Lazard Sifts Through Emerging Markets for Ideas After Slump

The asset management company joins a small but influential group of investors that is becoming more bullish.

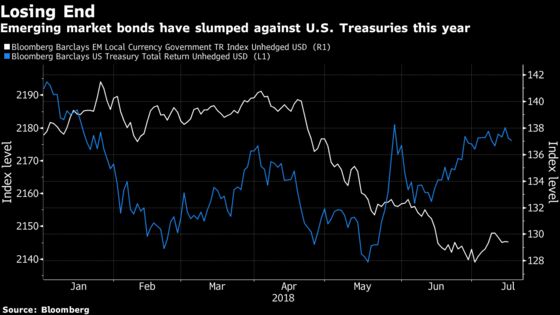

(Bloomberg) -- After the carnage in emerging markets in the second quarter, Lazard Asset Management LLC is finding value to jump back in, joining a small but influential group of investors that is becoming more bullish.

“The good news is when people sold emerging markets, they sold it all,” said Arif Joshi, a New York-based portfolio manager at Lazard, adding that the selloff provided him with opportunities rarely seen in his 20-year investment career. “We anticipate significantly positive returns from EM and we’re running our portfolio at close to the maximum of the risk budget both in dollar-denominated and local-currency debt.”

The debt team at Lazard is honing in on trades that include betting against Mexico credit-default swaps and buying bonds sold by governments in Ghana and Indonesia, said Joshi, who helps run strategies including the Lazard Emerging Markets Local Debt Fund. The selloff has taken valuation discounts to extreme levels as investors dumped assets indiscriminately, he said.

Lazard’s views echo others who expect a rally after rising U.S. Treasury yields, dollar strength and inflamed trade tensions pummeled currencies and bonds from Argentina to Indonesia. Goldman Sachs Group Inc., Franklin Templeton Investments and BlackRock Inc. say cheap prices, rising corporate profits and strong fundamentals will outweigh risks from a trade war, rising interest rates and potential U.S. recession.

“We’ve had the worst quarter ever in emerging-market history,” said Joshi, referring to a blended index of emerging-market fixed income assets that he tracks.

Below are edited excerpts from comments made by Joshi in Sydney:

Inflection in Ghana and Indonesia

Where you make the most amount of return in the market is where you have an inflection point. Ghana, whose debt to GDP peaked out at 77 percent in 2016, has brought that down to 63 percent in two years. The twin fiscal and current account deficits that were negative 7 percent had dropped to negative 3 percent.

To Ghana’s credit, this new administration has managed to hit every one of those milestones and the market’s rewarded them for it.

There are countries like Indonesia, where years back the government passed a constitutional amendment to limit the fiscal deficit to 3 percent. Lazard is long dollar-denominated Ghana and Indonesian bonds.

Turkey may surprise

Investors are either short or underweight Turkey -- there’s not a lot that they need to do to get Turkey to outperform because the market is all on one side. There’s a chance they’ll hike rates at the next meeting and the market will be extremely surprised at this point, and may rally quite a bit as people cover shorts.

Short Mexico CDS

We are short Mexico dollar-denominated credit-default swaps. We put that short on earlier this year when Mexican CDSs were trading at about 100 basis points over U.S. Treasuries, so it was very cheap protection.

Maximum risk budget

We went long emerging markets and short the U.S. dollar 16 months ago: we rode the market up in the second half and rode the market down over the last quarter. Now we’re riding the market back up. We’re likely to stay in this positioning over the next 12 months. We anticipate significantly positive returns from EM and we’re running our portfolio at close to the maximum of the risk budget both in dollar-denominated and local currency debt.

It’s highly unlikely that we’re going to change that view until one of two things occurs: valuations have to move from that extreme level and get back well below the median levels of yields and spreads that we’ve had in the past nine years. Or we get very strong signs that you are indeed at the end of the economic cycle in the U.S. We’re in between stage one and two right now.

U.S.-China trade war

Tariffs on Chinese imports don’t happen in September. (Joshi was referring to the “base case” with regard to President Donald Trump’s threatened tariff hikes on $200 billion of Chinese products.)

Two Fed hikes

By the September meeting, we’ll know whether those tariffs are coming. To the extent that they are, I would think at the December meeting that Powell would pause -- something the market isn’t pricing in at all. Second thing he could do is lower the terminal rate. Our base case is that the Fed will hike in September and December, and no trade war.

The market got into the right hand of the “dollar smile” in the first half of the year, but it’s likely to get in the middle up until we get to the end of the economic cycle in the U.S. That’s when we’ll see it go into the left hand of the smile.

To contact the reporters on this story: Adam Haigh in Sydney at ahaigh1@bloomberg.net;Ruth Carson in Sydney at rliew6@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, ;Tan Hwee Ann at hatan@bloomberg.net, Andreea Papuc

©2018 Bloomberg L.P.