Manhattan Home Prices Fall Under $1 Million for the First Time Since 2015

Buyers seeking bargains send median to three-year low.

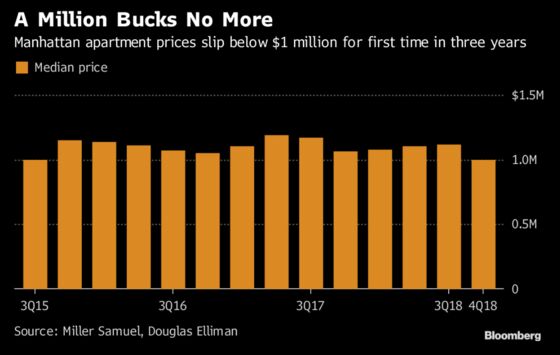

(Bloomberg) -- Manhattan home prices fell in the fourth quarter, with the median slipping to less than $1 million for the first time in three years, as ample inventory continued to allow buyers to demand sweeter deals.

Condo and co-op prices declined to $999,000 in the three months through December, a drop of 5.8 percent from a year earlier, appraiser Miller Samuel Inc. and brokerage Douglas Elliman Real Estate said in a report Thursday. Many apartments were sold for less than sellers originally sought, with an average discount of 6.2 percent from the last list price. That’s up from price cuts of 5.4 percent a year earlier.

It was the first time the median was less than $1 million since the third quarter of 2015, when it was $998,000.

The price decline is largely the result of shoppers having options. The inventory of existing homes on the market was up 17 percent from a year earlier. That’s given buyers greater negotiating power, and left sellers with no choice but to cut overly optimistic listing prices if they want to move properties.

“We had a number of cases where a lot of people came back for second and third visits, and never made an offer, and it’s totally and completely tied to pricing,” Steven James, chief executive officer of Douglas Elliman’s New York City division, said in an interview. “Many sellers still have not gotten the message. I think many more sellers in 2018 got the message, and those who got the message sold.”

Studio and one-bedroom units continued to see the most inventory gains. For all apartments, it took 15 percent longer to sell a home in the fourth quarter than it did a year earlier, according to Miller Samuel and Douglas Elliman.

‘Perfect Storm’

On top of a still-strong pipeline of newly built homes swelling inventory in the city, 2018 saw rising interest rates, new U.S. tax laws that further strained some homebuyers’ finances through caps on property-tax deductions and a stock market unkind to many investors.

“All that kind of created almost a perfect storm to drive down prices farther than people anticipated,” said Matthew Hughes, a broker with Brown Harris Stevens. “The market was very hot in 2015, 2016, and we needed a natural correction.”

As developers try to sell new homes, some are offering to pay transfer or mansion taxes, cover attorneys’ fees, or provide buyers such perks as a year of free butler or car service -- giveaways “that you’ve never even heard of just a couple years ago,” Hughes said. “I’ve seen it all.”

To contact the reporter on this story: Justina Vasquez in New York at jvasquez57@bloomberg.net

To contact the editors responsible for this story: Debarati Roy at droy5@bloomberg.net, Daniel Taub

©2019 Bloomberg L.P.