Looking for the Next China? There’s Just One Problem

Looking for the Next China? There’s Just One Problem

(Bloomberg Markets) -- There’s an old Polish saying that when two people quarrel, a third will benefit. And so global investors are now looking for the country best positioned to gain from the U.S.-China trade war.

China has been good to foreign investors over the past decade. Since the collapse of Lehman Brothers Holdings Inc. in 2008, the MSCI China Index has offered an annualized 8.6 percent return.

But last year was bruising. China staged one of the world’s worst stock routs, with the benchmark MSCI index tumbling about 20 percent. Meanwhile, the yuan flirted dangerously close to the psychologically important 7-per-dollar, a level that hadn’t been reached since the global financial crisis, fueling concerns that Beijing may weaponize the currency.

Is it time to ditch China and look elsewhere? With the higher tariffs that China Inc. faces, U.S. companies will be tempted to buy semiconductor parts from Malaysia, data storage units from Thailand, or cotton from Pakistan. Indeed, some asset reallocation is already taking place. Vietnam, for instance, was the only emerging Asian nation outside of China that received net foreign stock inflows last year. Many investors in the region have been betting the Southeast Asian nation will be the big winner out of the U.S.-China spat. Multinationals including Samsung Electronics Co. relocated factories there even before the trade war started.

Still, if you’re investing in dollars, moving assets out of China is nice only in theory. The devil is in the execution.

Any savvy global investor deciding where to deploy money at the beginning of the year has exchange-rate risk on their mind, as emerging-markets currencies are volatile and protecting against sudden movements can be expensive. For instance, in the first week of 2019, hedging the Indonesian rupiah or the Indian rupee with a one-year forward would set you back 5.4 percent and 4.2 percent, respectively. If you add the fact that stocks in those two nations already trade at elevated multiples of 16.8 times and 21.6 times earnings, this means any capital gain would likely need to come from earnings growth instead of from multiple expansion. Suddenly these hot emerging markets no longer look so appealing.

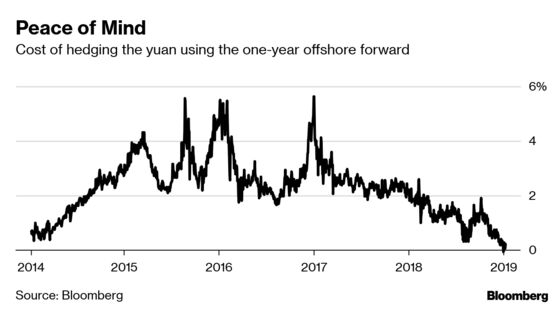

Hedging the yuan, on the other hand, is cheap this year. Using one-year forwards would cost you only 0.2 percent, peanuts compared with 5.6 percent or 2.2 percent at the beginning of 2017 and 2018, respectively. What’s more, China stocks now trade at only 11.5 times earnings, 28 percent cheaper than a year ago. From this view, China doesn’t look so bad, even with a trade war and economic slowdown.

Pressure on the yuan was in part helped by the U.S. Federal Reserve’s sharp dovish turn in early January. The implied rate of December 2019 federal funds futures fell from 2.93 percent in early November to 2.37 percent in the first week of 2019. In other words, futures traders see no further tightening whatsoever this year.

It can’t be stressed enough how important a stable currency is for emerging markets. If you doubt the yuan, compare it with the Turkish lira, Russian ruble, or Brazilian real, which have all been on roller coaster rides. Foreigners that rushed into those markets over the past decade could only groan with envy as China’s stocks outperformed.

In the currency space, the most fragile economies are the ones suffering from twin deficits, in the fiscal and current accounts, which are indicators that governments can’t balance their budgets and populations consume more than they earn. Brazil, India, Indonesia, South Africa, and Turkey fall into this category. Even if smaller nations such as Vietnam follow China’s export-oriented model, boosting economic growth by shipping apparel, electronics, and toys to the world, a current-account surplus is likely to be short-lived.

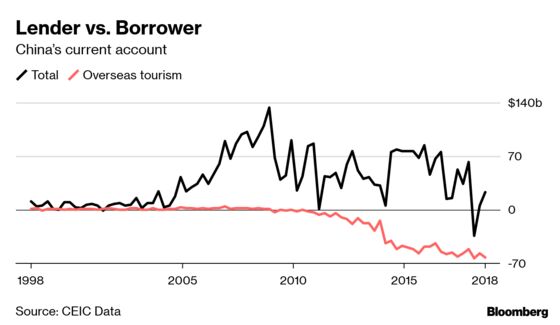

China’s path illustrates that point. Just a decade ago, the nation was the root cause of global payment imbalances, with a current-account surplus exceeding 10 percent of its 2007 gross domestic product. But the surplus dwindled to 0.4 percent of GDP last year, and the nation may well dip into a deficit in 2019, reckons Morgan Stanley. This is because, contrary to President Trump’s perception, China is no longer a frugal nation that sells a lot abroad and buys little in return. In the third quarter of 2018 alone, China’s middle class spent about $63 billion on overseas travel, eating into the exporters’ hard-earned surplus.

Indeed, China would have dipped into a current-account deficit a lot earlier if not for its heavy industries. Like in other nations, the defining features of a middle-class family in China are home ownership, a car, and a few credit cards. Nowadays, Chinese buy more than 20 million passenger vehicles every year—but more than 90 percent of them were manufactured at home. As a result, China’s net imports remained stable at about $42 billion a year.

Consumer products such as cars and household electronics are scale businesses, and thanks to its 1 billion-plus population, China can support such industries. But the economics don’t make sense for smaller nations, which have to import goods including cars.

To maintain an account surplus, smaller countries could try to remain frugal, exporting and not spending overseas. But that won’t produce another China, where billions of dollars of wealth has been created over the past decade. A China 2.0 requires young, eager workers who’ll build manufacturing hubs and, in turn, use fatter paychecks to buy their first cars or designer bags.

Forty years after Beijing embraced capitalism, the yuan remains heavily managed. But it’s not a bad thing for foreigners. As for the entire emerging-markets asset class, an alternative to China hasn’t materialized yet. Investors better get used to the notion that China is here to stay.

Ren is a Bloomberg Opinion columnist in Hong Kong covering Asian markets.

To contact the editor responsible for this story: Siobhan Wagner at swagner33@bloomberg.net

©2019 Bloomberg L.P.