(Bloomberg Opinion) -- Long before the Federal Reserve signaled interest-rate cuts were coming, China’s central bank was busy fiddling with an intricate dashboard of monetary-policy dials to boost growth.

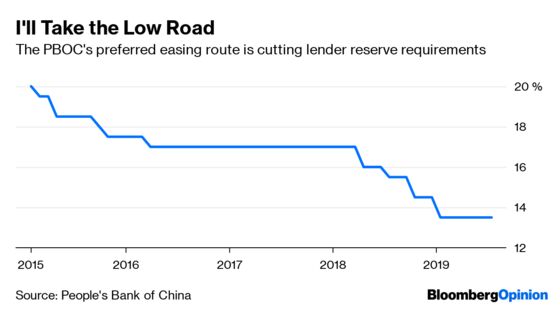

In 2018, the People’s Bank of China started cutting the amount of money banks are required to hold, and has been carefully adding liquidity to the system to encourage lending. Beijing has also turned to fiscal policy, lowering taxes and introducing an array of stimulus measures to encourage consumers.

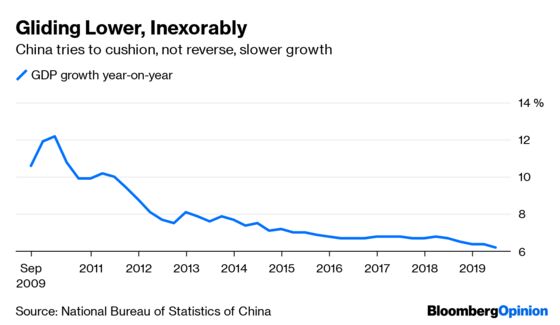

Hangovers from past efforts to juice activity explain China’s cautious calibration. The last thing officials want is a gush of liquidity that inflates asset prices. This easing is aimed at cushioning the slowdown, not reversing it. Few in Beijing are looking to replicate the glory days of double-digit growth rates notched in the early 2000s.

Now that the Fed has pivoted, China’s stance looks downright conservative relative to peers in developed and emerging economies. Central banks from Manila to Moscow have cut interest rates this year; the Fed and the European Central Bank have hinted more are coming.

Whether China will respond by cutting its benchmark lending rate remains an open question. With a deep policy toolkit, officials tend not to rely on the one-year lending rate to boost growth. But even with other options at hand, Beijing would be smart to stick to its measured approach.

Opening the stimulus floodgates just a crack shows that China recognizes its larger, older and less-export dominated economy is here to stay. Quarterly GDP numbers are more likely to begin with a 5 in the next few years, than the 6 of the past few or 7 from earlier this decade. In the second quarter, the clip was 6.2% compared with a year earlier, the slowest in almost three decades. The gradual, inexorable downward slope will continue.

There's a wistfulness in the portrayal of China's current economic numbers that suggests everything since the 15% growth of early 2007 is a failure. It's easy to forget that the big demand many people had of China back then was that it “rebalance.” In other words, focus less on rapid growth, nurture consumer spending and watch the pile of debt. Sound familiar?

China has done all of that, and underpinned the global economy as its own slice of that pie has increased. Among large economies, it sounded a growth alarm when few were listening. The country is still wrestling with the legacy of largess unleashed after the global financial crisis, which buttressed domestic and global activity, but left the country with an overhang of debt.

After lagging the PBOC, the Fed is now poised to exceed the easing efforts of its Chinese counterpart. There's little doubt among most Fed watchers that a couple of U.S. rate reductions are on the way, driven by what Fed Chairman Jerome Powell says is a desire to prolong the American expansion. The main risk the Fed has identified to that 10-year growth run isn't uniquely domestic; rather concerns about trade and risks to global growth (read: China and Europe) have deepened.

The credit for any bounce in the global activity will probably go to the Fed. After all, the dollar remains the dominant global currency. Yet it would be a mistake to overlook the maturing role of China’s central bank. Both institutions are ultimately interested in the same thing: a durable upswing supported by – and benefiting – China and America.

While a global central bank is implausible, prospects for world growth are best when the biggest monetary authorities pull in the one direction. In this instance, China got there first.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Daniel Moss is a Bloomberg Opinion columnist covering Asian economies. Previously he was executive editor of Bloomberg News for global economics, and has led teams in Asia, Europe and North America.

©2019 Bloomberg L.P.