgieva, said Thursday in a Bloomberg Television interview.

“We have been consulting all our members in this crisis on what are the policy actions that can help steer the economies through this very difficult time. In this virtual spring meeting that’s coming just next week, we will continue this constructive engagement with the membership, including with Turkey,” she said.

Policy makers in Turkey see no need for an IMF deal even though they consider now to be a time when they could get away with striking such an agreement, according to one of the people, who is familiar with Erdogan’s deliberations on the economy.

Building Bridges

Still, signs abound that policy makers in Ankara are laying the groundwork to secure some lifeline. Last month, Turkey officially asked the Fed to include the nation’s central bank in its dollar swap lines, people familiar with the decision said.

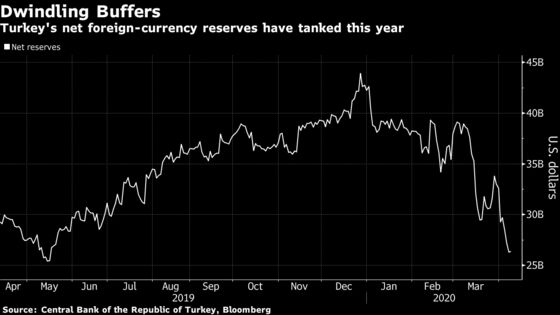

The issue has taken on more urgency after the nation’s central bank depleted its holdings. Gross reserves have dropped by almost $11 billion since the beginning of the year to $94.5 billion. Stripping out banks’ required reserves and other liabilities, the stockpile stood at only $26.3 billion as of Tuesday. According to the latest official data in February, $25.9 billion of the total was borrowed money.

When short-terms swaps conducted through the end of March are added, the net figure falls below zero, according to Bloomberg calculations.

And with no recourse to the Fed’s funding lines, it lacks the firepower to shield an economy that has more than $170 billion of external debt coming due over the next year. At the same time, the government might need to borrow more as it runs a wider budget deficit amid the health emergency.

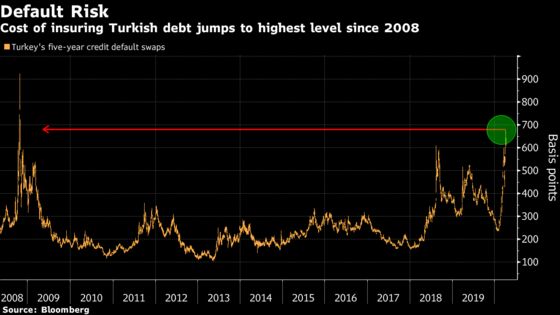

In a sign of heightened investor unease, the cost of insuring Turkish debt against a default has spiked, touching the highest level since 2008 on Monday.

Turkey’s advantage is its relatively low public debt burden. Lutz Roehmeyer, the Berlin-based chief investment officer at Capitulum Asset Management GmbH, says that’s among reasons why the government doesn’t need financial assistance at the current stage.

The last time the IMF bailed out Turkey in 2001, the financial crisis at the time wiped out a whole generation of Turkey’s political leaders and paved the way for Erdogan’s ascent to power.

The strings attached to any IMF package would likely put an end to the president’s growth-at-all-costs-approach to running the economy. Yet time could be running out, with hundreds of thousands of businesses already shut down because of the outbreak and the fate of the country’s $34.5 billion tourism industry at stake.

Timothy Ash, a strategist at Bluebay Asset Management in London, said he’s “wondering if -- against the cover of Covid-19 -- the hurdle to putting in a call to the IMF would be that high this time around?”

©2020 Bloomberg L.P.