Lagarde’s Year of Listening May See ECB Get Earful on Prices

Lagarde’s Year of Listening May See ECB Get Earful on Inflation

(Bloomberg) --

If European Central Bank officials use their review of monetary policy this year as a chance to connect with ordinary people, they need to be ready for some plain truths.

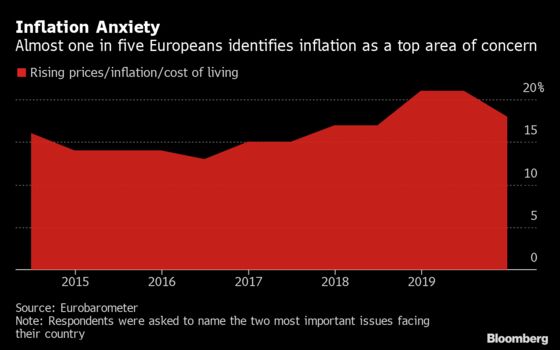

At the heart of the assessment, likely to be announced on Jan. 23, is how price stability should be defined and targeted. But ask citizens how they feel about inflation and they’re likely to come up with wildly varying answers. In fact, as the Federal Reserve found in its own recent consultation, many may be less convinced than central bankers that prices are rising too slowly.

While President Christine Lagarde says she wants to hear diverse views, it’s not yet clear how much that will involve people outside of economic and banking circles, nor how seriously policy makers will take the opinions submitted. If they did want consumers’ perceptions to influence how the review reshapes monetary policy, that could conceivably put the institution on a different path from the ultra-accommodative stance it has adopted for years.

“It’s definitely going to add to the knowledge the ECB has about the inflation process, and the ways inflation affects different groups in society,” said Florian Hense, an economist at Berenberg in London. “How much that is actually going to affect the overhaul or the result of that overhaul is a bit difficult to say.”

Lagarde, who wants to agree on the review at next week’s policy meeting, insisted last month that it will tap more than “the usual suspects.”

“It will also include consulting with Members of Parliament and I’ve committed to that with the European Parliament. It will reach out to the academic community, of course. It will reach out to civil society representatives, and it will aim at not just preaching the gospel that we think we master, but also listening.”

One example she might follow is that of the Fed, which held “community listening sessions” last year in places including San Francisco and Atlanta. The “Fed Listens” initiative heard how officials’ desire for higher prices wasn’t shared by lower-income workers, who fret about their living costs.

Such an exercise would appeal to Bank of France Governor Francois Villeroy de Galhau, who insisted last week that what consumers and businesses think, particularly on inflation, is crucial for the review’s credibility. “They are the ones that ultimately set prices and wages,” he said.

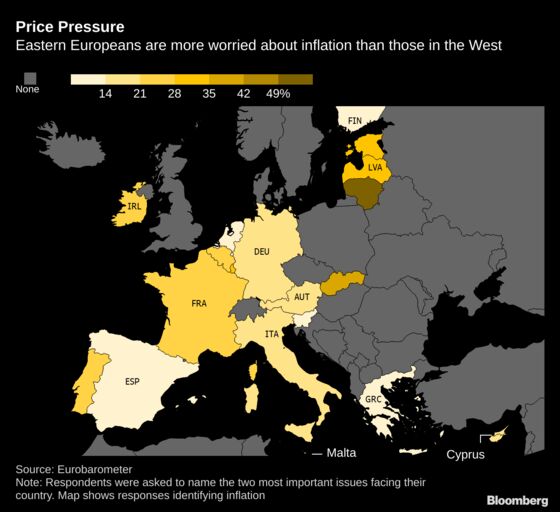

The approach has its problems though. A Bundesbank study published in December found “large differences” between German households on inflation perceptions depending on factors such as earnings, education, home ownership, job type and recent experience of price trends.

Housing is a key area of contention. It is significantly underweighted in the European Union’s official inflation measure because of the challenge of collecting data, yet it’s also a major expense for many individuals. Property values and rents have tended to outstrip inflation in recent years. Data on Thursday showed annual prices of homes in the euro region rose 4.1% in the third quarter -- roughly four times the pace of consumer inflation at the time.

Households not only tend to predict more inflation than investors, they also overestimate it. In July, former ECB Executive Board member Benoit Coeure cited a survey of citizens who believed annual price increases were near 9% in the 14 years through 2018, when the figure was actually 1.6%.

What Bloomberg’s Economists say

“The president indicated at the last press conference that inflation expectations will also be discussed. Which measures of inflation expectations tell us most about where headline CPI will be in two years? Economists have several to examine.”

-David Powell and Maeva Cousin. See her ECB PREVIEW

Coeure still noted that consumers are good at identifying shifts in inflation, and that their expectations can be “a better proxy” of company pricing decisions than financial markets. Under former ECB President Mario Draghi, policy makers tended to emphasize indicators of future inflation generated by investor bets, such as five-year, five-year forwards.

“The mood has changed, also because the policy space is reduced,” said Marco Valli, an economist at UniCredit in Milan. “There’s more inclination to look at different types of inflation expectations -- especially households.”

Lagarde’s strategy rethink is also an opportunity to better explain what the ECB is trying to achieve. Villeroy argues that if people can’t understand its goals, the effectiveness of its policies is blunted.

“They are less convinced than economists of the need to boost price growth from 1% to 2%,” he told an audience in Paris. “I believe the economic analyses and theories; but I also believe that they only have a real-world impact if they are perceived, accepted and assimilated by common sense and public opinion.”

Building a coherent view from a mass of public opinions is likely to be challenging, but it might be worth a try. At a time when many people in richer countries are furious at negative interest rates and quantitative easing, increasing the emphasis on their views could ultimately push the ECB to find more palatable ways to support the economy.

In any case, addressing erroneous perceptions of the ECB, as Villeroy suggests, will likely require more outreach. Lagarde has acknowledged as much, saying that bringing the central bank closer to citizens in an age of populism is a priority.

“It is important to me that our focus on connecting with the people we serve continues and grows stronger,” she told lawmakers in December. “Communication is a two-way street.”

--With assistance from Jana Randow and Zoe Schneeweiss.

To contact the reporters on this story: Craig Stirling in Frankfurt at cstirling1@bloomberg.net;Catherine Bosley in Zurich at cbosley1@bloomberg.net

To contact the editors responsible for this story: Simon Kennedy at skennedy4@bloomberg.net, Paul Gordon, Fergal O'Brien

©2020 Bloomberg L.P.