Near-Disaster in U.S. Treasuries Lights a Fresh Fire for Reform

To prevent another flareup, Fed officials this week -- have raised the possibility of shoring up the market’s foundation.

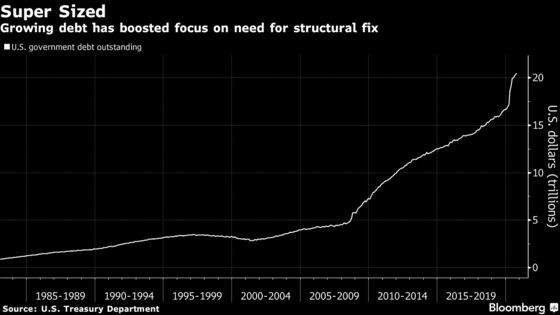

(Bloomberg) -- The U.S. Treasury market’s brush with disaster in March has reawakened calls to overhaul the underpinnings of the almost-$21 trillion cornerstone of the global economy and ease pressure on the Federal Reserve to step in with massive lifelines.

Bond liquidity vanished nine months ago as investors panicked about the pandemic and stopped trading, forcing the central bank to pick up the slack and buy debt at an unprecedented speed and scale to get the business functioning smoothly again.

To prevent another flareup, Fed officials -- including Chairman Jerome Powell this week -- have raised the possibility of shoring up the market’s foundation with a broad-based central clearinghouse to back up trades and handle surges in activity in times of stress.

A revamp could eliminate a source of criticism aimed at the Fed: that by backstopping the bond market in March, it helped bail out a leveraged trade popular with hedge funds. A central clearinghouse that handles more if not all Treasuries trades, supported by capital supplied by its members, could’ve removed the need for such dramatic Fed action.

Only about a fifth of the market goes through Fixed Income Clearing Corp., the only central clearinghouse in Treasuries. The dwindling role of banks and proliferation of electronic traders has diminished FICC’s role. That’s led to widespread fear that the Treasury market is too opaque and its risks too hard to grasp given that clearing and settlement methods vary so much.

“Central clearing is a reform that could be very useful to the Treasury market’s functioning,” said Darrell Duffie, a finance professor at Stanford University. “Dealers just cannot handle the demands for liquidity anymore. And while these extreme events have happened only once in a while, they will become a more regular occurrence if nothing is changed because the market is growing exponentially.”

There’s a lot at stake in getting the reforms right. The Congressional Budget Office projects outstanding Treasury debt will swell about $10 trillion in the next decade.

And Treasuries are the standard that helps determine the risk and price of everything from home mortgages to corporate bonds, and are the primary safe haven for global investors in times of turmoil. That special status could be put in question if there are more moments when they’re extremely hard to trade. U.S. taxpayers could even be affected if ultimately investors demand extra compensation to own the debt.

In finance, clearinghouses handle the settling of trades among market participants. A CCP, as they are often known, effectively acts as the buyer for every seller and vice versa, thus reducing systemic risk by eliminating the chance that if the firm on one side of a trade fails, the other side takes a hit. They act as a firewall by collecting money to back every trade, so there’s capital to pay off losses.

In U.S. stocks and many derivatives, every trade is processed in one, keeping the market stable by ensuring all consummated deals actually get completed. But not in Treasuries -- which foments fear during tumult -- even though that market is arguably more crucial to global finance since it steers borrowing costs for millions of home buyers, companies and governments around the world.

While the Treasury market is again functioning normally and the catalyst for the disruption, the pandemic, was a once-in-a-century event, the liquidity breakdown in March was the second of its kind in less than a decade. The need to broaden central clearing was also voiced after the Oct. 15, 2014, “flash rally” during which Treasury prices rapidly jumped and then plunged for no apparent reason. But no clearing changes have been rolled out since then.

Since the episode in March, Fed officials including Vice Chair for Supervision Randal Quarles and Governor Lael Brainard have publicly pointed to a clearing overhaul as a possible solution.

