Maybe Europe Can’t Recover From the Financial Crisis

Maybe Europe Can’t Recover From the Financial Crisis

(Bloomberg Opinion) -- If you read only one history of the global financial crisis and the turbulent decade that resulted, I recommend “Crashed: How a Decade of Financial Crises Changed the World,” by Columbia University historian Adam Tooze. Few authors are as capable of weaving together economics, policy and geopolitics into a coherent whole. Not only does Tooze cover every critical aspect of the crash in the U.S., but he offers deep insight into Europe’s slow-motion disaster.

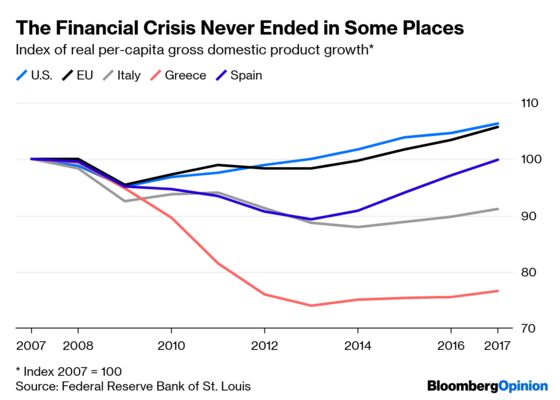

This importance of the latter is underappreciated. Although the crisis began in the U.S., the breakdown it triggered in Europe had graver consequences. A decade later, the economies of the U.S. and the European Union have both largely recovered, but some of the hardest-hit European countries — Greece, Italy and Spain — are not in such good shape:

The political fallout in Europe has also been long-lasting. Tooze probably overstates the impact of the crisis on the election of Donald Trump, which was more a function of long-festering racial and cultural conflicts. But the victory of the referendum to leave the EU, which now threatens to inflict permanent harm on the U.K., was precipitated in part by the failure of EU institutions to deal with the sovereign-debt crisis in the early 2010s.

Those institutions had been weak from the start. Because the euro zone had a unified currency, it was impossible to use exchange-rate devaluations to help Greece and other countries hit hard by the crisis, as would have been possible had countries had separate currencies. And because the EU had no unified fiscal policy, it was difficult to bail out Greece via transfers from economically vigorous member states such as Germany.

The real solution to the crisis was to have coordinated bailouts of European banks (which had lent money to shaky member states) and bond purchases by the European Central Bank — basically, what the U.S. did. But resistance from Germany’s electorate, as well as a cultural bias against stimulus and quantitative easing, delayed this solution for years. This demonstrated the lack of responsiveness and coordination inherent to the EU project.

European integration had been a fragile project from the beginning. Unlike the U.S., the EU was linguistically fragmented, with many centuries of history of political conflict. Voters in France and the Netherlands rejected an EU draft constitution in 2005, and the U.K. was too skeptical to even join the euro zone. Without full buy-in from important members like France and the U.K., the EU was never capable of approaching the kind of national unity found in the U.S. Thus, it stumbled along as something halfway between a country and a free-trade zone, until a crisis inevitably came.

The question is whether that crisis represented a turning point for Europe — a shock that acts as the catalyst for a long, inexorable decline. Beyond the sputtering recovery of Greece and Italy, there are number of other signs that this pessimistic scenario will come to pass.

The EU as a whole continues to be vulnerable to crises, but it’s questionable whether smaller European states can thrive as independent economies. Businesses naturally want to locate where there’s a large consumer market. If the EU fragments, countries may implement trade barriers that would make the continent less attractive as a market, and cause business to migrate elsewhere — as might now happen to the U.K. after Brexit.

Oddly enough, Europe’s linguistic and institutional fragmentation might be what helped it get rich in the first place. Anthropologist Jared Diamond has suggested that Europe developed precisely because the large number of competing nations encouraged a lot of policy experimentation. This is in contrast with China, where some believe that imperial policy mistakes — and later, the insane policies of Mao Zedong — held that giant nation back at a critical time. But in the modern globalized age, the tables may have turned, and China’s unification may allow it to become the economic center of the world while a fragmented Europe flounders.

China is becoming the world’s hub for high-tech electronics manufacturing, and may soon dominate in more traditional European strengths like autos. Meanwhile, despite a few bright spots, Europe has generally struggled to create technology giants. Clunky, onerous regulation like the General Data Protection Regulation will probably make it harder to do so.

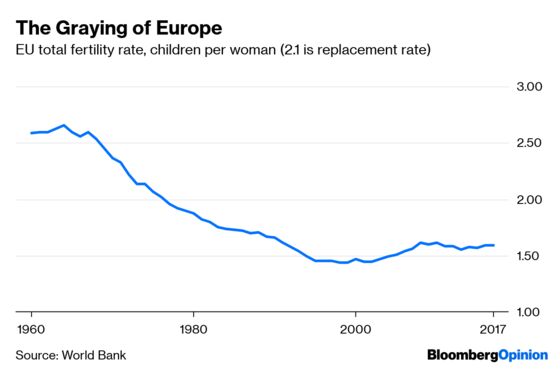

Beyond fragmentation and clumsy policy-making, Europe suffers from another fundamental weakness — low fertility rates:

This problem also afflicts East Asia, but that will come as cold comfort to Europe. Declining population will put strains on pension systems and make companies less interested in investing on the continent. The obvious policy is to increase immigration in order to maintain population levels, but Europe is not traditionally accustomed to diversity (as recent political turmoil over immigration has shown), and its labor markets may be too rigid to absorb large numbers of newcomers.

So there are many reasons to believe that future historians may see the financial crisis as the tipping point when Europe began to decline. The period of peace, prosperity and stability between the end of World War II and 2008 may turn out to have been merely a brief sunny plateau between the rise and fall of a continent whose technology and economies once dominated the world. It’s not obvious what Europe’s leaders can do to prevent this dark outcome, but they should be spending most of their time and effort thinking about how to avert it.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2019 Bloomberg L.P.