The Oil-Price Collapse Is Being Driven by Cars

(Bloomberg Opinion) -- If you’re asking which fraction of the oil barrel is responsible for the collapse in crude prices over the past month, look no further than the world’s drivers.

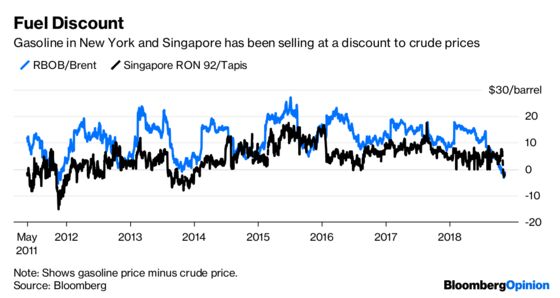

Nymex RBOB gasoline futures – typically priced at a premium to their raw material, crude oil – are trading at a sustained discount to Brent for the first time since 2011. It’s a similar situation in Singapore, where 92 RON gasoline has been cheaper than Tapis crude over the past few weeks, mirroring a pattern from late 2013 that came ahead of oil’s 2014 sell-off.

That’s not necessarily a disaster for refiners, which can make up their losses on gasoline with profits from better-performing products, such as diesel. But it’s an indicator that consumers in emerging markets, hit by 2018’s rise in oil prices combined with weakening currencies, are at risk of going on a demand strike.

Prices of major gasoline products in Thailand, the Philippines and India have all been slumping since early October. That’s not yet been enough to spark a revival in demand. In the Persian Gulf, stocks of light distillates – mainly gasoline – have hit record highs at the port of Fujairah in three consecutive weeks, according to S&P Global Platts.

The problem is that the world has too much of the light crudes that are most suitable for producing gasoline and too little of the heavier varieties that are better for diesel, jet fuel and fuel oil.

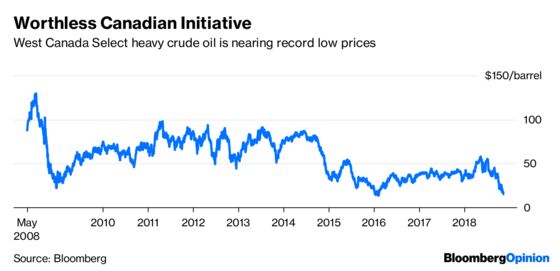

In the Americas, the gusher coming out of the oil patch in west Texas is mainly light, sweet crudes. Meanwhile, sources of heavier oil are struggling: Mexico’s production has been in decline for a decade, while Venezuela is reeling toward collapse and a shortage of pipeline export capacity has driven Western Canada Select below $20 a barrel.

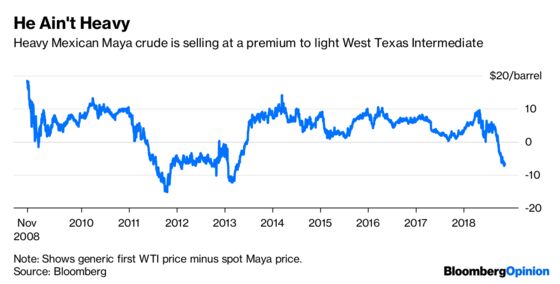

It’s a sign of U.S. refiners’ desperation to get hold of heavier crudes that heavy Mexican Maya is now trading at a premium to light West Texas Intermediate, an abnormal situation that hasn’t occurred since 2013.

It’s not clear that this situation is going to resolve quickly. While the gasoline piling up in Fujairah indicates that traders are hoping to shift cargoes from the Americas and Europe toward thirstier Asian markets, Chinese car sales have been slumping. Electric vehicles are taking a growing share of the market, and buying of conventional passenger cars is likely to have peaked.

Prospects may be better in India and Southeast Asia, but there too the discounts for gasoline against crude in Singapore suggest fuel retailers aren’t yet seeing the recent sell-off sparking resurgent demand.

Meanwhile, a bigger issue is looming next year: The International Maritime Organization’s pending rules on sulfur content in shipping fuel, which are likely to prompt increased consumption of middle distillates as a replacement for more polluting heavy fuel oil. Meeting that demand with the sweet mix of crude oils currently being pumped around the world will mean producing yet more gasoline that the world doesn’t appear to want.

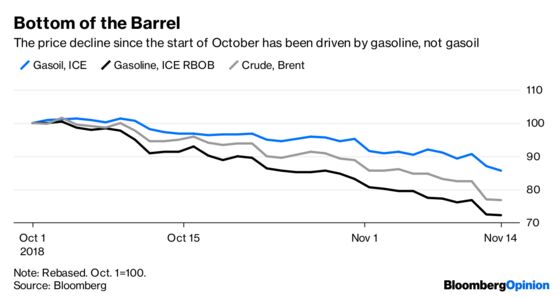

Right now, the balance between a tight market for middle distillates and an oversupply of gasoline is sending prices for crude slumping. Don’t count out the possibility that the middle of the barrel starts to become more of a factor for prices, though – or the odds that cheaper pump prices thanks to the past month’s sell-off finally get people driving again.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2018 Bloomberg L.P.