Oil Collapse to Worsen China’s Deflation, Open Path for PBOC

Oil Collapse to Worsen China’s Deflation, Open Path for PBOC

(Bloomberg) -- The collapse in oil prices is set to worsen China’s factory deflation in the coming months, building pressure on the central bank to loosen monetary policy more decisively.

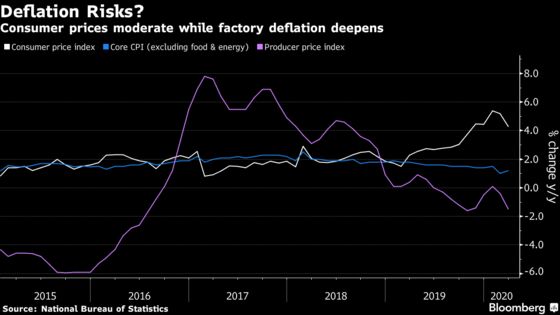

The most recent energy slump is another hit to companies already grappling with higher costs, broken supply chains, canceled orders and unwilling consumers. China’s factory-gate prices, which are a key inflation metric for the world economy, fell 1.5% in March, and could drop as much as 5% this quarter according to Shanghai brokerage Huabao Trust Co.

Crude oil is not part of China’s inflation baskets but it affects the prices of goods such as fuel, petrochemicals and packaging as well as transport costs. A previous spike in food prices and above-target consumer price gains has been a factor in the People’s Bank of China’s wariness about large-scale stimulus amid the downturn.

“Monetary policy will need to collaborate with fiscal policy to cushion the downward pressure in the economy, and interbank rates may continue to fall,” said George Wu, chief economist at Changjiang Securities Co. Ltd. in Beijing. “Producer price deflation will likely worsen in second quarter.”

The PBOC has cut short and medium-term rates recently on top of liquidity injections, loan rollovers and easier regulatory rules. The Politburo signaled last week that more of those moves will come to cushion the unprecedented economic downturn. At the same time, China’s stimulus efforts have stopped short of global peers or the debt-financed spending after the 2008 crisis.

Prices are one of the main factors the PBOC will look at when it decides whether to slash benchmark deposit rate, Liu Guoqiang, one of the central bank’s deputy governors, said earlier this month.

PBOC Watchers See Cautious Steps Despite Deepening Virus Impact

As the world’s largest crude oil importer, lower prices would normally benefit demand in China, especially from consumers. However, unless there is a strong pickup in the domestic economy, much of that dividend will be lost as consumers and companies aren’t spending.

The slump in prices is also hitting Chinese oil and gas producers, with PetroChina Co. looking to “dynamically optimize and adjust” its capital expenditure for 2020, it said last month. That will likely affect investment, jobs and spending, further damaging domestic demand.

What Bloomberg’s Economists Say..

“We expect the fiscal deficit to rise to 8-9% of GDP in 2020, up from 5% in 2019. We anticipate a further 30-40 basis points of rate cuts from the People’s Bank of China. In contrast with the 2008-9 stimulus, the focus will be on supporting jobs, not targeting a specific GDP growth figure”

-- Chang Shu, David Qu & Tom Orlik, Bloomberg Economics

For the full note click here

The PPI could drop about 4% for the year if oil prices stay between $20-$40 per barrel, according to Nie Wen, an economist at Huabao Trust Co. On Wednesday oil was trading at about $16 a barrel. “The situation China had a few years ago when deflation lasted dozens of months may happen again.”

China’s outsize role -- as the world’s largest exporter -- in the global inflation picture means that it‘s set to transmit a powerful deflationary impulse back through the world economy. China reports April inflation data on May 12.

Domestically, a faster fall in Chinese prices would hurt company profits and revenue, discouraging investment and hiring at a time when the government needs all sectors to quickly return to normal.

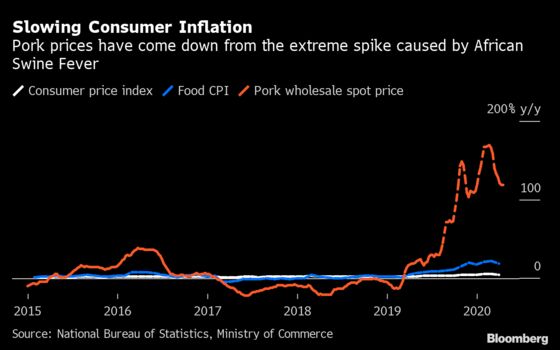

Pork prices have started falling in recent weeks, easing food inflation that has been squeezing Chinese households. Combined with cheaper oil, this will lessen concerns about the unintended effects of additional monetary easing.

Chinese consumers won’t see all the benefits of the decline in oil prices as the government keeps a floor at the equivalent of $40 a barrel for the benchmark Brent, Goldman Sachs Group Inc. economists wrote in a recent report.

“The European and U.S. economies are about to contract this year, and China’s stimulus will be no where close to its level in 2008 and 2009,” said Huabao’s Nie Wen. “Demand can’t grow significantly in such circumstances, then how could you expect producer prices to gain?”

©2020 Bloomberg L.P.

With assistance from Bloomberg