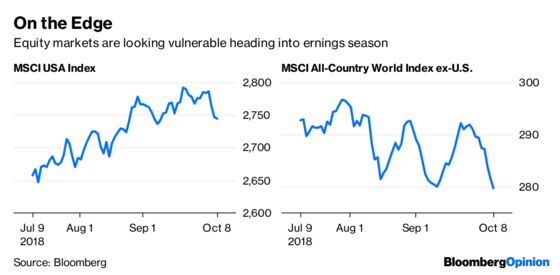

(Bloomberg Opinion) -- Equity markets are teetering. Monday marked the third consecutive decline in the 625-member MSCI USA Index. For non-U.S. stocks, the losses reached eight straight days. The reasons given are varied. The global bond market is tumbling, pushing borrowing costs to their highest since 2013. The escalating trade war between the U.S and China shows no signs of ending anytime soon — and may be getting worse. Italy looks to be headed toward a fiscal crisis and showdown with the European Union. The mood is so gloomy that hardly anyone seems to be excited about what should be another blockbuster earnings season.

In many ways, that's understandable. The stock market is less about what have you done for me lately, and more about what will you do for me in the future. Maybe investors realize this is as good as it gets, and some of the short-term boosts equities got from the U.S. tax cuts and other forms of fiscal stimulus will soon be wearing off. Although earnings for members of the S&P 500 Index are forecast to have risen 19.5 percent in the third quarter, estimates have come down of late. That's a break from recent quarters, when they rose heading into earnings season, according to Bianco Research. For the third quarter, 74 members of the S&P 500 companies have issued negative earnings-per-share guidance and 25 have issued positive guidance, according to FactSet. That's not the kind of development that is conducive to supporting relatively high valuations. As of last week, the forward 12-month price-to-earnings ratio for the S&P 500 was 16.7 times, which is above the average of 14.5 times over the past decade.

“Strong earnings have been the most important factor that has enabled the stock market to ignore the headwinds it has faced this year,” Matt Maley, an equity strategist at Miller Tabak & Co., told Bloomberg News. “If the projection for future earnings suddenly becomes less bullish, it could/should be enough to upset the balance between the bullish & bearish macro factors that are facing the markets right now.”

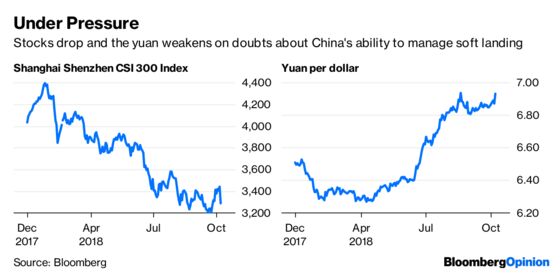

CHINA'S LOOKING DESPERATE

Of all the risks facing financial markets, none spook investors more than the prospect of a hard landing for China's economy. Chinese authorities are doing their best to bring down sky-high leverage levels and wring out other excesses without doing too much damage to the economy. And if China was hoping to project strength during tense trade negotiations with the U.S., it's not working. The CSI 300 Index fell 4.3 percent in Shanghai on Monday following a week-long holiday with no trading, the biggest decline since February 2016. The yuan fell 0.89 percent, the most among 31 major currencies tracked by Bloomberg. This all came after China said its foreign-currency reserves fell in September, as heightened trade tensions with the U.S. fueled concerns of capital outflows and further yuan depreciation. Reserves declined by $22.7 billion to $3.09 trillion in September, the People’s Bank of China said Sunday. What's really concerning is that this all came even as China’s central bank cut the amount of cash lenders must hold as reserves for the fourth time this year. The People’s Bank of China lowered the required reserve ratio for some lenders by 1 percentage point, effective from Oct. 15. The cut will release a total of 1.2 trillion yuan ($175 billion), of which 450 billion yuan is to be used to repay existing medium-term funding facilities which are maturing, the central bank said. To some traders, the move felt a bit desperate.

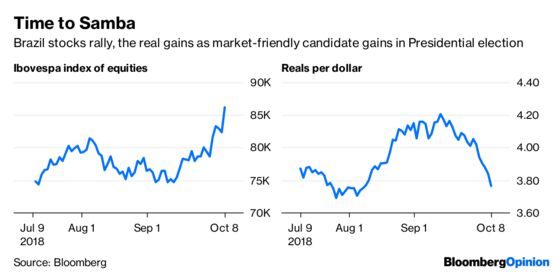

BRAZIL BONANZA

Although the momentum for China is downward, things are looking up for another critically important emerging market. Brazil's currency rallied along with stocks and bonds after investor favorite Jair Bolsonaro took a commanding lead in the first round of the presidential election, garnering support that surpassed all polls. The benchmark Ibovespa equity gauge surged 4.57 percent – the most since March 2016 — in Sao Paulo, and the real strengthened the most among global currencies, appreciating as much as 3.32 percent. Traders are cheering on Bolsonaro to avoid a return to the left-wing Workers’ Party and the economic policies of the past few years, which led to the worst recession in at least a century, blew out the budget deficit and cost the country its investment-grade credit rating. Although Brazilian assets are likely to behave well in the near term, volatility will likely increase as we head toward the end of October, according to Bertrand Delgado, director global markets and head of Latin America fixed income and foreign exchange at Societe Generale SA. "Given that the external outlook is likely to remain challenging over the coming quarters, the markets will most likely test the next president's willingness and ability to bring about a structural overhaul in Brazil in a relatively short timeframe," Delgao wrote in a research note.

