New Era of Bond-Market Volatility Begins as Fed Fights Inflation

The hottest rate of inflation in four decades has ushered in a wilder era of bond-market volatility.

(Bloomberg) -- The hottest rate of inflation in four decades has ushered in a wilder era of bond-market volatility, causing investors to shop for hedges to protect their portfolios.

Bouts of Treasury volatility tend to erupt when hawkish shifts in central bank policy loom over the market. That has already started after Federal Reserve Chairman Jerome Powell said he was retiring the word “transitory” in describing inflation, helping send an index of expected swings in Treasuries to a 20-month high. The central bank’s final meeting of the year on Wednesday could set the stage for a more sustained period of turbulence should policy makers indicate a faster and longer period of monetary tightening is required to tame consumer prices.

“Fed meetings are going to be fun again, starting this week,” said Kevin Flanagan, head of fixed-income strategy at WisdomTree Investments. “They have put an increased pace of tapering on the table and the question for next year is what else is coming.”

As a result, many fund managers are bracing for the end of what was a quiet era of bond-market swings, excluding the drama at the start of the pandemic in 2020. They’re adding hedges to their portfolios in the form of floating rate Treasury notes, Treasury inflation-protected securities and cheap options. Complicating matters, the risks are two-way: Volatility could easily spread from the bond market to equities and other asset classes, tightening financial conditions and causing the Fed to have a change of heart.

In the past, Powell has telegraphed a deliberate pace of policy decisions and sought to contain market volatility. That may well play out again as the central bank reduces its asset purchases and lays the groundwork for rate increases next year. Still, Flanagan said there is a risk that elevated inflation and a hotter economy compel a faster pace of tightening than what’s expected. In terms of protecting portfolios, Flanagan said “owning floating rate Treasury notes is a way to follow the Fed.”

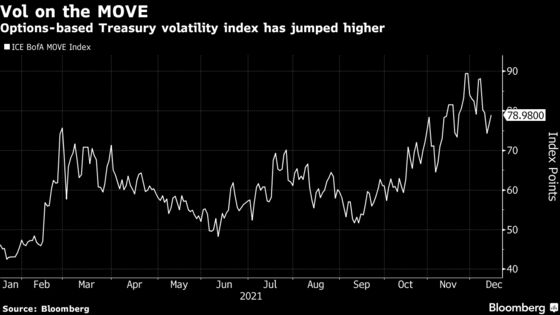

The risk of a more aggressive tightening course already has ignited turbulent trading conditions in the $22 trillion Treasury bond market. The MOVE Index, a closely watched proxy of expected Treasury volatility, spiked to a 20-month high reading of almost 90 at the end of November, and currently sits at about 79 -- well above its past decade’s average of 65.

“There is a wide dispersion of outcomes if they have to fight inflation,” said Bob Miller, head of Americas fundamental fixed income at BlackRock. “If the Fed adopts a fighting inflation stance, volatility stays high with the risk of short-circuiting another two years of solid growth for the economy.”

It’s not just fixed-income investors who are concerned. Greater bond-market volatility has significant consequences for all investors. Low nominal Treasury yields and negative inflation-adjusted real yields fueled a boom in equities and other speculative assets, sending measures of U.S. stock-market valuations to near the most-expensive levels since the dot-com bubble. A policy mistake by central bankers trying to tame inflation is the biggest downside risk for global stocks next year, according to an informal Bloomberg News survey of fund managers.

Kathryn Kaminski at AlphaSimplex Group said the biggest change her firm has been following is a transition away from a classic long-stocks, long-bonds strategy that works in a deflationary environment.

“One of the things people often forget -- which is one reason I think there’s going to be more volatility -- is that bonds behave very differently in an inflationary environment than they do in an deflationary environment,” said Kaminski, a portfolio manager and chief research strategist at the firm, which manages about $6.4 billion. “Bond volatility was much higher in the 1970s when inflation was much higher. And on average, stock-bond correlations were positive during the inflationary environment of the 1970s.”

The central bank’s renewed focus on consumer prices already has prompted a sharp decline in bond-market inflation expectations, with the 30-year yield trading at its lowest level since early January. Yet, not everyone’s convinced that such signals can be trusted. Some believe inflation will continue running above the Fed’s target of 2% as the pandemic era’s massive fiscal and monetary support overshadow not only the Fed’s tightening but also longstanding deflationary forces such as high debt levels, productivity boosted by technology and an aging population amassing more savings.

That has firms like Pacific Investment Management Co. modestly overweight TIPS because the securities are not fully pricing in an appropriate inflation risk premium should stimulus keep the economy motoring along next year, according to PIMCO’s latest asset allocation outlook.

Ultimately, the Fed may find itself in a quandary: Continue to fight inflation, or be forced to respond to the wrath of financial markets reacting to the economic headwinds created by higher rates. In the past three tightening cycles, the Fed tied itself to financial conditions and sought to limit bond volatility and prevent a spillover to other asset classes. Most recently, in late 2018, it was forced to end rate hikes once equities and credit fell sharply.

“A tail risk for 2022 is one of inflation proving stickier than expected and the Fed tightens financial conditions and accepts a slower economy,” said Gene Tannuzzo, global head of fixed income at Columbia Threadneedle. “The Fed will allow more volatility until financial conditions become too tight.”

The prospect of the Fed fighting a more entrenched level of inflation while also seeking to manage the fallout from broader financial markets only adds to the ingredients that could lead to spikes in volatility.

“Going forward, the Fed will have to just keep stepping back in,” said Vineer Bhansali, the founder of hedge fund LongTail Alpha. “There will be these fits and starts and they just have to step in more and more frequently to stabilize inflation and markets,” he said. “Inflation is just here, so you have to get used to it. That’s all extremely positive for volatility to keep increasing and you have to protect yourself.”

©2021 Bloomberg L.P.