The $7.9 Trillion Pile of Negative-Yielding Debt Is Growing Fast

The $7.9 Trillion Pile of Negative-Yielding Debt Is Growing Fast

(Bloomberg) -- For all the hand wringing over the end of ultra-loose monetary policy, the world just doesn’t seem able to shake its addiction to negative-yielding debt.

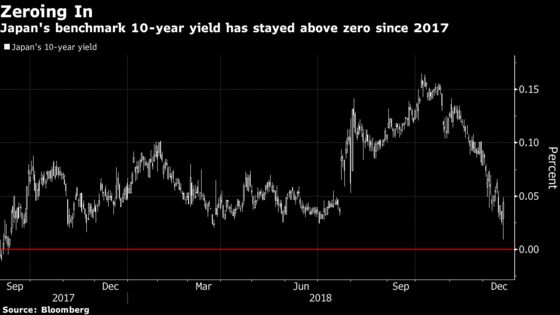

Only two months ago, speculation was rife that the Bank of Japan would have to step in to stop yields from rising. Now, rates on benchmark bonds are poised to drop back below zero. In Germany there are no positive yields as far as seven years along the curve. And globally, bonds with negative yields total $7.9 trillion -- close to levels seen at the start of the year -- and up from the 2017 low of $5.7 trillion reached in October.

Bonds are back in demand after a sea change in sentiment swept financial markets in recent weeks as the outlook for growth decisively worsened.

“I expect the global economy to be substantially worse in 2019 than this year,’’ said Akira Takei, global fixed income manager in Tokyo at Asset Management One Co., which oversees the equivalent of $500 billion. “The recent drops in bond yields and equities reflect such outlook. Investor views are also changing on the U.S. as an end of the current policy tightening is coming into sight.”

Small wonder developed-market bonds are headed for their best December in seven years, and 10-year U.S. Treasury yields have fallen as low as 2.80 percent, further undermining forecasts they were headed for 4 percent or higher. A cocktail of bad news from sliding U.S. home sales to worsening global manufacturing data point to slowing growth, putting further pressure on yields.

That leaves global financial markets struggling to emerge from the era of ultra-low yields started after the global financial crisis, even with the Federal Reserve on track to raise interest rates this week for the ninth time since December 2015 -- and the European Central Bank pledging to start tightening policy next year.

Japan’s Negativity

Japan’s 10-year yields dropped to as low as 0.01 percent on Wednesday after having stayed positive since September 2017. Some BOJ officials have said they see no problem with yields declining to zero or even below, according to people familiar with the matter.

JGB markets are becoming increasingly volatile as benchmark yields approach zero. The central bank’s decision to refrain from cutting bond purchases at its regular operations Wednesday spurred a surge in futures and a margin call from the Japan Securities Clearing Corp.

Japanese yields are riding a global downtrend sparked by Treasuries, said Eiichiro Miura, general manager of the fixed-income investment department at Nissay Asset Management Corp. in Tokyo.

“Markets are worried that a recession will come within a year because rate hikes will hurt the economy, sending stocks and credit markets lower,” Miura said. This will make it increasingly difficult for the BOJ to move toward policy normalization and push yields even lower, he said.

Weaker and Weaker

Weakening growth -- both globally and in the U.S. -- has been a major driver of lower Treasury yields, agrees Jon Hill, an interest-rate strategist at BMO Capital Markets Corp. in New York.

While a lot of U.S. economic figures are still pretty strong, “if you look one year, two years, three years, whatever, the confidence in how long that positive momentum can sustain becomes weaker and weaker,” he said. If the Fed sees the neutral rate as being below 3 percent, then 10- and 30-year yields will struggle to move higher than that level, he said.

Opposing Views

Not all developed markets are likely to see yields decline next year, according to M&G Investments. While the London-based money manager is stockpiling Treasuries, it’s also shorting 30-year bunds, betting yields on Germany’s debt will rise as the ECB cuts debt purchases.

“The euro area is in a better position today than it has ever been in the past, arguably, and yet bund yields really don’t show that,” said Pierre Chartres, investment director at M&G Investments in Singapore, which oversees the equivalent of $362 billion. “The path for yields is upward in the future and we want to benefit essentially from that.”

Europe’s Monsters

But optimism in Europe has faded as signs of slowing growth and escalating political tension push German yields toward 0.2 percent, down from more than 0.8 percent in February. While the ECB is capping its 2.6 trillion euro ($2.96 trillion) asset-purchase program this month, traders see slim odds of a move higher in interest rates next year.

Bunds will be supported by a number of factors next year including a shortage of supply, political risk in Italy and the fact they remain attractive for foreign investors on a currency-hedged basis, according to Bank of America Merrill Lynch.

“For the euro area it is indeed easier to find downside than upside risks,” strategists Ralf Preusser and Sphia Salim wrote in a note to clients, who see yields rising to only 0.6 percent by the end of next year. “Monsters always lurk under the bed.”

--With assistance from Masaki Kondo, John Ainger and Sydney Maki.

To contact the reporters on this story: Ruth Carson in Singapore at rliew6@bloomberg.net;Chikako Mogi in Tokyo at cmogi@bloomberg.net

To contact the editors responsible for this story: Paul Dobson at pdobson2@bloomberg.net, Nicholas Reynolds

©2018 Bloomberg L.P.