EU Leaders Under Pressure After ECB Salvo Fails to Calm Markets

EU Leaders Under Pressure After ECB Salvo Fails to Calm Markets

(Bloomberg) --

The European Central Bank and financial markets agree: It’s time for German Chancellor Angela Merkel and fellow government leaders to step up now to shield the European economy from the spreading coronavirus.

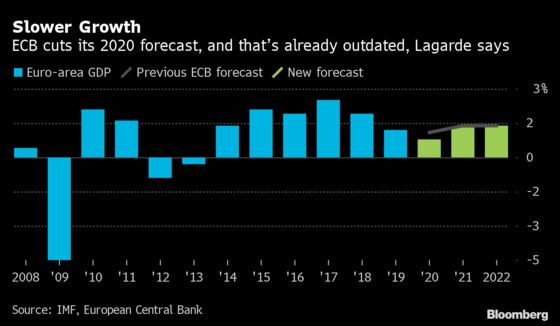

Confronting a crisis ECB President Christine Lagarde has privately warned could echo the meltdown of 2008 if policy makers don’t unite, the ECB unveiled a series of monetary policies Thursday that failed to pacify investors concerned that the euro-area is bound for recession.

Europe’s benchmark stock index posted its biggest-ever decline and borrowing costs jumped. The conclusion of investors: The ECB is all but out of ammunition to support the economy and now governments must do their part.

“The ECB cannot prevent a credit contagion, fragmentation or a recession by itself,” said Shweta Singh, a managing director at TS Lombard, a consultancy. “The fiscal policy response so far looks dismal.”

What Lagarde had sought to do was to “surgically” support the elements of the euro-area economy that will likely be hurt by the virus. The central bank promised to buy more bonds, and beefed up a loan program with terms that effectively amount to an interest-rate cut for banks that use it to push money into the economy.

But there was no cut in the already negative deposit rate that investors and economists had banked on. Nor was the idea even suggested in the meeting of officials, according to people familiar with the matter.

That, alongside a comment from Lagarde that the ECB wasn’t in the business of calming bond markets, was enough to alarm investors. It validated their suspicion that after more than 12 years of crisis fighting, the central bank has little scope left to support demand.

Indeed, in their meeting, the policy makers themselves acknowledged there is little monetary policy alone can do to tackle the fallout from a virus, the people said on condition of anonymity to discuss the details.

Lagarde was though crystal clear who she feels can act. “An ambitious and coordinated fiscal stance is now needed in view of the weakened outlook,” she said.

Macron’s Response

But in a sign of the mounting tension over the crisis response, French President Emmanuel Macron launched a rare public criticism of central bank policy, saying said the ECB’s plan wasn’t good enough.

“The ECB already today shared its first decisions. Will they be enough? I don’t think so,” Macron said in a televised address to the French nation. “It will be up to it to take new ones.”

His remarks followed a statement by his finance minister urging “massive and coordinated” fiscal measures at a European level to build on the ECB package.

Hemmed in by EU budget limits, France, Spain and Italy are all looking to Germany, whose traditional austere policy leaves it with money to spend should it want to.

There were some signs Thursday that Europe’s largest economy may be willing to do so, with Bloomberg News reporting that Merkel’s administration is prepared to abandon its long-standing balanced-budget policy.

The virus-triggered crisis is one of the “exceptional circumstances” under the constitutional debt brake that allows for additional borrowing, according to people familiar with the country’s economic policy, who requested not to be named because the discussions are not public.

What Bloomberg’s Economists Say...

“The European Central Bank’s emergency measures will provide significant monetary stimulus and limit the disruption to financial markets as the coronavirus hits the euro-area economy. Importantly, they are designed to deliver support as and where it’s needed.”

-- David Powell and Maeva Cousin

Click here for full report

While Merkel’s government is ready to explore additional spending, no decisions have been made on specific measures or an amount. The government did not respond to requests for comment.

The focus now falls on Brussels on Monday when European finance ministers are due to convene.

Lagarde put “tremendous pressure on euro area finance ministers and the respective treasuries to present a meaningful and coordinated package at Monday’s Eurogroup meeting,” said Guillaume Menuet, an economist at Citigroup Inc.

Whether Germany will ultimately prove a long-term source of stimulus for itself and the rest of the euro-area will hinge on the political transition now underway there.

Merkel has vowed to step aside when her term ends next year at the latest and her Christian Democrats are embroiled in a contest to choose her successor. If the conservative wing, often angered by Merkel’s concessions to her European partners, comes out on top, they are likely to cleave to the hard line positions advocated by Merkel’s long-time finance chief Wolgang Schaeuble.

A moderate in the Merkel mold might be more amenable to the appeals of the ECB, the IMF as well as the French and Italian governments. That would be especially true if they wind up in coalition with the Greens.

The real game changer in German politics is the rise of the environmentalists as a counterpoint to the far-right populists of the AfD.

With the center-left Social Democrats on the slide after paying the price for successive coalitions with Merkel, the Greens are in pole position to form the next government with Merkels’ CDU-led bloc.

There will still be opposition from the budget hawks in countries like the Netherlands, Finland and Austria. But Germany is the fiscal superpower in Europe.

If its next government has a strong presence from the Greens, and the European Commission’s push to eliminate carbon emissions gets off the ground, the outline of a new kind of fiscal policy could be beginning to emerge.

To contact the reporters on this story: Ben Sills in Madrid at bsills@bloomberg.net;Simon Kennedy in London at skennedy4@bloomberg.net

To contact the editors responsible for this story: Stephanie Flanders at flanders@bloomberg.net, Alaa Shahine

©2020 Bloomberg L.P.