Imran Khan Pledges Deep Reforms as Pakistan Nears IMF Deal

The International Monetary Fund stands ready to support Pakistan as it tries to tide over a balance-of-payments crisis.

(Bloomberg) -- Pakistan is close to a deal with the International Monetary Fund after nation’s Prime Minister Imran Khan pledged to carry out deep structural reforms of an economy that’s staring at a balance-of-payment crisis.

There was a convergence of views on structural reforms in a meeting with Managing Director Christine Lagarde in Dubai on Feb. 10, Khan said in a twitter post. Pakistan is close to an agreement after differences have narrowed, Finance Minister Asad Umar told reporters on Monday.

The South Asian nation is looking to bridge a financial gap of at least $12 billion with negotiations for its 13th IMF bailout since the late 1980s. While the United Arab Emirates and Saudi Arabia have both given Pakistan $3 billion each in support, the government is counting on inflows from ally China that has invested billions through the Belt and Road Initiative.

“I had a good and constructive meeting with Prime Minister Khan, during which we discussed recent economic developments and prospects for Pakistan in the context of ongoing discussions toward an IMF-supported program,” Lagarde said in a statement on Sunday. “Decisive policies and a strong package of economic reforms would enable Pakistan to restore the resilience of its economy and lay the foundations for stronger and more inclusive growth.”

Pakistan has extended talks with the IMF twice since November over the fund’s proposed changes to currency and tax policy. The nation last wanted to get a deal in time for a January meeting of its executive board.

Downgrade

Pakistan’s credit score was downgraded by S&P Global Ratings this month citing a worsening economic outlook amid a delay in striking a deal with the IMF.

The Pakistani rupee has declined by 20 percent in the past year, the most among Asian countries, according to a basket of 13 currencies compiled by Bloomberg. The nation’s reserves that have continued a downward spiral since mid-2016 stand at $8.2 billion, covering less than two months of imports.

“With the weaker economic settings, and limited progress in addressing fiscal imbalances following elections in mid-2018, we believe prospects for a rapid recovery in fiscal and external settings are now diminished,” S&P said in a statement. “Negotiations with the International Monetary Fund have taken longer than anticipated, and we now believe the reform timeline will be more protracted in nature.”

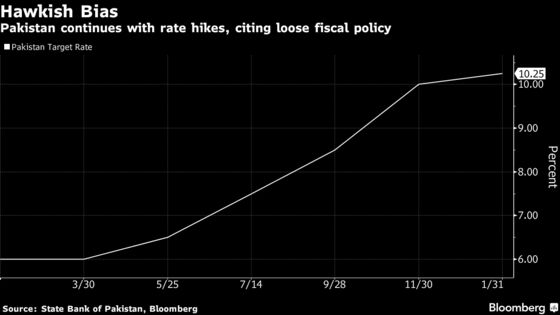

The nation has restricted imports and raised interest rates in five straight meetings but the fiscal deficit is yet to show signs of consolidation despite reduction in spending, Tariq Bajwa, governor at State Bank of Pakistan, said last month.

Pakistan’s Khan formed a government in August with an agenda to battle corruption and introduce reforms that stop regular requests to the IMF for bailouts. The South Asian nation’s boom and bust economy enters a balance of payment crisis whenever it grows as imports increase resulting in the widening of the fiscal gap.

Both sides agreed to work together on policy priorities and reforms aimed at reducing imbalances and laying the foundations of a job creating growth path in Pakistan, according to a statement by Pakistan’s finance ministry. In this regard, talks will continue to finalize an agreement of a program, the statement said.

--With assistance from Kamran Haider.

To contact the reporters on this story: Shaji Mathew in Dubai at shajimathew@bloomberg.net;Faseeh Mangi in Karachi at fmangi@bloomberg.net

To contact the editors responsible for this story: Shaji Mathew at shajimathew@bloomberg.net, Karthikeyan Sundaram, Khalid Qayum

©2019 Bloomberg L.P.