Investors Glum on Asian Sovereign Bonds as Dollar, Oil Bite

Asia’s sovereign bonds look set to call time on a two-year binge fueled by a tide of cheap money.

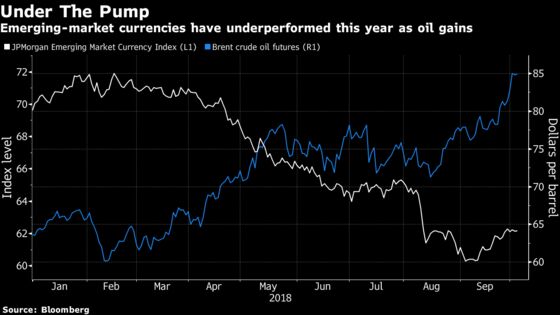

(Bloomberg) -- On track for their first annual drop since 2015, emerging Asia’s sovereign bonds look set to call time on a two-year binge fueled by a tide of cheap money. Investors start the fourth quarter on the defensive, thanks to soaring oil prices, a raging U.S.-China trade war and a stronger dollar.

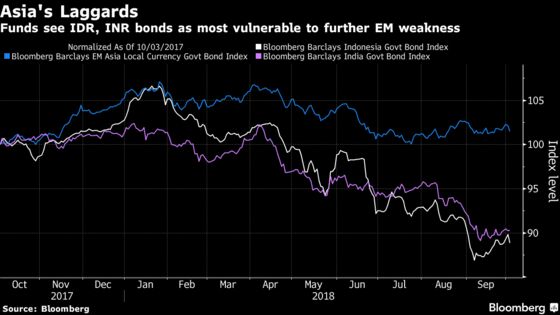

Indian and Indonesian debt will be the most vulnerable as risk sentiment remains fragile, even as policy makers step up efforts to contain the weakness, according to fund managers surveyed by Bloomberg. South Korean and Thai bonds are seen among the safest bets, with the economies’ current-account surpluses compensating for their relatively low yields.

“There is room for some more correction in emerging Asian government bond markets,” said Roland Mieth, Singapore-based emerging markets portfolio manager at Pacific Investment Management Co. “The main driver for this is global factors and the China outlook.”

Thomas Wu, head of Asia fixed income for discretionary portfolio management at Pictet Wealth Management in Hong Kong, agrees. “Until the U.S.-China trade situation is resolved, we’re not really constructive on EM Asian FX,” he said. “For sovereign bonds, we are equally defensive and we’re not seeing an improvement or a turnaround for the time being.”

From a surge in crude oil to a stronger dollar, trade tensions to deficit fears, geopolitical risks to footloose global capital flows, investors face a busy end to the year trying to pick the region’s winners and losers. With the Bloomberg Barclays EM Local Currency Government Asia Index already down 3.6 percent this year, they may face a further headache after Treasury yields rallied to a seven-year high Wednesday.

Here’s a look at what some see in store for emerging Asian government bonds:

India

Indian sovereign bonds are down 12 percent so far in 2018, erasing last year’s gain as the rupee set a succession of record lows. Once favored for their high yields, rupee notes have lost their shine as a rally in crude prices threatens to inflate India’s oil import bill and worsen a current-account shortfall which stands at a five-year high.

Policy makers are set to raise interest rates for a third time this year on Friday, adding to a recent flurry of measures aimed at shoring up the currency. As oil marches toward the $100 mark for the first time since 2014, analysts warn costlier crude will further stoke inflation and hurt sentiment toward a market that’s already reeling from a rare default at a local lender.

“If the oil price continues to go up, that will continue to weigh on the current-account balance and add to further weakness,” said Alexandre Bouchardy, Head of Asset Management Singapore at Credit Suisse Asset Management. “It’s hard to say how much more interest rates have to rise as it depends on where oil prices go, but probably anything between 50-200 basis points from current levels.”

Indonesia

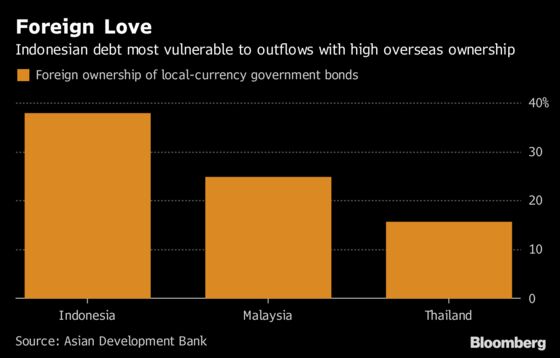

With yields of around 8 percent -- the highest in Asia’s major markets -- rupiah sovereign bonds were once a magnet for global funds. Indonesia is now regarded as among the most susceptible to outflows due to the substantial foreign ownership of its bonds.

