Japan Is Having Its Own Heated Debate Over Modern Monetary Theory

Olivier Blanchard of MIT argues that it is only possible to finance large deficits by money creation.

(Bloomberg) -- The hottest economic doctrine around says governments should stop worrying and learn to love their public debt. Japan’s been more relaxed than most –- but a looming tax hike suggests it may be about to blink.

Modern Monetary Theory posits that countries which control their own currency can seek stronger economic growth via government spending, without risking default. The only limit on spending is inflation -- a remote prospect in Tokyo, where steering clear of deflation is the priority and a 2% price target remains far out of reach.

It’s a controversial idea that has detractors and admirers worldwide, and may even surface in next year’s U.S. election campaign. Japan is often cited as evidence the theory is accurate. Now it’s having its own version of the MMT debate.

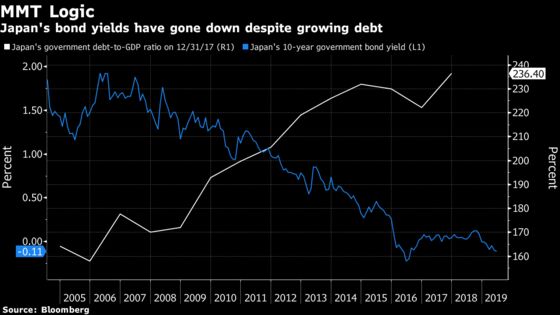

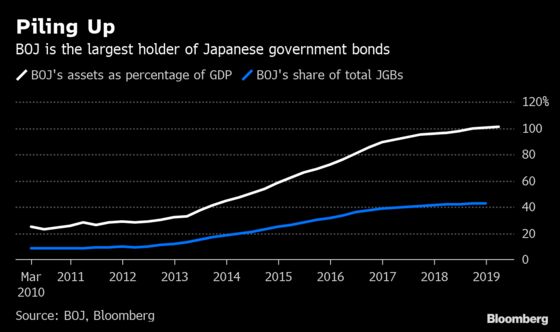

The world’s third-biggest economy has been running budget deficits for two decades and selling a chunk of the resulting debt indirectly to its own central bank with interest rates at around zero. The lines that usually divide fiscal and monetary policy have blurred -– and MMTers say that’s fine.

But Japan’s rulers have been looking to trim their budget deficit for several years as they seek to address the world’s biggest government debt load at more than twice the size of the economy. The higher sales tax promised for October is central to their plan.

‘Not a Debate’

For Prime Minister Shinzo Abe’s government, and the Bank of Japan under Governor Haruhiko Kuroda, the argument that extra taxation might not be needed is viewed as heresy.

The tax hike is necessary to secure Japan’s welfare system and another postponement risks a credit ratings downgrade, Finance Minister Taro Aso said Monday, dismissing the views of an MMT advocate in parliament. “This isn’t a public debate, it’s a theory, though I’m not sure I should even call it a theory, it’s a line of argument,’’ Aso said.

The question came from a member of his own party, where some lawmakers think the government should be taking the opposite tack and spending more to shore up economic growth.

The issue of austerity versus fiscal support resonates well beyond Japan, where central bankers and finance ministers will gather for a Group of 20 meeting this week.

Solar System

Many of them are under heightened scrutiny at home. Low interest rates in advanced economies haven’t done enough to kick-start economic growth, lift wages or alleviate inequality. And that’s raising questions about whether the standard policy tools have outlived their use -- and fueled populist insurgencies that demand fundamental change.

Advocates of MMT say it’s time for a complete rethink of the economic solar system –- what money is, what taxes are for, and what government spending can achieve. They say there’s no need to fixate on deficit and debt metrics when there’s no sign of discomfort in bond markets, like in Japan. Yields on 10-year sovereigns have stayed below 1% percent since 2013 when the BOJ ramped up its buying spree.

Proponents say MMT isn’t like a switch you can turn on and off -- it’s a descriptive framework that applies to governments in full control of their currency, whether or not they choose to use all their options. Such countries don’t need tax revenue to balance the books, MMTers say, though they may use taxes to restrain demand when it overheats.

“There’s nothing wrong with the idea of MMT,’’ said Satoshi Fujii, who served as an economic adviser to Abe for six years. He’s called for a postponement of the tax increase and additional public spending of 15 trillion yen ($140 billion) a year over three years to jump-start inflation.

Still, a more conventional explanation for why Japan has avoided flight from bond markets is that around 90% of the national debt is domestically held -- something that separates it from peers like the U.S., which relies on China and other foreign creditors.

Mainstream economists, even when they’re generally supportive of more government spending to promote growth, warn that MMT risks letting public finances get out of control. Olivier Blanchard of MIT argues that it is only possible to finance large deficits by money creation without sparking inflation when interest rates are at zero.

For now, the BOJ is running low on ammunition, proving the case that a central bank can’t simply conjure up price-growth out of nowhere without the help of government spending.

Like Aso, Kuroda is dismissive of MMT. In April he described it as extreme, inappropriate, and entirely unrelated to what Japan has been doing.

Bill Mitchell, an MMT pioneer and co-author of a new macroeconomics textbook based on the theory, isn’t impressed.

"Aso can deny it for all he is worth," said Mitchell, a professor at the University of Newcastle in Australia. In fact, Japan has been a "laboratory to establish the principles of MMT and the consequences of different fiscal and monetary policy initiatives," he said.

Hiroshi Ando, a lawmaker from Abe’s party, is less squeamish about MMT than his leader. He’s organized study sessions for colleagues who support bigger budget deficits to learn more about the doctrine. About 10 of them attended a discussion on May 15.

“If you understand this theory,’’ said Ando, “you will come to the conclusion that it’s utterly untrue to say Japan’s finances are in a critical state.’’

--With assistance from Masahiro Hidaka and Emi Nobuhiro.

To contact the reporters on this story: Toru Fujioka in Tokyo at tfujioka1@bloomberg.net;Enda Curran in Hong Kong at ecurran8@bloomberg.net

To contact the editors responsible for this story: Malcolm Scott at mscott23@bloomberg.net, Paul Jackson, Ben Holland

©2019 Bloomberg L.P.