Lebanese Peg That’s Held Up for Over Two Decades Is Under Siege

Lebanese Peg That's Held Up for Over Two Decades Is Under Siege

(Bloomberg) -- Lebanon’s slow-churning currency crunch is fast engulfing Bashar Boubess’s business.

The miller pays for wheat imports in dollars but bakeries buy his flour in Lebanese pounds. For weeks now, the bank has refused to exchange those pound earnings back into the hard currency he needs to replenish supplies. His wheat stocks have dropped 30%.

Boubess has turned to money changers to keep his business alive, but it’s expensive: they demand more pounds for every dollar than the increasingly unrealistic official rate.

“If I sell to the bakeries in dollars, I’d just be transferring the problem to them,” said Boubess, owner of Modern Mills of Lebanon. “I don’t know if we can last the week. What am I supposed do?”

More than two decades after Lebanon pegged its pound to the dollar, providing an anchor of stability as the economy emerged from civil war, the moment of reckoning may finally be arriving.

The central bank on Tuesday announced that it will guarantee a supply of dollars at the official rate of 1,507.5 pounds to cover imports of wheat, gasoline and pharmaceuticals, which retail at government-regulated prices. The measure could go some way to averting social upheaval, after weeks of strikes and protests, but it also amounts to a tacit acknowledgement that everyone else is working to a parallel rate.

The divergence is small -- Boubess, for instance, said he last paid 1,595 per dollar to buy $50,000 at an exchange bureau -- and top officials including Prime Minister Saad al-Hariri have said the peg is a red line. But the widening imbalance has raised fears among Lebanese that a steeper slide is now only a matter of time.

The central bank’s reserves have fallen some $4 billion in the last two years to reach about $37 billion in July. As confidence has plummeted, even ordinary people have begun to transfer their dollar savings abroad or hide notes under their mattresses.

“You can’t help but be affected by what people are are saying and I’ve thought of transferring my money abroad,” said Rose, a widow who’s living on her late husband’s retirement savings and declined to give her name for privacy. “But if everyone withdraws their money, what will happen? There’ll be a crisis?”

High Stakes

For this tiny, import-dependent country that straddles the geopolitical fault-lines of the Middle East, the stakes have rarely been higher since the 15-year civil war that ended in 1990. The slow bleed of bank deposits, a key source of funding for the government, has exposed glaring vulnerabilities. The International Monetary Fund projects Lebanon’s current-account deficit will reach almost 30% of gross domestic product by the end of this year. Only Mozambique is in worse straits.

The central bank has repeatedly urged calm. Governor Riad Salameh told Bloomberg last month that reserves were “ample” and Lebanon has no intention of abandoning the peg.

Those words have done little to reassure investors increasingly worried that Lebanon’s political divisions are insurmountable and will bedevil any effort to cut spending, raise taxes and fight corruption -- measures required by international donors to unlock $11 billion in aid pledges sorely need to revive a sluggish economy.

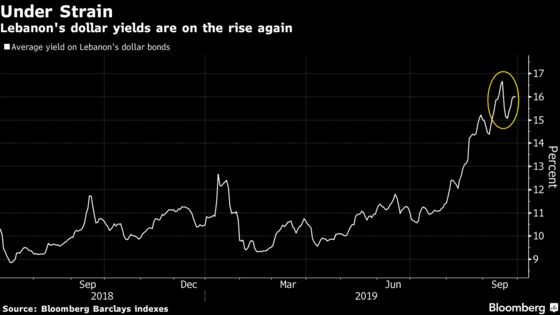

Moody’s said Tuesday it was putting Lebanon on review for a potential downgrade in its sovereign risk rating as the central bank’s drawdown of foreign exchange risks destabilizing the peg. The issue is preoccupying the airwaves, further diminishing demand for the national currency and pressuring the peg.

Lebanese expatriates, a mainstay of the economy for as long as anyone can remember, are sending less money home. Goldman Sachs Group Inc. estimates that deposit growth turned negative in May for the first time in decades.

