Flood of China Mega Listings Will Tighten Hong Kong Liquidity

Landing Mega China IPOs Will Shake Up Hong Kong’s Interest Rates

(Bloomberg) --

Some of China’s biggest companies are planning to sell shares in Hong Kong, potentially locking up much of the city’s cash this year.

That could further destabilize Hong Kong’s already-volatile interest rates: mega listings like Alibaba Group Holding Ltd.’s late last year tend to mop up liquidity as traders set aside funds to buy stock. It drives up Hibor, which affects the cost of everything from mortgages to corporate loans, and can linger after big share sales.

While rival U.S. exchanges have in recent years attracted China’s top tech entrepreneurs with their more favorable fundraising rules, escalating tension between the world’s two largest economies is now raising Hong Kong’s standing. Just this week, the U.S. Senate approved a bill that might bar some Chinese firms from trading in the country, while Nasdaq Inc. is planning new restrictions aimed at smaller companies.

“The large and leading companies will come back first,” said Cliff Zhao, head of strategy with CCB International Securities Ltd. He predicts as many as 30 Chinese firms may seek to list in Hong Kong in the second half of the year. “The Hong Kong dollar will strengthen due to the huge demand for capital,” around any significant share sale, he said.

Concern over China’s surprise plan to impose a national security on Hong Kong may not deter Chinese firms from shifting to the city. Alibaba sold shares in Hong Kong in November, during the height of anti-government protests.

Margin financing around large listings further squeezes liquidity in Hong Kong’s banking system. The one-month interbank rate hit its highest since 2008 in the months leading up to Alibaba’s share sale. Xiaomi Corp.’s offering in 2018 had also sent Hibor to an almost decade high. Higher rates also tend to support Hong Kong’s pegged currency, which has been near the strongest it can trade versus the greenback since late March.

Hong Kong Exchanges & Clearing Ltd. is considering a move that may help ease the strain from IPOs on the city’s liquidity conditions. The exchange operator was this week consulting brokers on whether to cut the city’s settlement cycle for share sales, currently a five-day lag that’s unique among the world’s major markets. It ties up pledged capital for far longer than the Nasdaq, which has a three-day settlement period.

Hong Kong is emerging as the best alternative for Chinese firms who face increasing barriers to raising money from U.S. investors. Yum China Holdings Inc., JD.com Inc. and NetEase Inc. are among U.S-listed Chinese companies looking to tap Hong Kong’s $5.1 trillion stock market for fresh funds.

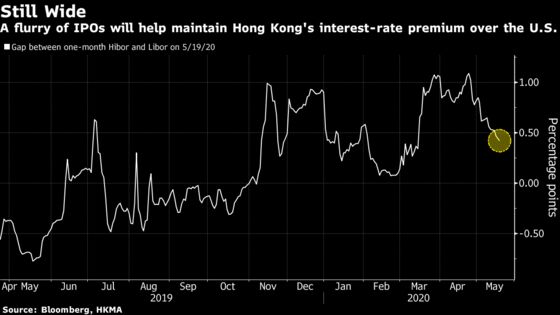

Even before any large share sales were confirmed for Hong Kong, the city’s exchange rate last month strengthened to 7.75 per greenback for the first time since 2016. That’s because traders were selling the American currency and using the proceeds to buy the higher-yielding Hong Kong dollar, making profit from the so-called carry trade. In April, the gap between Hong Kong’s borrowing costs and those in the U.S. was the widest in more than two decades.

To prevent the currency from breaching its trading band and to defend the city’s peg system, the Hong Kong Monetary Authority subsequently sold Hong Kong dollars. As a result, the city’s aggregate balance -- an indicator of interbank liquidity -- rose 75% to HK$94.7 billion ($12.2 billion) in four weeks. While that helped nudge Hibor lower, the rate’s premium over its U.S. counterpart is still about 50 basis points.

And so the carry trade remains largely profitable. While concern over Beijing’s tightening grip triggered the biggest loss in six weeks for the Hong Kong dollar, the currency had reversed most of that move by Friday morning. It traded within 1 pip from the strong end of its narrow band this week.

A potential flurry of IPOs means the appeal of the long Hong Kong dollar carry trade will remain, especially if listings coincide with periods of seasonally-high demand for cash, said Carie Li, an economist at OCBC Wing Hang Bank Ltd. At current levels, the aggregate balance would need to grow another HK$56 billion before the Hibor-Libor gap closes and the trade loses its charm, she said.

“You’ll see a lot of money coming into the Hong Kong market because of the influx of IPOs,” said Banny Lam, managing director at CEB International Capital Corp. “During the IPO process, a lot of money will be frozen that will push up the local Hong Kong interest rate.”

©2020 Bloomberg L.P.