One Lousy Treasury Bond Auction Doesn’t Say Anything

One Lousy Treasury Bond Auction Doesn’t Say Anything

(Bloomberg Opinion) -- The U.S. Treasury Department sold $27 billion of 10-year notes on Wednesday, and by one important metric, it drew the lowest demand in a decade. Some called the results “stunningly weak.” Others claimed that buyers stepping back validated JPMorgan Chase & Co. Chief Executive Officer Jamie Dimon’s observation that yields are “extraordinarily low.”

I’m here to tell you that practically none of it matters. At all.

Sure, the bid-to-cover ratio, which gauges demand by comparing the amount of bonds that were bid on with the amount offered, came in at 2.17. There’s no way to spin that as a good number, but it’s also hardly an outlier. The auction three months ago had a middling 2.35 ratio, and back-to-back sales in August and September 2017 came in at 2.23 and 2.28, respectively. Those latter results are arguably worse than this week’s deal when considering that the September 2017 auction was a mere $20 billion in size. That means Wednesday’s enlarged 10-year auction drew about $13 billion more in demand.

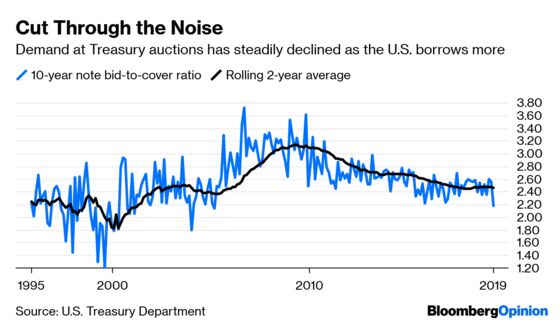

What’s more, the $15.9 trillion Treasuries market has faced progressively lower auction appetite for years now. To understand this trend isn’t any more complicated than the obvious arithmetic: The U.S. is borrowing more to finance widening budget deficits and investors aren’t proportionately upping their bids. A chart of the two-year rolling average of the bid-to-cover ratio tells the tale. By that measure, demand is about the weakest since shortly after the financial crisis:

A year ago, after a poor 10-year sale (and, coincidentally, amid a fresh round of tariffs), I took a deep dive into demand and pressed traders and strategists for insights into how to react to the auction figures. The answer I got back was near-unanimous: You can’t.

But for bond traders, the day-to-day implications are less clear. Take last month’s 10-year auction. Demand was the ninth-lowest since the start of 2009. In all the instances it was lower, yields fell four times and rose four times in the following month. Sometimes, Treasuries rallied into the offering; on other occasions, they were in the midst of a sell-off.

That’s why some strategists are reluctant to draw any grand conclusions from the upcoming slate of auctions, particularly as investors try to assess the fallout from the latest round of tariffs imposed by President Donald Trump.

“The auction stats that come out immediately after auctions are really a referendum on how well the market is pricing in the risk and the concession built in,” said Blake Gwinn, strategist at NatWest Markets. “As far as the longer-term trend in yields, can you look at a strong auction and say clearly we’re in a bullish market? I don’t know I’d ever really go that far.”

At the time of Wednesday’s auction, financial markets didn’t have a firm read on whether the U.S. and China would reach a trade deal, which explains why 10-year yields were little changed. With rates some 15 basis points below their 2019 average, it’s understandable why investors would be leery to step in and bid aggressively given the uncertainty. Plus, the Treasury had competition: Bristol-Myers Squibb Co. issued $19 billion of debt on Tuesday, and International Business Machines Corp. borrowed $20 billion on Wednesday. Those were two of the 11 largest U.S. corporate-bond sales in history. Domestic buyers, after all, are the ones who have stepped up in recent years to finance America's budget deficits. And they may have simply been running low on cash.

The setup for Thursday’s 30-year bond sale was more of the same, with Trump announcing minutes beforehand that he had received a “beautiful letter” from Chinese President Xi Jinping and that the two leaders would probably speak by phone. “I think it’ll be a very strong day,” he said, though “our alternative is an excellent one.” Yields quickly moved to little changed on the session. The auction wound up drawing decidedly average interest.

As for linking the weak demand to comments from Dimon, well, remember he said 5% 10-year yields were “a higher probability than most people think” back in August, and they never came close. But more to the point, it’s not as if low yields have stopped investors from bidding aggressively before. In June 2016, just a month before yields reached their all-time lows, the bid-to-cover ratio was 2.7, a level that hasn’t been reached since. The last time the ratio was above 3 was in March 2013, just months before the so-called taper tantrum and when yields were a paltry 2.03%.

Ultimately, the only way to read anything into auction results is by understanding both longer-term expectations and looking at how the market moved leading into the sale. If bond traders are convinced that growth will slow and yields will stay persistently low (like mid-2016), they’ll bid no matter the price. However, if yields move sharply lower in short order on some sort of fleeting shock — say, North Korea conducting a powerful nuclear test — that’s how you wind up with a result like in September 2017, which, again, could be considered even weaker than this week’s offering.

More often than not, though, one set of auction statistics says little about the path forward for the world’s biggest bond market. It’s fun to draw up conspiracy theories that the weak demand for 10-year notes reflected a no-show by China, the largest foreign holder of Treasuries. Even if that were somehow proven true, it provides little guidance because investors know that the country realistically can’t afford to entirely shun America’s debt.

If a U.S. auction ever failed, of course, that would be a big deal and raise questions about how the government overseeing the world’s largest economy would fund itself. But until that day comes (which could very well be never), traders need not sweat the small stuff in any given Treasury bond sale.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.