Lagarde Inherits ECB Tinged by Bitterness of Draghi Stimulus

When Christine Lagarde takes charge of the ECB, she’ll inherit policy disputes of her predecessors, now with even deeper scars.

(Bloomberg) -- When Christine Lagarde takes charge of the European Central Bank, she’ll inherit the policy disputes of her predecessors -- now with even deeper scars.

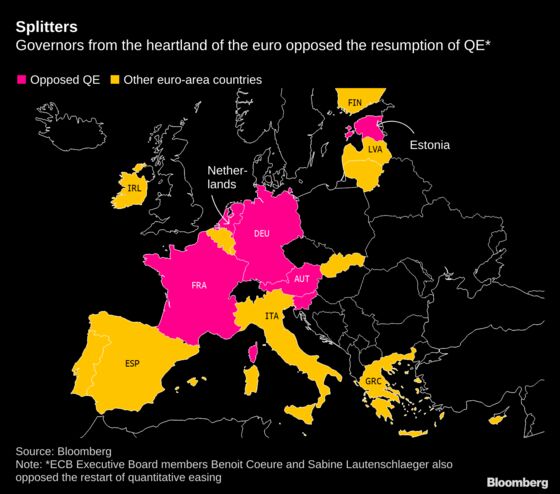

The new president will have to confront the aftermath of an unprecedented revolt among officials over Mario Draghi’s plan to reactivate quantitative easing. In a move probably linked to that, Germany’s Sabine Lautenschlaeger unexpectedly quit the Executive Board.

While such discord is reminiscent of when Draghi became president in 2011 after resignations by other German policy makers, the cumulative bruises from years of arguments present a challenge to Lagarde. She’ll need to determine how to lead the Governing Council while broaching inevitable disagreements, and to look at how to accommodate discord when it arises.

“The differences between the majority group and the hawkish group seems quite stark,” said Nick Kounis, an economist at ABN Amro in Amsterdam. “I don’t think she has a magic wand to make people who fundamentally disagree agree.”

Draghi has encountered dissent before, but never to such a degree. Bundesbank President Jens Weidmann and Klaas Knot of the Netherlands immediately criticized the Sept. 12 QE decision. Last week, Bank of France Governor Francois Villeroy de Galhau publicly declared his own disagreement, and Lautenschlaeger resigned.

The president was left relying on support mainly from southern Europe and the euro’s smallest economies, at a meeting described by one participant as the most tense he can remember. He spoke on condition of anonymity, because such discussions are private.

Lagarde can survey the wreckage first hand when she starts work in November.

She has already faced a call from Austrian policy maker Robert Holzmann to allow the views of individuals to be cited in accounts of meetings to acknowledge differences. That would be a step toward the openness of the Bank of England and U.S. Federal Reserve, which publish votes.

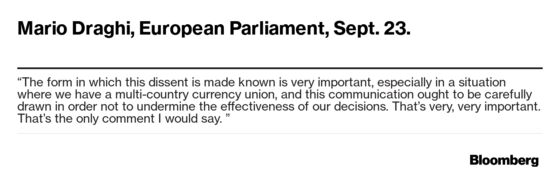

Such moves could go some way toward accommodating dissent while ensuring that, as Draghi said last week, disagreements don’t undermine policy decisions.

Even a safety valve to vent views might not be enough. Lagarde may also need to find a different way of initiating policy moves from Draghi, who often signaled major measures publicly without formal discussions with his colleagues first.

“It would probably be a mistake to try and emulate Draghi’s approach,” said Richard Barwell, an economist at BNP Paribas Asset Management.

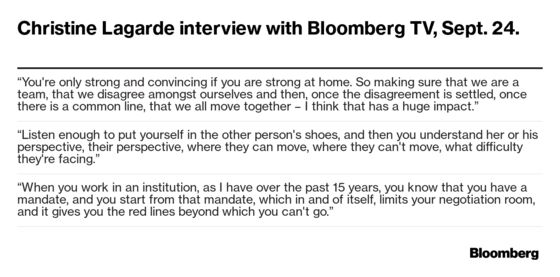

While Lagarde signaled in an interview last week that she’ll seek “teamwork” from her colleagues, she may also need to embrace more engagement than Draghi did -- and maybe share responsibility with her chief economist, Philip Lane.

That might help accommodate those who think their experience means they know better. She has never been a central banker, having served as French finance minister and led the International Monetary Fund.

Lowering the temperature will surely assist Lagarde if she wants to unveil further timely stimulus. More bond purchases could require the ECB to scrap self-imposed limits intended to safeguard against monetary financing -- a key principle for the Germans.

However, more discussion could slow down policy making in the already unwieldy group of 25 policy makers, including the six-member Executive Board.

“She will try to build a consensus,” said Barwell. “The center of gravity within the Council should therefore shift back toward the governors, away from the board -- dragging the reaction function of the ECB with it.”

Here’s how the current backdrop compares with those faced by previous presidents.

Founding Father

Established two decades ago under Wim Duisenberg, the ECB was modeled on the Bundesbank and governed by a mantra of price stability. Policy makers established a convention of decision by consensus, papering over disagreements. The founders of a fledgling institution managing an experimental currency wanted to protect nationally appointed policy makers from pressure to speak up for local interests.

Trichet Transition

Jean-Claude Trichet’s term began in 2003 with benign economic conditions. When the financial crisis struck, the ECB was initially swift to recognize the dangers, though subsequently twice abortively raised interest rates.

Consensus unraveled as German board member Juergen Stark and Bundesbank President Axel Weber disagreed with Trichet’s strategy for fighting the region’s debt crisis. Both resigned in 2011.

Draghi’s Dominance

The current president pushed the Governing Council into creating a crisis-fighting tool in 2012 to match his public commitment -- an unexpected pledge made six weeks earlier -- to do “whatever it takes” to save the euro. That was opposed by Weber’s successor, Weidmann.

In 2014, Draghi declared the need to start QE, months before the decision was actually taken, and Weidmann again objected. The current spat is a more dramatic version of that disagreement.

To contact the reporters on this story: Craig Stirling in Frankfurt at cstirling1@bloomberg.net;Catherine Bosley in Zurich at cbosley1@bloomberg.net

To contact the editors responsible for this story: Simon Kennedy at skennedy4@bloomberg.net, Fergal O'Brien

©2019 Bloomberg L.P.