U.S. Recession Risk Creeps Higher Because of Weak Business Spending

Weak Corporate-Spending Appetite Boosts U.S. Recession Risk

(Bloomberg) -- Terms of Trade is a daily newsletter that untangles a world embroiled in trade wars. Sign up here.

American business is holding back on investment, and that’s holding back the economy.

After growing 5.9% last year, such corporate outlays -- including for equipment, software, commercial buildings, factories and mines -- have downshifted, laying economic growth prospects clearly at the feet of consumers. Household spending, which accounts for almost 70% of gross domestic product, didn’t skip a beat in the second quarter and is poised for another solid showing in the third.

Nonresidential investment, on the other hand, has slowed abruptly -- falling an annualized 0.6% in the second quarter, the weakest performance in three years, after a 4.4% gain in the prior period. With profitability moderating, global economies grasping for growth and the negative repercussions from antagonistic trade policies, companies have precious little appetite to ramp up expenditures on facilities and equipment.

That’s part of the reason Federal Reserve policy makers are forecast to cut interest rates Wednesday for a second-straight meeting. The central bank’s last two statements in June and July described business investment as “soft,” and spending may be poised to sag again in the third quarter. The New York Fed’s latest survey of manufacturers in the state, released Monday, showed the outlook for capital spending plunged by the most in three years.

Read more: New York Fed Factory Gauge Slumps

Economists surveyed by Bloomberg in September see a 35% chance of recession in the next 12 months.

While business investment makes up about 15% of GDP, small potatoes compared with households, consecutive quarterly declines are rare “outside of recessions or shortly after recessions,” JPMorgan Chase & Co. chief U.S. economist Michael Feroli said in a recent report.

“Profitability -- defined as the rate of return on invested capital -- has decreased in recent years,” Feroli wrote. “This likely has been a headwind to capex. Another more commonly-cited challenge for business investment is trade policy-related uncertainty, through it is harder to find a clear empirical link between trade policy and capital spending.”

For the past 50 years, he said, the nonfinancial corporate sector’s return on invested capital has mainly averaged 7.5% to 9.5%. “Over the last few years it has been moving toward the lower end of that range,” Feroli said.

Randall Stephenson, chief executive officer of telecom giant AT&T Inc., said the weakness in investment may eventually filter through to consumers.

“It shouldn’t be a surprise to anybody that business investment starts slowing down” amid trade tensions, Stephenson said at a Goldman Sachs investor conference Tuesday. “I don’t think we’re headed to a recession, but we’re definitely slowing down. And you can’t have that kind of slowdown in business investment and not find its way into the consumer, ultimately.”

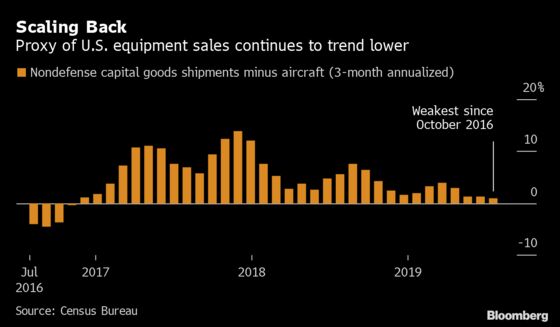

Monthly data on shipments of non-defense capital goods excluding aircraft, a proxy of business investment used by economists to shape quarterly GDP estimates, declined at the start of the third quarter after no change in June. In the three months through July, these shipments advanced at a tepid 0.9% annual rate -- the weakest performance since late 2016.

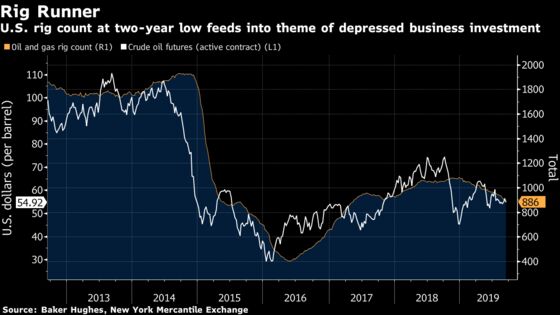

The energy sector is responsible for some of the weakness in investment. With oil prices still well below the October 2018 peak of $76, and inventories remaining elevated, exploration and production firms have been less than enthusiastic about drilling as investors demand capital discipline over production growth. The number of oil and gas rigs in the U.S. is at a two-year low, Baker Hughes data show.

Another reason for corporate hesitancy is bloated inventories. The ratio of the value of durable goods stockpiles relative to sales has been increasing. This could reflect companies’ accumulation of big-ticket items and manufacturing inputs ahead of tariffs, more restrained customer demand or a combination of both.

While American consumers remain the bedrock for the economy and show few signs of flagging, the investment retrenchment and corporate profitability concerns are making the U.S. more vulnerable to a recession.

--With assistance from Katia Dmitrieva.

To contact the reporter on this story: Vince Golle in Washington at vgolle@bloomberg.net

To contact the editors responsible for this story: Scott Lanman at slanman@bloomberg.net, Jeff Kearns

©2019 Bloomberg L.P.