Markets Catch Spring Fever. Is It Justified?

A jolt of optimism leads financial commentary. Plus, eyes on earnings, a big day for Chinese bonds and more.

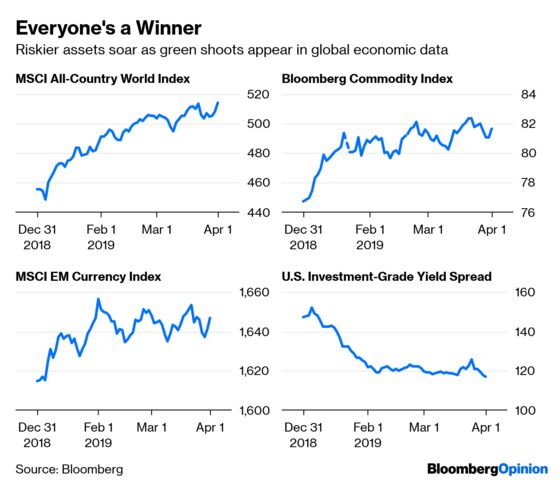

(Bloomberg Opinion) -- For the last couple of weeks, investors have been hearing from a few economists about how signs were emerging that the global economic slowdown was starting to moderate. The proof came Monday, as stocks, commodities, credit markets and emerging-market assets all shot higher like green shoots in springtime in response to some surprisingly upbeat economic reports, starting with manufacturing data in China over the weekend. The question now is whether this is sustainable.

The MSCI All-Country World Index of equities jumped 1.14 percent to close at a new high for the year on Monday, extending its gain from December’s low to about 18 percent. This performance reflects optimism that the dovish turn by major central banks led by the U.S. Federal Reserve may succeed in tempering the much-feared synchronized global economic slowdown. After all, even without officially lowering policy rates, the Fed’s jawboning managed to cut global borrowing costs by about 30 basis points this year to 1.75 percent, as measured by the yield on Bloomberg Barclays Global Aggregate Total Return Index. And let’s not forget that one of the reasons equities and other risk assets have done so well lately is the growing belief that the Fed and its major peers may even cut rates before the year is out. The problem is, with global stocks on the cusp of setting fresh record highs, central banks may be loath to loosen monetary policy for fear of being accused of fostering bubbles in financial assets. Even affirmed dove James Bullard, president of the St. Louis Fed, said last week that he expected second-quarter growth to rebound, and that calls for a rate cut were “premature.”

Beyond what central banks may or may not do in terms of interest rates, there are other reasons to be cautious. The top-ranked rates strategists at BMO Capital Markets wrote in a Monday research report that stronger data in China might lessen President Xi Jinping’s urgency to do a trade deal with President Donald Trump. The longer the two countries drag out trade talks, the more jittery markets may become. “Beijing is undoubtedly pondering whether or not to ‘wait out’ Trump until the results of the U.S. Presidential election next year,” the strategists wrote. Plus, “the White House, surely emboldened by the findings of the Mueller investigation, won’t be in a compromising state of mind nor willing to accept a deal not considered an absolute victory for domestic trade.”

POOR EARNINGS HAVE A SILVER LINING

As the calendar turns to April, attention will soon turn in earnest to how corporate earnings fared in the first quarter. Most everyone seems to expect profits to be flat to lower, which is no one’s catalyst for a continuation of the stock market’s strong performance in the first three months of the year. But what is encouraging is that earnings revisions in the all-important U.S. markets have largely stopped trending lower, and revenue in aggregate should be up about 4.5 percent from a year earlier, according to DataTrek Research. “That’s an underappreciated positive point for U.S. stocks, because confidence in revenue growth serves to offset recent macroeconomic worries,” DataTrek co-founder Nicholas Colas wrote in a research note Monday. Only two of the 11 S&P sectors should show negative revenue growth, with technology down 1 percent because of Apple Inc., and energy down by 3.5 percent because of commodity prices. The other thing to know about stocks is that despite this year’s rally, sentiment still seems to be very bearish. State Street’s monthly index of investor confidence plunged to an all-time low of 69.4 for January and hasn’t recovered much since; it came in at 71.3 for March. To put those numbers in context, the index only got as low as about 82 during the financial crisis and was above 100 – the level at which investors are neither increasing nor decreasing their long-term allocations to risky assets – as recently as last summer. The measure has authority because unlike survey-based gauges, it’s based on actual trades and covers 15 percent of the world’s tradeable assets.

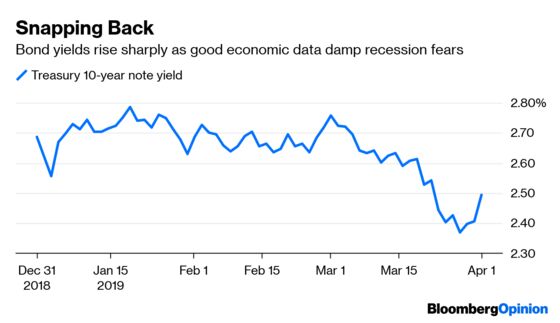

THE RISK IS HIGHER YIELDS

The bond market has a way of making even the best and brightest look silly. The recent big rally in U.S. Treasuries pushed down yields on 10-year notes to 2.41 percent at the end of the first quarter. At the start of the year, the median estimate of 59 Wall Street economists and strategists surveyed by Bloomberg was for the yields to end March at 2.88 percent, with the low forecast being 2.50 percent. The current outlook is for yields to end the year at 3 percent. Although that may be too high, it’s probably a safe bet that the next move in yields is to the upside rather than downward. Monday’s market reaction was an indication that bond investors had perhaps become too pessimistic in their outlook for the economy, as 10-year yields jumped 9 basis points to 2.49 percent in response to the positive economic data. Bond investors have “glanced over data reports and moved to the more serious issue of Fed 2019 policy,” FTN Financial interest-rate strategist Jim Vogel wrote in a research note Monday. “That changes this week.” The strategists at JPMorgan Chase & Co. led by Nikolaos Panigirtzoglou noted in a research report Friday that the drop in yields in recent months reflects bond traders pricing in an 80 percent chance of a recession. If so, then it stands to reason that yields will only rise if the incoming data continues to hold up and it looks like the Fed will lean toward raising rates by year-end instead of cutting them.

