Mnuchin Asked About Fed Option That Could Avoid Rate Hikes

Treasury Secretary privately asked bond dealers and investors in October whether they want U.S. Fed to tighten policy or avoid.

(Bloomberg) -- Treasury Secretary Steven Mnuchin privately asked bond dealers and investors in October whether they want the Federal Reserve to tighten monetary policy by raising interest rates or through faster cuts in its securities portfolio, six people familiar with the matter said.

Mnuchin’s question could be seen as suggesting a way for the central bank to accomplish its goal of preventing a strong economy from overheating without triggering the ire of President Donald Trump, who has blasted Fed Chairman Jerome Powell for raising rates. For his part, Mnuchin has refrained from commenting on monetary policy, citing the importance of the Fed’s independence.

In an Oct. 30 meeting with a Treasury advisory committee that makes recommendations to the government quarterly on its debt sales, Mnuchin asked which they favored -- an accelerated balance sheet run-down or further rate hikes -- if they had to choose one or the other, according to the six people, who asked not to be identified because the conversation was private. One of the people said that Mnuchin asked the question out of curiosity of what bond market participants thought of the two alternatives before the Fed.

The committee was split in response, two of the people said.

Mnuchin raised the question during a regularly scheduled quarterly meeting with the Treasury Borrowing Advisory Committee, or TBAC, which includes representatives from investment funds and banks. Its members include executives from Goldman Sachs Group Inc., Citadel LLC and JPMorgan Chase & Co.

The TBAC provides the secretary a chance to engage with bond market participants to help inform debt management plans, a Treasury spokesman said, declining to elaborate further.

Trump’s Nominee

Trump has broken with decades of precedent by commenting on Fed policy with repeated attacks on the central bank’s rate increases. He has also recently blamed Mnuchin for recommending Powell for the job, two people familiar with the president’s thinking said.

Still, Mnuchin hasn’t been the target of any direct, public criticism from Trump and, despite reports he may leave the Treasury Department as part of a broader Cabinet shakeup, is likely to stay in the administration for now, according to people familiar with the plans.

On Monday, Trump told the Wall Street Journal that “the Fed right now is a much bigger problem than China,” which is locked in a trade war with the U.S. He also seemed to widen his criticism of the Fed to include its ongoing balance-sheet reduction. “I don’t like what they’re doing,” the president said. “I don’t like the $50 billion.”

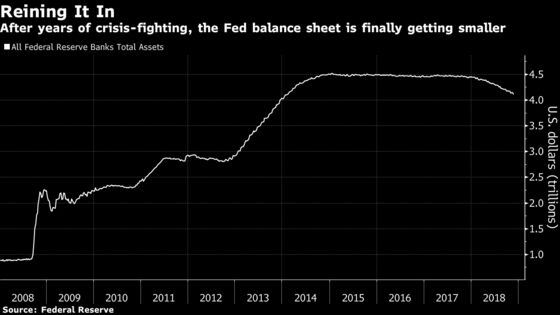

The Fed is currently reducing the bond holdings on its $4.1 trillion balance sheet by a maximum of $50 billion per month -- $30 billion of Treasuries and $20 billion of government agency debt and mortgage-backed securities.

Fed watchers voiced skepticism that the independent central bank would change its monetary strategy along the lines Mnuchin talked about, noting that Powell and his colleagues are much more comfortable altering interest rates to steer the economy than they are tinkering with the balance sheet. Fed officials have repeatedly said the target range for the federal funds rate -- not the balance sheet -- is their main tool for setting policy.

Any acceleration in the balance sheet unwind wouldn’t be without consequences for the Treasury either, given that part of the government’s increased debt sales to the public has been a result of the central bank’s waning purchases. The Fed buys Treasuries through non-competitive bids submitted alongside the government’s auctions. These Fed purchases, known as add-ons, do not affect the auction size. So any reduction in the Fed’s demand has to be made up in the auction to keep Treasury’s proceeds level.

Powell, whom Mnuchin meets regularly to discuss economic issues, has described gradual rate increases as an effort to strike a balance between tightening credit too much, thus triggering a recession, and not enough, subsequently spurring inflation and asset-price bubbles.

December FOMC

The central bank is widely expected to boost rates by another quarter percentage point next month. But the path in 2019 is less clear.

Powell himself laid out a scenario earlier this month for a pause in the rate hiking campaign sometime next year by highlighting potential headwinds to the U.S. economy.

The Fed in October 2017 began its program to methodically shrink its balance sheet by allowing some of the bonds it holds to mature without reinvesting the proceeds. It started off small, with bond drawdowns initially limited to $10 billion per month, and then gradually raised that to the current $50 billion maximum.

Paring the portfolio puts some upward pressure on long-term interest rates by adding to the supply of bonds that investors must absorb. It thus effectively tightens financial conditions and acts as a drag on economic growth, just as increases in short-term interest rates do.

But it’s much less visible and has attracted little attention outside of the financial markets since it was launched. Indeed, several Fed officials have said that their aim was to make the balance sheet unwind the equivalent of “watching paint dry.”

Powell told reporters in June that the program was “proceeding smoothly” and evinced little desire to change it. The balance sheet has shrunk $354 billion since the plan began. The chairman will deliver a speech on Wednesday to the Economic Club of New York.

--With assistance from Jennifer Jacobs.

To contact the reporters on this story: Rich Miller in Washington at rmiller28@bloomberg.net;Saleha Mohsin in Washington at smohsin2@bloomberg.net;Liz Capo McCormick in New York at emccormick7@bloomberg.net

To contact the editors responsible for this story: Brendan Murray at brmurray@bloomberg.net, Jenny Paris

©2018 Bloomberg L.P.