Italy's Wondrous Bonds Cover Up Budget Challenges Ahead

Italy's Wondrous Bonds Cover Up Budget Challenges Still Ahead

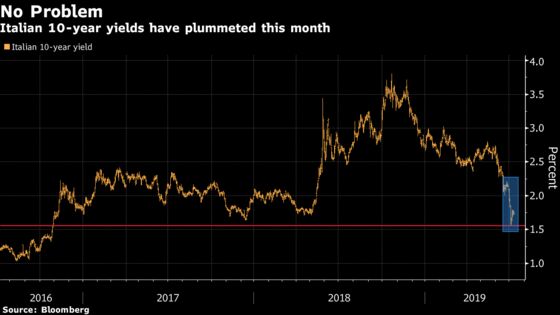

(Bloomberg) -- Looking at Italy’s debt market, you’d be forgiven for thinking that the embattled nation’s problems were firmly behind it.

Bonds had their best week in more than six years, and yields are at their lowest since 2016, prompting the government to lock in bargains by issuing 50-year debt on Tuesday. The driver isn’t budget prudence, but the prospect of the European Central Bank restarting quantitative easing, providing a guaranteed buyer of Italian debt.

The risk is that the market backdrop emboldens Deputy Prime Minister Matteo Salvini to push his aggressive tax cuts. That could revive tensions that roiled the country’s markets after the coalition government took office in mid-2018, particularly as the coming year’s budget will be even tougher.

“The wind is in your sails if you do want to be long Italian bonds,’’ said Richard McGuire, head of rates strategy at Rabobank. “But low yields give Salvini a completely free hand if he wants to play to the home crowd and appear to be driving a hard bargain” with the EU.

Italy avoided European Commission punishment over its budget deficit last week, but its 2020 plans remain an issue amid a sluggish economy. While industrial production rebounded more than expected in May the country is forecast to narrowly avoid recession in 2019 and slowly pick up the following year, according to the EU’s latest forecasts.

To fulfill its promises, the government needs to find 23 billion euros of new revenue or spending cuts to prevent an automatic sales tax increase next January. The EU wants more savings on top of that.

But Salvini, leader of the League party, has promised a “fiscal shock’’ with radical tax cuts next year to jump-start the economy. That’s at odds with Finance Minister Giovanni Tria’s reassurances on fiscal discipline.

The other risk is the ECB not delivering on stimulus. Its next policy gathering is July 25, though economists don’t anticipate a QE relaunch until September. Fitch, which rates Italy’s debt just two steps above junk, will review the country in early August.

For now, investors are buying the rhetoric coming out of Italy, or at least can’t afford not to. Yields are still substantially higher than elsewhere in the region, with those on benchmark German bonds now only a fraction above the ECB’s minus 0.4% deposit rate. Italy’s 10-year yield is about 1.7%.

NatWest Markets are among a number of banks still recommending Italian bonds.

“The fact that Mr. Tria has been allowed to work quietly with the Commission and come to an agreement is a positive signal that goes beyond merely buying time,” strategists Giles Gale and Imogen Bachra wrote in a note to clients.

There are signs that Salvini may have other ideas.

The same day ECB President Mario Draghi said that bond buying could resume, Salvini raised the topic of so-called mini-bills, which some fear might be a precursor to an alternative currency. Ten-year yields still fell nearly 20 basis points.

“The market simply didn’t hear him,” said Rabobank’s McGuire. “As long as the hope and expectation of ECB stimulus remains, then I think the path is open for yet tighter Italian spreads.”

--With assistance from Alessandro Speciale.

To contact the reporters on this story: John Ainger in London at jainger@bloomberg.net;Lorenzo Totaro in Rome at ltotaro@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Fergal O'Brien, Jerrold Colten

©2019 Bloomberg L.P.