Global funds hold more than a third of Indonesian government debt, compared with just over a quarter of Malaysian securities and under a fifth of Thai bonds.

Rupiah bonds are also suffering from the same ailment that’s plaguing their Indian peers: a widening current-account shortfall, which swelled to a four-year high in the second quarter.

“About 20-25 percent of Indonesia’s government borrowings are in U.S. dollars so Indonesia, more than any other Asian government, is subject to changes in U.S. rates, the U.S. dollar and external conditions,” said Brad Gibson, head of Asia-Pacific fixed-income portfolio management at AllianceBernstein LP in Hong Kong. “Once the external environment improves, then rates can actually rally quite strongly in Indonesia as there is no domestic reason for the central bank to continue to hike.”

Malaysia

As the only net exporter of energy among Asia’s major EM economies, Malaysia stands to benefit from the rise in crude prices. Oil contributes just under a fifth of revenue, and higher prices will provide a buffer for the nation’s bonds.

Inflation has cooled after the authorities scrapped a consumption tax in June while concerns about the government’s debt levels have eased. The ringgit lost about 2 percent this year, compared with declines of 10 percent for the rupiah and almost 13 percent for India’s rupee.

“Malaysian government bonds have been quite stable and we are slightly positive. They have high real interest rates and inflation is contained,” said Bouchardy at Credit Suisse Asset Management. “The only potential thing to monitor is the proportion of the foreign ownership of the local-currency bond market. It’s still high.”

Philippines

Philippine bonds were the region’s worst performer last quarter, with a loss of almost 5 percent. The peso slumped to the lowest since 2005 last month amid worries about the nation’s current-account deficit and a perception that the central bank was behind the curve in tackling inflation.

The negative sentiment may ease after Bangko Sentral ng Pilipinas raised its benchmark interest rate by half a percentage point for a second consecutive meeting in September. Policy makers have also pledged to do what’s necessary.

Read more here on the underperformance of Philippine bonds

For AllianceBernstein -- which has been underweight Philippine bonds for the past five years -- peso yields may be approaching attractive levels.

“Philippine bond yields are around 6 percent and the BSP has become more aggressive with tightening,” said Gibson at AllianceBernstein. “Philippine bonds will start to look attractive for the first time in many years as the yield you can earn on the Philippine peso is sufficient for the volatility you may incur.

Thailand

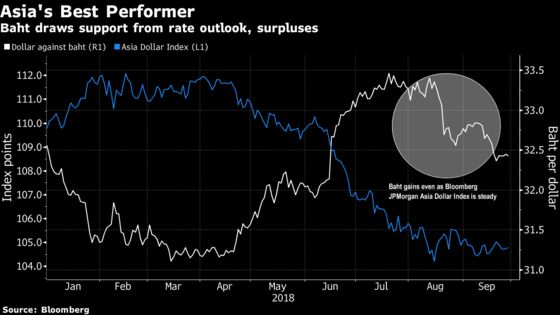

As funds soured on risk assets, Thai bonds offered a safe -- if somewhat unexciting -- proposition. A sizable current-account surplus and a relatively low level of foreign ownership of its bonds mean that Thailand has been less exposed to the volatility buffeting regional markets.

Thai bonds attracted more than $7 billion this year, after drawing $10.6 billion during the whole of 2017. The baht has held steady against the dollar this year, and is the region’s best performer. Still, investors seeking refuge in Thai debt have to contend with yields that are below that of U.S. Treasuries.

“Thailand is a very low-yielding market,” said Bouchardy at Credit Suisse Asset Management. “There are no inflation pressures, current account is in surplus, interest rates are low but it is hard to envision high returns for this market.”

South Korea

South Korean bonds have drawn almost $37 billion of inflows this year, second only to China among eight regional markets tracked by Bloomberg. Funds are staying put in Asia’s fourth-largest economy, as a decent but unspectacular pace of growth means the central bank is unlikely to embark on an aggressive tightening cycle.

Investors are also deriving comfort from the nation’s current account surplus which rose to $8.8 billion in July, the widest in 10 months, and a stockpile of foreign-exchange reserves that are at a record high.

“If you look at countries with current-account surpluses and larger onshore markets, you will expect those countries to be more resilient and this includes China, South Korea and Singapore,” said PIMCO’s Mieth. “But if U.S. Treasury yields move higher, no market in the region will be able to rally.”

--With assistance from Masaki Kondo and Yudith Ho.

To contact the reporter on this story: Liau Y-Sing in Kuala Lumpur at yliau@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Cormac Mullen

©2018 Bloomberg L.P.