JPMorgan Says Digital Currencies Must Balance Inclusion, Banks

JPMorgan Says Digital Currencies Must Balance Inclusion, Banks

(Bloomberg) -- The creation of central bank digital currencies to address economic inequality with new retail loan and payments channels must be designed so they don’t “cannibalize” a country’s commercial financial system, according to JPMorgan Chase & Co.

If set up hastily, retail CBDCs could risk “disintermediating commercial banks” and lead to the exodus of 20% to 30% of their funding base -- “potentially rapidly under stress,” JPMorgan strategist Josh Younger wrote in a note Thursday.

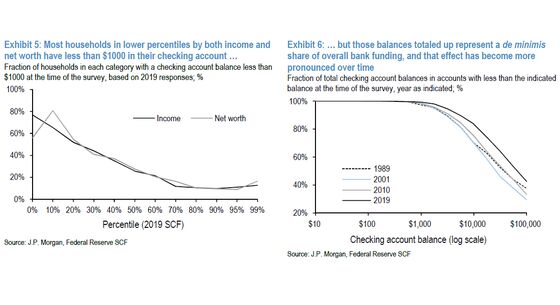

It’s possible to have more “financial inclusion” without significantly affecting the structure of the monetary system, he said. That’s because most lower-income households have less than $1,000 in their checking accounts, and those balances represent a small share of overall bank funding, according to Younger.

“If every last one of those depositors were to hold only retail CBDC, it would not have a material impact on bank funding,” Younger said.

“Financial inclusion” is frequently mentioned as a potential benefit of retail CBDCs. Federal Reserve Governor Lael Brainard, in May remarks, cited it as a major impetus for the U.S. central bank to consider its own CBDC. She also said the Atlanta and Cleveland Feds are conducting separate research projects on digital currency and financial inclusion.

“Hard caps of $2,500 would likely meet the needs of the vast majority of lower income households while not having any discernable effect on the funding mix of large commercial banks,” Younger said in the report. “Relatively heavy handed caps on holdings would be needed to reduce the utility of a retail CBDC as a store of value.”

©2021 Bloomberg L.P.