Forget Tantrums, Emerging Markets Are the Haven Now

(Bloomberg Opinion) -- Just as the Federal Reserve steadily picks up the pace of rate increases, Wall Street’s quantitative strategists are telling clients to sell U.S. stocks and buy into emerging markets.

U.S. central bankers are increasingly confident in their view of the economy. Of the Fed’s 16 voting members, 12 are advocating for one last rate increment this year, bringing the 2018 total to four. That compares with eight such votes in June. Policy is no longer “accommodative,” according to the latest statement.

So given the 2013 taper tantrum and the 1997 Asian financial crisis, it’s a bit surprising that Wall Street is turning bullish on emerging markets now.

The key is valuations. According to Credit Suisse’s HOLT, an accounting framework that sifts through more than 20,000 companies in 65 countries, the premium of developed markets over their emerging counterparts is at a historical peak. This year, the S&P 500 Index has pursued its record bull run, outperforming the benchmark MSCI Emerging Markets Index by almost 18 percentage points.

Many on Wall Street worry that the American market is too expensive. Since 1981, the S&P 500’s cyclically adjusted price-to-earnings, or CAPE, ratio has been higher only once, as my colleague Nir Kaissar wrote, and that was at the peak of the dot-com bubble.

Valuations aside, many — this columnist included — just don’t believe the U.S. can remain immune from the fallout of a global trade war while the rest of the world suffers. Sooner or later, American shoppers will feel the pinch: Almost one-quarter of the $200 billion Chinese products subject to higher tariffs are consumer goods.

Beyond the immediate outlook, even Fed board members are divided on what the economy will look like in 2020. Of the voters, nine see at least one rate increase then. Three reckon the central bank will have to revert to easing that year.

So if you believe the decoupling of U.S. and emerging markets can’t last, “The time for the rotation may be now,” JPMorgan’s quant strategists said in a recent note. Stock markets tend to anticipate economic performance by six to 12 months.

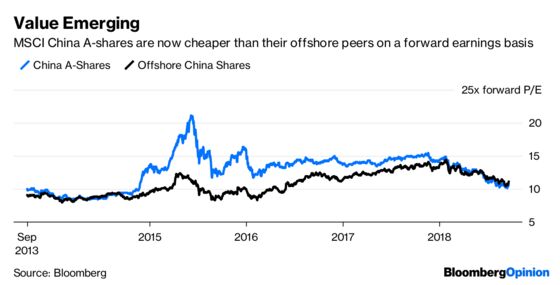

Already, through the trading link with the Hong Kong exchange alone, global investors have bought a net $29 billion of Chinese stocks this year. The nation’s A-shares are at their cheapest levels since 2014.

As I’ve argued, EM stocks can’t rally unless their nations’ currencies stabilize first. In emerging Asia, at least, the grownups seem to be in charge. Indonesia, suffering from a widening current-account deficit, and the Philippines, beset by inflation, have both boosted interest rates by 1.5 percentage points this year, with the latest increments announced Thursday.

China, meanwhile, with a 30 percent weighting in the MSCI Emerging Markets Index, isn’t blindly following in the Fed’s footsteps. Its central bank has left the door open to monetary easing to lift the economy as trade sanctions bite.

You could even say a mini-taper tantrum has already happened. Hedge funds have been selling steadily out of MSCI Emerging Markets futures this year, unwinding all the buying they did since mid-2016.

There are two ways for these markets to get back in the same orbit: Either through an EM rally or an American correction. Either way, emerging markets look like the safer place to be.

To contact the editor responsible for this story: Paul Sillitoe at psillitoe@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2018 Bloomberg L.P.