Italy’s Got One Shot to Make Good on Its Bond-Market Lifeline

Italy Gets Rare Chance From Bond Markets to Sort Out Its Issues

(Bloomberg) -- Just looking at Italian bonds, observers would have little clue about the nation’s dire economic situation.

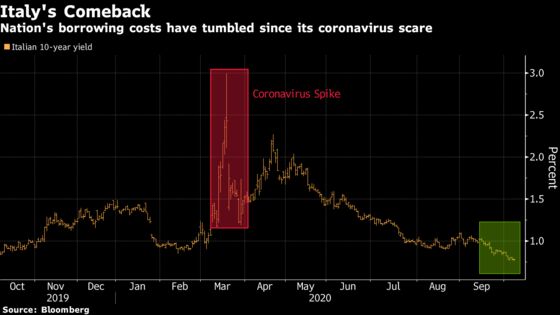

Instead of trading as though its credit rating is on the precipice of junk status, the debt is acting more like a haven, according to Moody’s Analytics data. Italy’s coalition government can raise money for 10 years at 0.76%, a whisker above a record low. The spread over German bonds, a key gauge of risk, is the narrowest in years.

But little has changed on the ground. Italy is weathering its worst recession since World War II, its debt load has spiraled near 160% of the economy’s size and two of the top credit-rating agencies rank the nation just above non-investment grade. And now a resurgence in coronavirus cases is sweeping across Europe.

Its lifelines have been unprecedented bond-market support from the European Central Bank and the prospect of aid from the European Union’s planned recovery fund, helping to make Italy’s bonds the euro zone’s best performers in the third quarter.

“Clearly there are big differences between our ratings and the bond-implied rating,” said Kathrin Muehlbronner, lead sovereign analyst for Italy at Moody’s Investors Service.“Italy needs to use this opportunity.”

Data from Moody’s Analytics, a partner entity, show Italian bonds are trading as though they’re rated A2, similar to Ireland, rather than their own Baa3 grade. Italy’s three-year yield fell Thursday to a record low of minus 0.206%.

Turning around the euro area’s third-largest economy won’t be easy. For much of this century, it has seen anemic growth relative to peers. The government’s own projections have the economy shrinking 9% this year amid the pandemic and expanding only 1.8% in 2021 under a worst-case scenario.

“When others in the euro zone grow at 2%, Italy grows at 1% and if the others grow at 1%, then Italy barely grows,” said Muehlbronner.

EU Cash

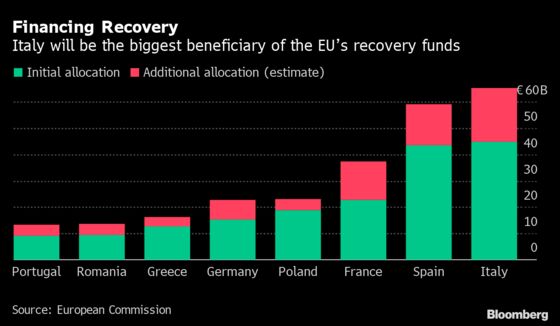

Italy is likely to receive as much as 209 billion euros ($246 billion) in grants and loans from the bloc, making it the top beneficiary of the recovery fund, which aims to get the money flowing next year.

Rome has plans to invest EU cash in digitalization, infrastructure, schooling, de-bureaucratization and job programs, but it needs to act quickly in order to meet its goal of bringing the debt ratio down to 151.2% in 2023. The EU has stipulated that at least a portion of the money must be spent on green projects.

“Recent government choices seem to point more toward supporting demand through a plethora of bonuses and cash benefits, often unrelated to sectors more impacted by the crisis,” said Rosamaria Bitetti, an economist and lecturer at Luiss University in Rome. “We hope the EU will provide stricter guidance on spending during a systemic crisis to avoid the risk of wasting resources.”

For Moody’s, which is set to review Italy Nov. 6, the hurdles the nation needs to overcome are still significant, including heavy bureaucracy and large wealth gaps between its north and south. A downgrade to junk could see the its bonds removed from key indexes, spurring a flood of forced selling. Fitch Ratings, the other agency that ranks Italy just above non-investment grade, reviews the rating on Dec. 4.

Lower Yields

Another risk is that the EU’s planned 750-billion-euro economic recovery fund could fail to materialize. If that happens, the delicate balance in Italy’s debt market could be undone.

“Should we enter December with no progress” on the recovery fund “and no visible path toward a compromise, while being unsure about ECB policy for 2021, markets could start to reprice more meaningfully,” strategists at Bank of America including Sphia Salim wrote in a note. “A breakdown in negotiations would easily see markets test not just 2020 but 2018 wides,” they said, referring to the Italy-Germany yield spread.

Still, investors are more upbeat than they have been in a long time, thanks largely to the ECB, which owns over a fifth of Italian debt, according to NatWest Markets. In effect, the central bank is a guaranteed buyer should things go awry -- a sudden political upheaval, for example -- and Goldman Sachs Group Inc. expects the institution to further boost its stimulus package this year.

Aviva Investors is among those who see room for Italy’s borrowing costs to drop further, in spite of its mounting liability load. Indeed, Japan provides an example of a heavily indebted nation that’s able to borrow at rates close to zero. And investors from the Asian nation, seen as some of the most risk averse, bought a record amount of Italian debt in August.

Joubeen Hurren, a money manager at Aviva, sees the country’s 10-year yield premium over Germany falling below 100 basis points, a level not breached since 2016, from around 130 basis points currently. The gauge surged above 300 basis points during the selloff in March.

“The EU recovery fund is meaningful, in that it can potentially solve or at least postpone debt sustainability issues,” he said, adding that his fund is positioned for a rally in inflation-linked bonds. “The outlook for Italian bonds is quite constructive.”

©2020 Bloomberg L.P.