Investors Wary as Political Uncertainty Persists in Thailand

Investors are hesitating to invest in Southeast Asia’s second-largest economy because of political upheaval.

(Bloomberg) -- When Kulthirath Pakawachkrilers had to convince yet another Chinese investor that business was still a good bet in Thailand despite the political upheaval, she knew it was going to be a tough sell.

Companies once considering investing in Southeast Asia’s second-largest economy were now looking at other options -- and the uncertainty surrounding the aftermath of the elections was driving much of the concern, said Kulthirath, chief executive officer of the Thailand e-Business Center, which advises companies on entering the Thai market.

Kulthirath, who’s also on the committees of the Thai Digital Trade Association and the Thai e-Commerce Association, has met with more than 600 foreign investors in the past year. She said the majority had decided now is not the right time to invest in Thailand.

“They are hesitating,” Kulthirath said from her office in Bangkok. “Half of them are very worried, especially the Chinese because their economy slightly relies on the government too, so they say that the more a government is strong, the more that a country is strong.”

The decades-long power struggle between the country’s pro-military allies and opposition parties is threatening to further unhinge an already fragile economy, even with a new government headed by former junta leader Prayuth Chan-Ocha about to be sworn in.

After five years of military rule, the junta retained control of the government in the March election with only a slim four-seat majority coalition in the House of Representatives. That keeps the bitter political fighting very much alive and makes it difficult for returned Prayuth to pass meaningful legislation.

Currently, 41 members of parliament from the pro-military coalition are facing calls to be disqualified over accusations they broke rules prohibiting politicians from holding shares in media firms. The petition comes from the opposition Future Forward party, whose leader Thanathorn Juangroongruangkit is himself suspended from parliamentary duties pending the court’s ruling on a similar accusation.

“If all of these lawmakers got suspended or banned, the government won’t be able to push through the vote on any issues in the lower house,” said Punchada Sirivunnabood, an expert on Thai politics and a visiting fellow at Singapore’s ISEAS-Yusof Ishak Institute.

Political risk is making businesses hesitant to invest in an environment of heightened global challenges. Already $20 billion of spending on transport and logistics projects has been delayed because of the three-month impasse in forming a government.

‘Limited Power’

The economy “is facing key risks from both the U.S.-China trade war and Brexit. We need the government to steer the economy through these problems,” said Kriengkrai Thiennukul, vice chairman of the Federation of Thai Industries. “Without the government, all businesses are in a wait-and-see mode and government officials have limited power to work.”

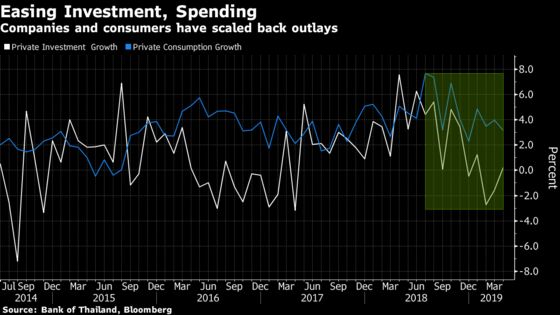

The political uncertainty is a shadow over an economy whose growth potential has gradually declined over the years. The export-heavy manufacturing industry has lost market share to low-cost neighbors like Vietnam, productivity has steadily declined and the nation has one of the oldest populations among developing countries. That’s even before trade wars and a global slowdown are factored in.

Lucrative free trade talks have languished under military rule and there’s urgency to get those going again.

Negotiations for a free trade agreement with the European Union were suspended back in 2014 after the junta overthrew the democratically elected government, straining relations with Thailand’s third-biggest trade partner. While the EU went on to restore political ties with Thailand in 2017, there is no signal the two sides will resume negotiations for an agreement they spent more than a year working on.

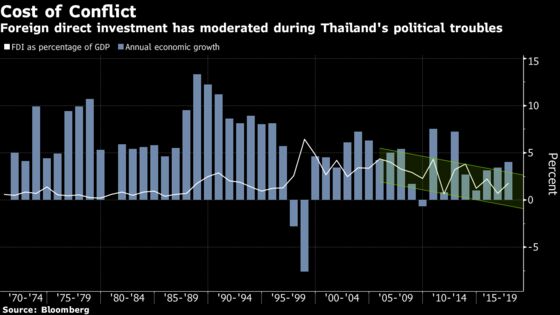

FDI Slump

“Many countries have used our military government as the reason for suspending the talks,” Kriengkrai said. “Once we return to democracy, we need to move quickly.”

Approved foreign direct investment from EU companies has plunged 32% since 2014 to just $1 billion last year, according to data from the Thai Board of Investment. Overall FDI rose 0.5% in April from a year ago, after declining in the previous two months, latest figures from the Bank of Thailand show.

“The political uncertainties are probably the greatest factor of all for the manufacturers who are thinking of investing or have already invested in manufacturing in Thailand,” said Karri Kivela, executive director of the European Association for Business and Commerce.

Slower investment growth and the worsening trade outlook will curb economic growth, which the central bank says may come in lower than its 3.8% forecast for the year -- already among the weakest in Southeast Asia.

Economic Advantages

Although it’s losing out to regional peers like Vietnam as businesses shift supply chains amid the U.S.-China trade war, Thailand still offers a number of advantages over its less-developed neighbors -- especially in the vehicle industry, where Subaru Corp. and Harley Davidson Inc. have expanded operations.

Micah Shepard, president of Southeast Asia at German-based automotive parts maker Schaeffler Manufacturing Co. Ltd., said Thailand “has the full supply base of everything you more or less need to make your product,” which gives it a “big advantage” over Vietnam. Schaeffler Manufacturing has factories in both countries after opening a $50 million manufacturing plant in Vietnam’s Bien Hoa last month.

Thailand is hoping to win over investors as a one-stop-shop business hub with its signature project, a $54 billion infrastructure project along the eastern seaboard, which would see new industrial zones supplemented by a high-speed railway, an expanded airport and deeper ports.

Kanit Sangsubhan, secretary general of the Eastern Economic Corridor, said projects are proceeding, with a contract to build a $7 billion high-speed railway connecting three major airports already secured. “Within the next month we might be able to pass another two or three projects at the same time,” he said.

For investors, a stable government able to deliver on these investments is crucial for the economy.

“Deep down inside they want certainty,” said Kulthirath. “We pray for it.”

--With assistance from Suttinee Yuvejwattana, Natnicha Chuwiruch and Siraphob Thanthong-Knight.

To contact the reporter on this story: Philip J. Heijmans in Singapore at pheijmans1@bloomberg.net

To contact the editors responsible for this story: Ruth Pollard at rpollard2@bloomberg.net, Nasreen Seria

©2019 Bloomberg L.P.