The Historic Oil Price Truce Won’t Last

The U.S.-Saudi-Russia deal on crude oil output will come under pressure when the world becomes a more normal place again.

(Bloomberg Opinion) -- After four days of high drama, low farce and long periods of tedium, the OPEC+ group of countries, led by Saudi Arabia and Russia, finally agreed to a record cut in their oil production in response to the coronavirus-triggered collapse in demand. But the deal will come under pressure when the world becomes a more normal place again.

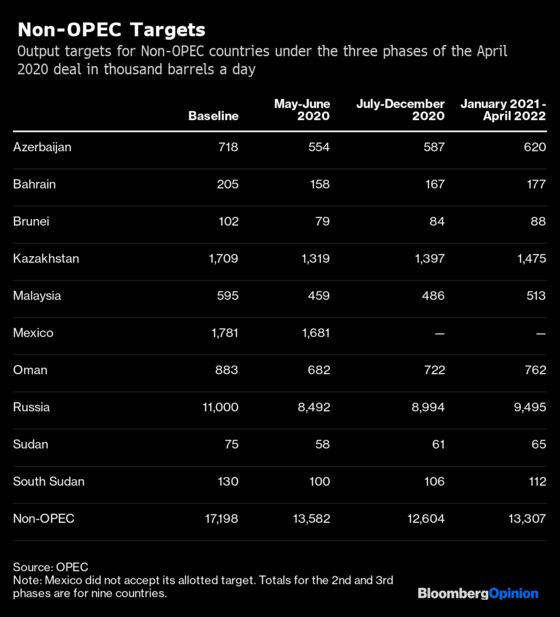

The drama was provided by Mexico refusing to accept its allotted cut. The farce followed when the country’s oil minister left the virtual OPEC+ meeting to hold separate talks with her U.S. and Canadian counterparts, while the other energy ministers agonized for hours, and then for days, over how to respond. The tedium? Well, that was just the bits in between.

Mexico was asked to cut 400,000 barrels a day of production in the first phase of an OPEC+ deal that would run for an unprecedented two years. It offered one-quarter of that, and from a slightly higher baseline than what was asked for.

An unlikely white knight appeared to ride to the group’s rescue on Friday in the form of U.S. President Donald Trump. He proposed an arrangement with Mexico’s President Andres Manuel Lopez Obrador (known as AMLO) in which 250,000 barrels a day of the “market-driven” decline in U.S. output would be rebranded as “Mexican.”

But don’t be fooled: That wouldn’t have taken a single additional barrel of oil off the market beyond those that would disappear anyway because of the Covid-19-prompted collapse in demand. Eventually, after nearly four days of trying to persuade the Mexican government to budge, the Saudis and the Russians finally decided to cut their losses and swallow Mexico’s lack of genuine commitment. The alternative would have been to allow the commodity markets to open on Monday morning with the group still in disarray and to risk another big price slump.

In fairness, the OPEC+ deal is historically grand in its scope, given the size of the cuts and their duration, although it’s questionable how much value there is in setting targets two years hence, when so much remains uncertain. The 20 producers taking part will initially cut output by 9.7 million barrels a day, with all but Mexico reducing production by 23% for two months — May and June. As it stands now, Mexico’s cuts will end with the first phase of the deal, when it will presumably have to leave the OPEC+ group. The reduction for the remaining 19 countries will taper to 7.7 million barrels a day until the end of the year, and then to 5.8 million barrels for another 16 months, until April 2022.

Don’t be surprised if the headline numbers published by OPEC+ are even bigger than these. There has been some suggestion that the official figure could be closer to 12.5 million barrels a day, but that would be achieved by raising the starting production numbers for Saudi Arabia, the United Arab Emirates and Kuwait, who have all boosted production this month, leaving their real targets unchanged. This is smoke and mirrors to try to make the cuts look even more substantial.

The deal raises some even bigger questions than Mexico. Russia, for example, is to cut its output by 2.5 million barrels a day over the next three weeks. Really? Igor Sechin, head of state-controlled oil company Rosneft, was a fierce critic of Russia’s modest contribution to previous reductions. I can imagine how he’ll react when he’s told his company has to cut output by almost 1 million barrels a day by May 1.

The contribution from Friday’s meeting of G-20 energy ministers — which followed Thursday’s marathon OPEC+ call — was, to put it mildly, underwhelming. India’s minister mentioned filling the country’s strategic oil reserve, but there were no concrete new offers from the group. With oil prices on the floor, building up reserves makes sense anyway, and China and India have already started. But storage space is limited.

The U.S. has room for another 77 million barrels in its Strategic Petroleum Reserve, but Congress refused last month to approve the budget for an initial 30-million-barrel purchase. Oil traders and analysts estimate that China could buy an extra 80 million to 100 million barrels this year. Meanwhile, the Indian government is asking state-run refiners to buy 15 million barrels of crude from Saudi Arabia, the United Arab Emirates and Iraq to fill its tanks. Beyond those three countries, there’s little storage capacity elsewhere.

U.S. Energy Secretary Dan Brouillette told the G-20 meeting that the oil market collapse will impose some 2 million barrels a day of American output cuts by the end of the year without any government intervention. Some predictive models, he added, see the drop as big as 3 million barrels. Russia previously rejected such “free market” cuts, arguing that production falling in response to a lack of demand is not an output reduction. But in the end it capitulated, along with the other OPEC+ countries. There was no mention in the OPEC+ communique of the deal being dependent on the actions of anyone else outside the group. Other non-OPEC+ producers, including Canada, Brazil and Norway have also contributed “market-driven” output cuts.

This is the second time in less than five years that Saudi Arabia’s attempt to pursue a pump-at-will policy has collapsed. After just one month, this one has lasted an even shorter time than the previous effort, brought to an end by the OPEC+ deal with Russia and other countries toward the end of 2016.

But these are quite clearly extraordinary times, with an unprecedented demand collapse. Don’t be surprised if the war over market share between the Saudis, the Russians and the Americans resumes once the lockdowns ease and people want oil again. This is a temporary truce rather than lasting peace between the three biggest producers.

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Julian Lee is an oil strategist for Bloomberg. Previously he worked as a senior analyst at the Centre for Global Energy Studies.

©2020 Bloomberg L.P.