Next China: Shadow Boxing

China faces a long list of economic challenges, among the trickiest of which is shadow banking.

(Bloomberg) -- Want to receive this post in your inbox every Friday? Sign up here.

China faces a long list of economic challenges, among the trickiest of which is shadow banking.

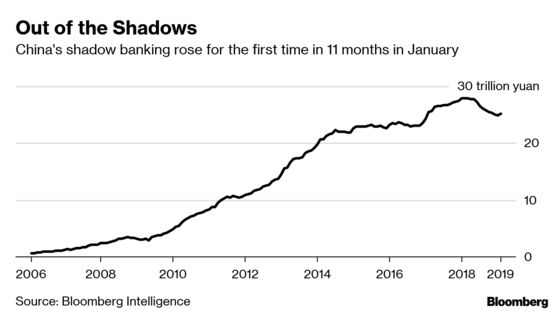

This catch-all phrase encompasses several forms of lightly regulated lending, many of which came about specifically to avoid oversight. But at an estimated $9 trillion, it's become hard to miss.

Shadow banking isn't all bad. It's a crucial source of financing for the country's private sector, which employs 80 percent of urban workers, thanks to a banking system that's gravitated towards state-owned enterprises. And that's what's tricky.

For policy makers, the perils are clear. It emerged this week, for example, that China Merchants Bank funneled about $400 million from a shadow-banking product into the purchase of a European sports company that's since imploded. China Merchants Bank was part of a consortium that paid $1 billion for a 65 percent stake in MP & Silva in 2016, only to see the company dissolved two years later.

Then there's peer-to-peer lending. Defaults by these companies, which allow individuals to lend money directly to borrowers, have wiped out the savings of families across China. Some have staged protests to get their money back, sparking concerns about social stability.

Addressing these risks is not pain free. China last year engineered the country's most-substantial shrinking of shadow banking on record and the subsequent tightening of financial conditions dragged economic growth to the slowest in a decade. So it was not surprising when financial markets rallied this week after central bank data for January showed the first increase in shadow banking in 11 months.

It's a tough bind. Authorities could ease up on their campaign but at the risk that any delay in dealing with shadow banking could invite calamity later on. Though at some point, if growth slows too much, the need to avert a sharp deceleration will outweigh concerns of future crisis.

And Trade

Chinese and U.S. negotiators continued talks in Washington this week aimed at either hammering out a deal before the March 1 deadline, when American tariffs rise to 25 percent, or extending the deadline. An extension looks increasingly likely, with President Donald Trump saying March 1 is not a "magical date." A tentative agreement for China to pledge to keep its currency stable was another sign that tariffs are unlikely to rise when the calendar flips to next month.

Tech Divide

The U.S.-China split in technology though seems to be widening. A disagreement between European and American telecom carriers on if Huawei equipment should be used in networks became public this week. New Zealand's prime minister, meanwhile, signaled Huawei might be allowed to be part of its 5G networks, and a senior Italian official dismissed U.S. warnings that the company's gear could facilitate spying. The U.K.'s cybersecurity chief also pointed out that shrinking the pool of suppliers by excluding Huawei is also not good for security.

Tax Man

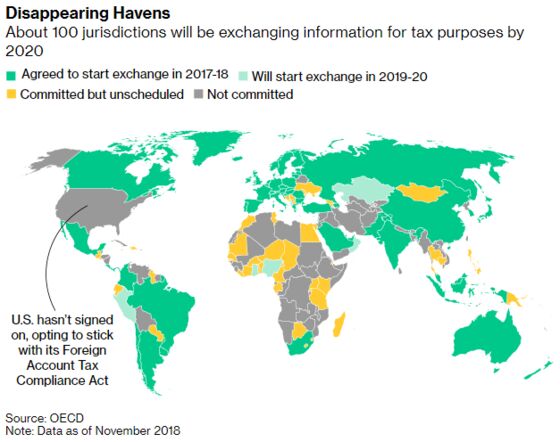

One issue that does unite governments is taxes and not letting people dodge them. China is no exception. Beijing has taken a number of steps recently to strengthen enforcement. That includes signing onto the Common Reporting Standard, a global financial disclosure system that facilitates information sharing between countries, thereby making it harder to stash cash overseas. Though even here there's divergence with the U.S., which has opted against the pact.

Greater Bay

China unveiled a grand plan this week to more closely integrate the cities of Hong Kong and Macau with neighboring Guangdong province. The potential benefits are large. HSBC says it could create a trillion-dollar regional economy that exports more than Japan. But there are also plenty of concerns. Chief among those is worry that the plan will further erode the "one country, two systems" framework that's allowed Hong Kong to maintain separate legal, monetary and political systems.

Family Feud

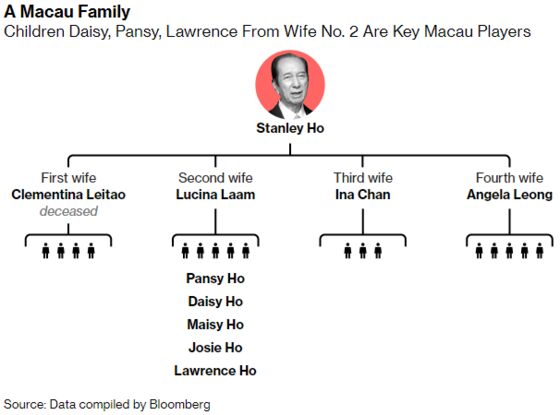

And finally, a family dispute has put a spotlight on one of Asia's most-storied business empires. Stanley Ho built Macau's first casino in 1962 and held a monopoly on gaming in the city for the next four decades. Along the way, he married four women and fathered 17 children. But with Ho now 97, different branches of his sprawling family are vying for control. Looming over this feud though is next year's review of the company's gaming license and questions about if the family will be able to solve its problems in time to avert disaster.

To contact the editor responsible for this story: Malcolm Scott at mscott23@bloomberg.net

©2019 Bloomberg L.P.

With assistance from Bloomberg