ITALY'S NAMING NAMES

Only four countries in the world have more debt than Italy's $2.28 trillion: the U.S., China, Japan and France. It's almost unimaginable what would happen to the global financial system if Italy's newly elected populist leaders decided they no longer wanted to be part of the euro zone and resurrected the lira. And yet, investors are being forced to ponder that very scenario after some very inflammatory comments out of Rome on Monday. That's where Italian Deputy Prime Minister Matteo Salvini said Europe’s real enemy is European Commission President Jean-Claude Juncker, European Union economic policy chief Pierre Moscovici and the Brussels bureaucracy that pushes budget restrictions on its members and open borders. “We are against the enemies of Europe — Juncker and Moscovici — shut away in the Brussels bunker,” Salvini said. "The politics of austerity of the last few years has increased Italian debt and impoverished Italy." Yields on benchmark 10-year bonds rose above 3.5 percent for the first time in four years while the FTSE MIB Index dropped 2.43 percent to approach a bear market. Investors are now considering the potential for ratings downgrades, with S&P Global Ratings and Moody’s Investors Service due to review the sovereign before the end of the month, according to Bloomberg News's John Ainger and James Hirai. “The Italians are continuing to test the EU’s resolve,” Jens Peter Sorensen, the chief analyst at Danske Bank A/S, told Bloomberg News. “If neither the EU or Italy back down, yields will continue to climb higher from here. But I expect that Italy and the EU will find a compromise, even though it looks difficult at the moment.” The Bloomberg Euro Index fell as much as 0.4 percent to its lowest level since August.

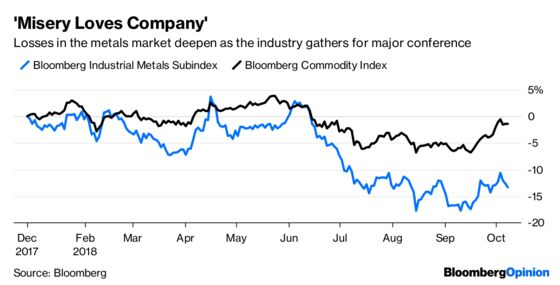

METALS IN NO MOOD TO PARTY

The global commodities market this week is focused on London and the LME Week metals conference that is one of the year’s major gatherings. The theme this year must be "Misery Loves Company" because the event isn’t doing anything to boost the market. The Bloomberg Industrial Metals Subindex dropped 0.86 percent to bring its decline for the year to 13.3 percent. If the losses hold through year-end, it would snap two years of gains in the gauge. Among the hardest hit metals on Monday was aluminum, which sank after Norsk Hydro ASA flip-flopped on whether a key alumina plant will close, while zinc fell on concerns about the weakening outlook in China, according to Bloomberg News. Aluminum lost 3 percent to settle at $2,067 a metric ton in late trading on the London Metal Exchange, the biggest drop since April. Zinc lost 0.8 percent, and nickel and lead also posted declines. Metals have been battered this year as the dollar rose and the U.S.-China trade war hurt prospects for demand. Aluminum has been roiled by U.S. sanctions against Russia’s United Co. Rusal, as well as Norsk’s troubles at its Alunorte refinery. While China cut banks’ reserve requirements for the fourth time this year, investors read the move “pessimistically” as an indication of increasing downward pressure on the economy, Wei Lai, an analyst at Cofco Futures Ltd., told Bloomberg News.

TEA LEAVES

Many people are tying the weakness in stocks to the big slump in the bond market, which has pushed yields globally to their highest since 2013. This week's debt auctions by the U.S. Treasury Department will go a long way toward answering the question of whether yields are high enough to attract bargain hunters and therefore arrest the selloff in both markets. The U.S. is offering $36 billion of three-year notes and $23 billion of 10-year notes on Wednesday, and $15 billion of 30-year bonds on Thursday. It's fair to say that the quick rise in yields on longer-term debt has caught most of Wall Street by surprise. At 3.23 percent at the end of last week, the yield on the benchmark 10-year Treasury note is up from 2.40 percent at the start of the year. The more than 50 economists and strategists surveyed by Bloomberg News didn't expect the yield to get this high until mid-2019, based on the median estimate.

DON'T MISS

Fed Is Intent on Raising Rates Even If Economy Sours: Tim Duy

China Hopes Old Tools Can Build New Economy: Mohamed A. El-Erian

Bears Beware, the Yuan Will Weaken on China's Terms: Shuli Ren

Hedge Fund Stars Crying Uncle Gives Industry Hope: Nir Kaissar

Next Financial Crisis Is Staring Us in the Face: Barry Ritholtz

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.