Lagarde Has Euro-Fighting Options From Rhetoric to Rate Cuts

The euro’s rally to a two-year high is making ECB officials nervous, and putting economists on the lookout for some intervention.

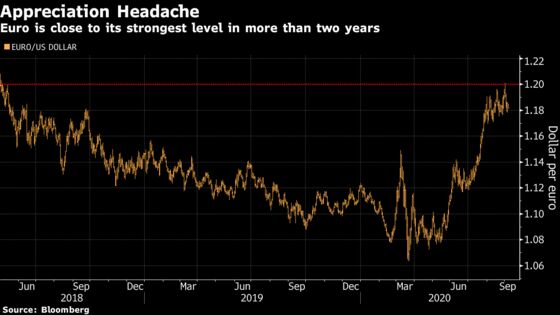

(Bloomberg) -- The euro’s rally to a two-year high is making European Central Bank officials nervous, and putting investors and economists on the lookout for some kind of intervention as soon as Thursday’s policy meeting.

The currency’s 10% jump since coronavirus lockdowns started in March makes ECB President Christine Lagarde’s job harder by putting downward pressure on inflation. Combined with signs that the economic recovery is slowing, it boosts the case for more monetary stimulus.

Such action looks unlikely when the Governing Council sets policy this week, but Lagarde and her colleagues might decide to start laying the groundwork in case they do need to act. Here are some of the options:

Talk It Down

While the ECB repeatedly says it doesn’t target the exchange rate, policy makers know their words can have an effect. After the euro rose above $1.20 last week, chief economist Philip Lane knocked it back by saying it “does matter” for monetary policy.

The single currency dropped for six straight days through Tuesday to below $1.18, though Bloomberg’s options pricing model points to a greater chance that it will trade above $1.22 in the next three months, than below $1.14.

Economists at banks including Barclays Plc, Goldman Sachs Group Inc. and JPMorgan Chase & Co. say Lagarde may emulate Lane after Thursday’s meeting. Her predecessor, Mario Draghi, made multiple verbal interventions.

“For now I think they’ll stick with jawboning,” said Charles Diebel, a money manager at Mediolanum International Funds. “But the euro level is important in terms of European recovery prospects so ultimately they will have to take it into account and respond.”

Signal More Easing

Lagarde may even want to hint at what the ECB would do. She might link the currency’s impact on inflation to the possibility of stepping up the pace of the 1.35 trillion-euro ($1.6 trillion) emergency bond-buying program, says Gilles Moec, chief economist at Axa SA. Another option could be to note the potential for an interest-rate reduction.

“The chances are rising that Lagarde floats a rate cut as a policy option as soon as this week,” said Frederik Ducrozet, a strategist for Pictet & Cie.

Cut the Deposit Rate

No economists expect lower rates this week, but money-market traders this week priced in a 10 basis-point cut in the deposit rate to minus 0.6% for September next year. Two months ago, they weren’t forecasting such a step until 2022 at the earliest.

Peter Chatwell, head of multi-asset strategy at Mizuho International Plc, expects the move by the second quarter of next year.

“By that time the euro will have exceeded $1.30,” he predicted. “The loss of export competitiveness and dis-inflationary dynamics will at that point justify it.”

Cut Targeted Long-Term Rates

The ECB didn’t join in with the wave of rate cuts during the pandemic. Its deposit rate has been at a record-low minus 0.5% for a year, since the final weeks of Draghi’s tenure.

Lagarde’s Governing Council seems more sensitive to the risk that the policy -- a charge paid by banks on the deposits they keep at the ECB -- squeezes lenders’ profit margins so much that it disrupts credit supply.

Officials have another option though, thanks totheir recent innovation: Dual rates.

Under new terms announced in March for its targeted long-term loans, the ECB will give banks cash for as little as minus 1%, on condition they lend it on to companies and households. That more than offsets the negative deposit rate.

Economists Eric Lonergan of M&G Investments and Megan Greene of Harvard Kennedy School wrote last week that the policy means “monetary stimulus has no practical limit” because rates can be cut without damaging the banking system.

“It could also be easier to sell to less-dovish members of the Governing Council,” said Anders Svendsen, chief analyst at Nordea A/S in Copenhagen.

Avoid a Currency War

Whatever policy makers do, they’ll be careful to describe their actions in terms of the outlook for inflation, rather than the exchange rate.

Major economies have long agreed not to indulge in competitive devaluations, and U.S. President Donald Trump has frequently accused the ECB of keeping the euro artificially low to aid exporters.

“It could not focus any action on the currency,” said Christoph Rieger, head of fixed-rate strategy at Commerzbank AG. “This would immediately trigger a backlash from the U.S. administration and risk a currency war.”

©2020 Bloomberg L.P.