Italy Sticks With Budget Plan, Won't Be Cowed by Market Threat

Italy’s new government will have both tax cuts and a universal basic income in its very first budget.

(Bloomberg) -- Italy’s new government will have both tax cuts and a universal basic income in its very first budget to show financial markets the coalition isn’t backing down from its agenda, Finance Minister Giovanni Tria said.

The sweeping economic program is aimed at proving to investors that the populist administration is serious about its mission, even after its creation initially rocked Italian bond markets. Basic income for the poor is a measure strongly backed by the Five Star Movement, while governing coalition partner, the League, promised voters a reduction and simplification of tax brackets.

The two measures “need to go hand in hand as they are necessary in order to change the system and to support economic growth,” Tria, 69, said in Rome in a Bloomberg interview, his first with an international news organization since being sworn in on June 1.

“Higher economic growth must come from the gradual implementation of the government program,” the finance chief and former economics professor said. “Such a path will require us to act on the composition of both tax revenues and expenditure -- our discontinuity with the previous governments won’t be about the deficit level, but rather about the policy mix.”

| What Our Economists Say... "Interest rates don’t have to increase a lot to make Italy’s debt unsustainable, even in the absence of additional spending. If the average cost of debt were to rise to 3.5 percent from 3.1 percent, the debt-to-GDP ratio would be on an upward trajectory. The seven-year yield can be used as a proxy for the figure because the average maturity is about that and it already stands at 2.1 percent." --David Powell, Senior euro-area economist, Bloomberg Economics See our Italy Insight for more. |

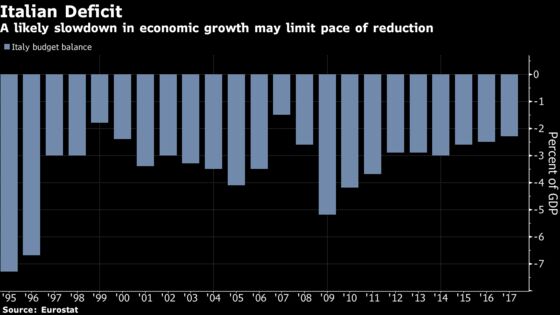

Fiscal Plans

Asked about the threat of a ratings downgrade because of the fiscal plans, Tria said his numbers and simulations available at the international level show it “wouldn’t be justifiable.” He also said that the time may have come for an agreement at the European level on excluding some investments from the deficit calculation, allowing for further budgetary room.

Since being sworn in last month, Italy’s populist coalition led by the League’s Matteo Salvini and Five Star’s Luigi Di Maio has been sparring with European leaders over issues ranging from migration to the future of the European Union. While Tria confirmed his government’s intention to remain solidly within the euro zone, he said there are many “dysfunctions within the monetary union” which need to be addressed.

“Nobody wants to leave the euro, but if we don’t fix it, things risk getting worse,” he said.

Deficit Reduction

A likely slowdown in economic growth in Italy and the rest of Europe may lead the government to reduce the pace of budget deficit reduction “which will allow for more capital-expenditure funding, not for more current spending,” while progressing with the reduction of the debt as a ratio of the country’s output, Tria said.

While reiterating that the government won’t pass any supplementary budget adjustments this year, Tria said that it can end 2018 within the deficit and debt forecasts set by the previous administration. That means a deficit of 1.6 percent of GDP and a debt ratio of 130.8 percent.

“We aim not to worsen our structural-budget situation, possibly to improve it, which clearly implies a threshold for the public deficit,” Tria said, speaking in his office in central Rome on Wednesday. Next year’s deficit “might be higher” than the 0.9 percent target set by the previous government, he said.

Bond Yields

Italian bond yields rose in late May as weeks of political uncertainty over the formation of a government and the risk of early elections that would have been seen as a referendum on euro membership rattled financial markets.

The 10-year yields have come off the recent highs but are still well above the average 1.9 percent seen in the first four months of the year. The 10-year yield rose slightly to 2.67 percent Thursday morning from 2.65 percent.

Markets also worried about the cost of the government’s program, which was published before the cabinet was sworn in. Full implementation of the program, which also includes a review of the pension system allowing for earlier retirement, could cost as much as 126 billion euros ($147 billion) in its first year, according to Carlo Cottarelli, a former International Monetary Fund executive who nearly became premier himself.

Asked about the funding for those government measures, Tria said that this month the Treasury will undertake simulations and analyses that will allow the government to set its new public-finance targets by the end of September.

--With assistance from Giovanni Salzano, Zoe Schneeweiss and Ross Larsen.

To contact the reporters on this story: Lorenzo Totaro in Rome at ltotaro@bloomberg.net;Simon Kennedy in London at skennedy4@bloomberg.net

To contact the editors responsible for this story: Fergal O'Brien at fobrien@bloomberg.net, Alessandra Migliaccio, Kevin Costelloe

©2018 Bloomberg L.P.