March was a wake-up call that structural adjustments may be needed, Quarles said in October. “There certainly would be benefits to -- in a period of stress and in regular times -- improving the functioning of the Treasury market,” he told the Managed Funds Association. “There are a lot of ideas out there,” including central clearing, which he called “very worthy.”

Brainard in November cited “wider use of central clearing” as a reform that should be considered.

Powell raised the issue this week. “We need to be thoughtful about the structure of the Treasury market and look at ways to make sure the capacity is there for it to be handled by the private sector,” he told reporters Wednesday. “There may be a central clearing angle that would, you know, net a lot of risk. That’s yet to be proven. There are a lot of things that are being looked at right now,” he said, adding that he didn’t see the solution being the Fed having a permanent role in the market.

The Fed’s intervention beginning in March was seen by some as a bailout for hedge funds, who had piled into highly leveraged Treasury trades. If no changes are made, this could encourage continued risky behavior since investors will know the Fed will save them. This moral hazard issue is an even more important reason to revamp the Treasury market to prevent an ongoing need for the Fed to jump in, Duffie said.

Under Joe Biden’s presidency, an overhaul might get more attention. During Barack Obama’s administration -- when Biden was vice president -- there was two years of work toward this by Treasury Secretary Jacob J. Lew. But there’s been no movement toward more central clearing under Steven Mnuchin’s leadership of the department, though there’s been progress on making the market more transparent.

Janet Yellen, the former Fed chair, may pick up the baton if she becomes Treasury Secretary given the last Democratic administration was more supportive about reforms.

While nobody questions the liquidity of benchmark Treasuries during normal times, since the global financial crisis it’s increasingly proved inadequate during times of distress. Post-2008 regulations have curtailed banks’ willingness to hold securities or add risk to their balance sheets.

“The fundamental problem of flowing everything through dealer balance sheets is just going to become more problematic over time,” said veteran bond-market analyst Lou Crandall of Wrightson ICAP.

High-frequency trading firms play a bigger role, but their Treasury orders often don’t clear through FICC. The majority of the over-$500 billion in daily trading of Treasuries is settled and cleared bilaterally, not at FICC, through a hodgepodge of entities including brokers themselves.

Given FICC has a head start with clearing between dealers and in some corners of the repurchase-agreement market, many see them as the most likely firm to undertake a broader central clearing initiative. Its parent, Depository Trust & Clearing Corp., already clears everything that trades in the U.S. stock market -- evidence that it can handle processing an entire asset class.

Not everyone views central clearing as needed or helpful. Chris Leonard, head of U.S. rates trading at Barclays Plc, says expanding it in the repurchase-agreement market hasn’t prevented issues there, so its ability to help the cash Treasuries business is “questionable.”

Even Quarles, who has spoken approvingly of broadening central clearing, isn’t confident it’ll completely eliminate the need for the Fed to backstop Treasuries sometimes. “I’m not sure that would have been the answer to what we saw in March and April,” when there was a mad dash for cash by investors, he said.

Reforming the market has proved an arduous task in the past as typically it’s pitted desires of Wall Street dealers against those of new participants such as automated traders. But what exists presently is a very fragmented structure for a market regulated in a patchwork fashion.

“Given the disparate interests and incentives of market participants, as well as disagreements about how the costs and benefits of central clearing would be apportioned, a move to central clearing would almost certainly require regulatory fiat,” said Ken Monahan, a senior analyst covering market structure and technology at research firm Greenwich Associates.

Upheaval has sparked change before. The 2008 crisis led to Basel III and the Dodd-Frank Act, which curtailed bank use of leverage and shored up their capital bases. The October 2014 dislocation triggered the first review of the market’s structure since 1998.

“The three building blocks needed for modernizing the Treasury market structure are public reporting, trading-venue oversight and central clearing. We can have a much more efficient and resilient marketplace if Treasury reform gets an appropriate level of attention over the coming years,” said Stephen Berger, global head of government and regulatory policy at Citadel LLC, Ken Griffin’s hedge fund. “If not, then ultimately the cost of issuance for the government will be higher than it should be.”

©2020 Bloomberg L.P.