“This peg policy might not be under threat now but it’s not sustainable because of a growing deficit of the balance of payment and a growing external financing gap,” said Sami Nader, head of the Beirut-based Levant Institute.

The sense of urgency isn’t lost on the government, but with a political system built around a fragile sectarian balance, decisions are notoriously difficult to reach and implement. Deputy Prime Minister Ghassan Hasbani is calling for “immediate action.”

“Doing the same old things without cracking down and executing reforms immediately, and without a transformational approach to doing business, will place further pressure on the peg,” he said in an interview Monday.

Near breaking point, many are now demanding authorities take action to avert a crisis. On Sunday, protesters burned tires and blocked roads in downtown Beirut as a public backlash builds against worsening living standards.

Gas stations have been closing in protest and wheat mills are warning of shortages if they can’t get enough dollars at the official rate, because paying the parallel rate squeezes their margins.

“Banks would tell me they can only give $5,000 daily,” said a gas station manager in Beirut. “But what can I do with the rest of my payments? I need dollars.”

As he spoke, his employees sat behind orange cones tethered with red and white tape, turning drivers away with a single word: Strike!

The financial prosecutor last week detained six money changers, later releasing them on bail, for trading outside the central bank’s band -- a criminal offense in Lebanon.

“Citizens are concerned and we need to reassure them,” said veteran lawmaker Yassin Jaber. “We haven’t been doing that.”

Dollar Lifeline

Lebanon still has enough to ward off collapse, said Marwan Barakat, chief economist at Bank Audi, the country’s largest lender by assets. The central bank’s international reserves stood at $38.7 billion as of mid-September, equivalent to three-fourths of Lebanese pound money supply, and banks’ overall foreign-exchange liquidity covers 40% of their customer deposits, he said.

Promises of assistance from Saudi Arabia and Qatar, energy-exporting Gulf Arab countries that helped pull Lebanon back from the brink in decades past, have yet to materialize, though talks continue.

Lebanon also plans to tap international debt markets in October for $2 billion to finance its needs for the rest of the year after the central bank paid off over $3.2 billion in maturing debt in 2019. It is due to pay another $1.5 billion this year.

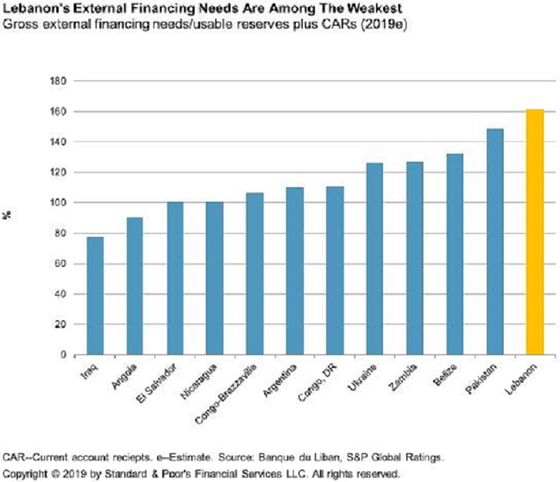

But under a definition of usable reserves that excludes assets not readily available for balance-of-payments purposes, Lebanon only has enough to cover about 42% of short-term debt, according to S&P Global Ratings, far short of the 100% threshold it says is the generally accepted minimum adequacy requirement.

Fitch Ratings, which ranks Lebanon at the same level as Zambia and the Democratic Republic of Congo, is warning the country’s large external financing needs will further erode the central bank’s gross reserves. Salameh has resorted to increasingly complex operations to ensure that the government can be financed without depleting the reserve.

Despite its efforts, the stockpile is essentially at the same level as when the central bank started the operations it calls “financial engineering,” according to Fitch analyst Toby Iles.

“It is questionable how much more room there is to keep attracting dollars through these operations.”

To contact the reporter on this story: Dana Khraiche in Beirut at dkhraiche@bloomberg.net

To contact the editors responsible for this story: Lin Noueihed at lnoueihed@bloomberg.net, Paul Abelsky

©2019 Bloomberg L.P.