India Is Missing the Wake-Up Call From Its Shadow-Bank Bust

Retail investors probably have no idea they’re financing Kapoor’s ‘diamonds’. ‘Yes’, that’s what he calls his promoter shares.

(Bloomberg Opinion) -- India’s finance industry is letting a good crisis go to waste by not learning from it.

The sudden $12.8 billion bankruptcy of infrastructure lender IL&FS Group, currently sequestered under a government-blessed, out-of-court process, underscores India’s lack of preparedness to handle a big shift in lending in recent years — away from banks.

Before I illustrate that challenge with a little story about a banking tycoon’s fundraising, a little background:

Over the last several years, the state-run Indian banks’ capital constraints have seen them cede market share to nonbanks. Nothing wrong there except that shadow lenders are the riskiest of trapeze artists: They have to perform without the ropes of deposit insurance and the safety nets of central-bank liquidity — two things banks take for granted. One fall could be a showstopper.

When the IL&FS show did stop, risk management was nowhere to be found; fiduciary responsibilities were similarly absent. Mutual funds that had been lapping up commercial paper and non-convertible debentures issued by shadow lenders, as well as the rating companies pocketing fees by blindly certifying their safety, sleepwalked into the crisis. And though both are being prodded by regulators to wake up, neither is displaying any zeal of its own.

After IL&FS blew up, the funding market froze, and the credit industry cried mommy, begging the central bank to act as the lender of the last resort. The Reserve Bank of India’s refusal to do so added to its brewing tensions with the government. Amid this mess, the least the mutual funds and the rating companies could have done was to signal a change in their own behavior.

Now let me tell you what they’re up to instead. Yes Bank Ltd. is a private-sector lender, controlled by co-founder Rana Kapoor. The bank annoyed the RBI with its egregious misreporting of nonperforming assets. In September, the RBI rejected Yes Bank’s proposal to let Kapoor continue as chief executive officer. A new CEO has to be found by January. Meanwhile, there’s a stampede among board members to leave. Yes Bank’s stock has sunk 50 percent in just three months.

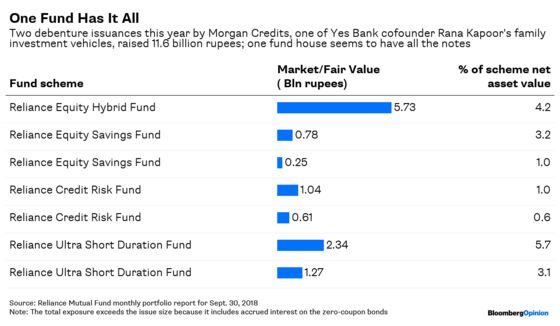

The jitters have reached the shadow banking world via Morgan Credits Pvt., one of the vehicles under which Kapoor’s family holds its Yes Bank stake. Morgan Credits offers the Kapoor family a neat way to monetize its shares without pledging them. To raise money, Morgan issued zero-coupon, nonconvertible debentures maturing in 2021, and it promised that the borrowed amount plus accrued interest will always be less than half of the market value of its holdings in Yes Bank. A good margin of safety for mom-and-pop investors while they earn some interest from a rich banker?

Reliance Mutual Fund certainly thinks so. Across plans, the fund seems to own the entire 11.6 billion rupees ($163 million) raised by Morgan Credits.

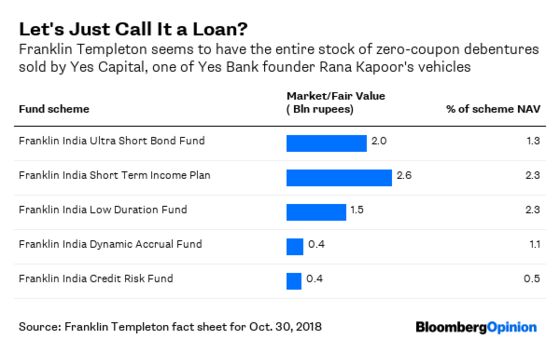

Reliance Mutual isn’t alone in doing such bilateral deals. As much as 3.27 percent of Yes Bank stake is with Yes Capital India Pvt., another of Kapoor’s vehicles. The family has monetized that stake, too, by issuing 6.3 billion rupees in zero-coupon notes. Most (if not all) of that is once again held by one fund: Franklin Templeton.

But things haven’t gone according to plan. The RBI swung its regulatory bat, and the debt ceiling for Morgan Credits was breached. At current prices, 3.04 percent of Yes is valued at less than two times the money the mutual fund has lent to Morgan. As the bank’s shares swooned, the Kapoor family fulfilled its promise to bring in liquid funds to make up the shortfall.

However, why let cash lie idle in a loan-servicing account? So, to allow this fund infusion to be reversed, a new version of the covenant was drummed up. The debt limit still holds, though now it would be busted only when the debt and accrued interest exceed half of Morgan’s 3.04 percent plus the 4.33 percent Kapoor owns in his own name. Satisfied by the legal strength of Kapoor’s personal guarantee, Care Ratings Ltd. reaffirmed the notes’ rating at A minus on Nov. 19.

One can understand why the family may not want to keep bringing fresh cash into Morgan, especially if it means selling Yes Bank stock. Doing so would only add to market panic. Kapoor took to Twitter in September to take a dig at the other co-promoter who had sold some shares. “Diamonds are forever,” he quipped.

Yet retail investors probably have no idea they’re the ones financing Kapoor’s diamonds, on the basis of debt covenants as fluffy as cotton candy. These are essentially unsecured loans to private investment companies, not suitable for mutual funds. Should fund managers use the cover of high credit ratings to mask the fact that no market exists for them whatsoever? That two months after the IL&FS debacle India’s financial industry should still be so unresponsive to risk-reward and fiduciary duties makes one wonder if these wild-swinging acrobats even deserve a safety net.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2018 Bloomberg L.P.