JPMorgan Says 2020 ‘Might Not Be a Year to Think About Recession’

The Fed’s change in tone may mean investors should reconsider the timing of the investment cycle.

(Bloomberg) -- The Federal Reserve’s change in tone may mean investors should reconsider the timing of the investment cycle, according to JPMorgan Chase & Co.

That means investors shouldn’t be driven by fears of recession for now, JP Morgan analysts said.

The Fed signaled last week that it’s done raising rates for at least a little while, and that it’ll be flexible in reducing bond holdings. The Fed’s changes have already been welcomed by equity investors who boosted the S&P 500 2.5 percent over three sessions, while rates traders have been working to figure out the implications of the newfound caution about shrinking the balance sheet. Demand for gold has increased as well.

Apart from the immediate implications, the Fed’s adjustments may warrant changes to JPMorgan’s previous outline that investors should consider moving fully to neutral and tilting defensive in the second half of 2019 to reposition for “durable challenges in 2020,” the firm said.

“If the Fed is less spooked by full employment, more tolerant of an inflation overshoot and less anxious to reach restrictive policy, then 2020 might not be a year to think about recession and so late 2019/early 2020 would be premature to position defensively cross-asset,” strategists led by John Normand wrote in a note dated Feb. 1.

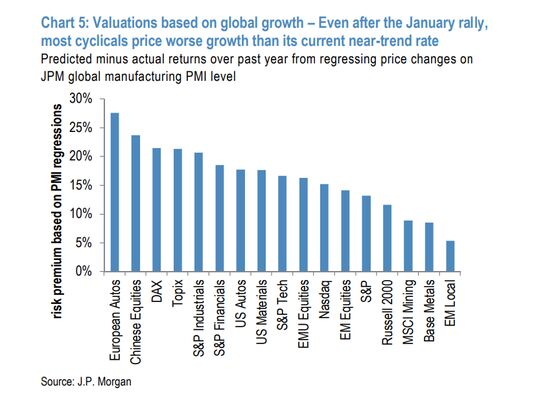

Many global measures of assets are pricing in slower economic growth than the current pace, the report said, including on risk premiums:

Cyclically oriented gauges like the S&P 500, European Autos, Chinese Equities, Topix, Emerging-Market Equities and MSCI Mining “still seem to trade as if global growth were running about a percentage point weaker than its roughly 2.6% current pace,” the report said.

JPMorgan arrived at the figure by regressing annual returns on a PMI index, comparing actual to predicted returns, and backing out from this risk premium an implied global growth rate.

“This framework is quite crude in that a single variable like the global PMI explains only about half of the variation in most of these assets’ returns,” the strategists wrote. “But as the signal is consistent with those of other fundamental frameworks, we are comfortable asserting that even modest improvements in global growth can push markets higher, because there is no evidence of overvaluation.”

To contact the reporter on this story: Joanna Ossinger in Singapore at jossinger@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Ian Fisher, Tony Czuczka

©2019 Bloomberg L.P.