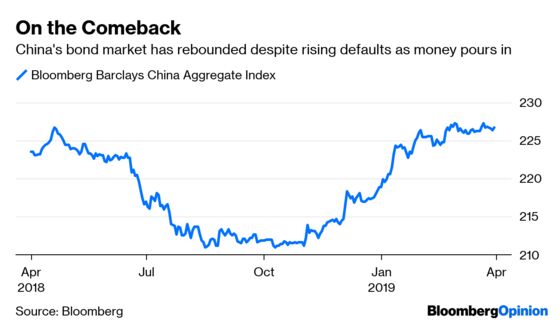

CHINA’S A BOND POWERHOUSE

You wouldn’t know it by the market action, where yields on five-year Chinese government debt securities rose a ho-hum 3 basis points to 2.93 percent, but Monday was a historic day for China’s bond market. April 1 was the first day that some of China’s onshore government and policy bank bonds were eligible to be included in the benchmark Bloomberg Barclays Global Aggregate Total Return Index. The securities will be phased in over a period of 20 months. Upon completion, 364 Chinese securities will account for 6.1 percent of the $54.9 trillion debt covered by the index, putting the nation’s $13 trillion debt market on track to overtake Japan’s as the world’s second-largest constituent, according to analysts. Ultimately, more than $100 billion will flow into China’s bond market from foreign investors, according to Bloomberg News’s Tian Chen and Annie Lee. One by-product of all this is that money flowing into Chinese bonds has probably kept yields and yield spreads on Chinese corporate debt narrower than they otherwise would have been given a spate of high-profile defaults. That, in turn, may be one reason China’s economy is doing better than many strategists have expected. Other index compilers, such as FTSE Russell and JPMorgan, are considering adding China’s debt to their gauges. (Bloomberg LP owns Bloomberg Barclays indexes and Bloomberg News.)

IT’S A MATTER OF PERSPECTIVE

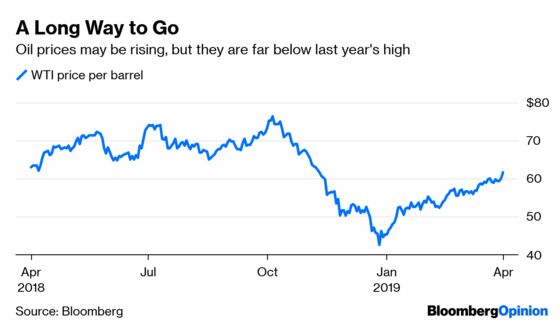

Oil is in the midst of an epic rally. U.S. prices surged 32 percent in the first quarter for their best performance in a decade as Saudi Arabia led OPEC and its allies in squeezing supplies to prevent a glut. The gain sounds impressive until you notice that West Texas Intermediate, at about $61 a barrel, is still down more than 20 percent from last year’s high of more than $76 a barrel in early October. Of course, that just shows how far crude had fallen at the end of 2018. But that’s not to say companies and individuals shouldn’t be worried about even higher prices on the horizon that could eat into profit margins and household budgets. A Bloomberg survey shows that OPEC’s output slipped in March for the fourth straight month, led by deep production cuts in Saudi Arabia, according to Bloomberg News’s Alex Longley and Alex Nussbaum. “It’s OPEC, for once sticking to their supply constraints,” they quoted Scott Bauer, chief executive officer of Prosper Trading Academy in Chicago, as saying. “In the past, they haven’t really heeded their own guidance. But this time they are, and it looks like it’s going to stay that way for the foreseeable future.” Iran’s oil minister concurs. The OPEC+ group could easily extend its agreement on oil-production cuts, Bijan Namdar Zanganeh said. “My understanding is, there is no difficulty extending the cooperation. It should be easy” to prolong the deal beyond the first half of the year, Zanganeh told reporters in Moscow following a meeting with his Russian counterpart Alexander Novak.

TEA LEAVES

Australia’s central bank will conclude a monetary policy meeting in a few hours, and while no change in interest rates is expected, it should still bear watching closely. That’s because of the strong manufacturing data out of China, which is Australia’s largest trading partner. Market participants will want to hear whether the Reserve Bank of Australia also suggests that things are turning around in China. Closer to home, conditions don’t look so hot. Australian business confidence fell to the lowest level in almost six years last month in another sign the economy is losing momentum. The index level dropped to 0 in March from 2 the previous month, the weakest reading since July 2013, a National Australia Bank Ltd. report showed Monday. Confidence fell across most industries, while manufacturing was flat and mining increased, according to Bloomberg News’s Michael Heath. “With forward indicators still looking weak, we will be watching closely over the next few months to assess whether conditions in the business sector weaken further,” Heath quoted Alan Oster, the chief economist at National Australia Bank, as saying.

DON’T MISS

Let’s Not Stress About the Next U.S. Recession: Bill Dudley

What Last Week Told Us About the Market: Mohamed A. El-Erian

The Forecasting Business Shouldn’t Be This Bad: Barry Ritholtz

Erdogan's Election Stumble Troubles the Lira: Marcus Ashworth

Trump Is Bullying OPEC Again. He Might Get His Way: Julian Lee

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.