Inside the PBOC’s Struggle to Balance China’s Growth and Debt

Even with worsening data pointing to the risk of a sharper decline, the PBOC is staying the course, for now.

(Bloomberg) --

Deep in the government compound in Beijing, China’s State Council was in session, debating a complicated proposal to help struggling domestic companies.

The cabinet meeting in Zhongnanhai, a walled expanse of ornamental lakes and pavilions adjacent to the Forbidden City, took place late in May, days after U.S. President Donald Trump heaped yet more tariffs on China’s exports and restricted the sale of goods to Huawei Technologies Co.

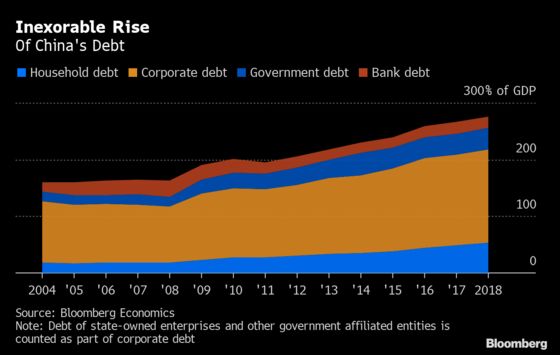

On this day though, officials were grappling not over the fallout from the trade war, but how to tackle a home-grown adversary: about $35 trillion in corporate, household and sovereign debt.

An official from the National Development and Reform Commission, the modern-day incarnation of the once-mighty State Planning Commission, was suggesting that the People’s Bank of China should release a bolt of cash that could be used by banks to buy stakes in companies, which would then use those funds to repay some of their debt.

The central bank governor Yi Gang was present at the meeting, but before he could speak, Premier Li Keqiang dismissed the proposal on the grounds that yet more central bank liquidity wasn’t the answer.

For Yi, it was one more small victory. In his 20 months in office, the University of Illinois alumnus has persistently argued against a “flood” of stimulus, instead releasing just enough liquidity to keep the economy on its gradual glide path from the double-digit growth rates of the mid-2000s toward the sub-6% rates expected into the 2020s.

Even with worsening data pointing to the risk of a sharper decline, the PBOC is staying the course, for now. While the U.S. Federal Reserve has slashed broad borrowing costs by 75 basis points since July, the PBOC is maintaining the most gradual of approaches, constrained by the fear of re-inflating debt bubbles or stoking already resurgent inflation.

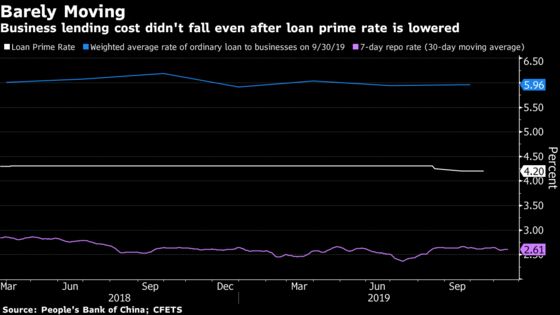

That approach has been confirmed this month. A 5 basis point cut to the key 7-day reverse repo rate on Nov. 18 followed a tweak of similar magnitude to the rate the PBOC charges banks to borrow for a year. The loan prime rate -- based on the interest rate for one-year loans that 18 banks offer their best customers -- was set at 4.15% for November, down from 4.20% in October, according to a statement from the PBOC on Wednesday.

For the global economy, which has relied on China for about a third of its total growth in recent years, Yi’s moderation has meant there will be no big support to world demand that marked past binges from Beijing. If Yi can pull off his tightrope walk between keeping growth stable and avoiding a debt crisis, China will continue its march toward being the “moderately prosperous” society that the Communist Party wants it to be. Fail, and all bets are off.

Yi is building on the work of his predecessor, Zhou Xiaochuan, who in the latter years of his tenure argued that controlling debt had become more important than hitting sky-high economic growth rates. That insight appears to have become internalized at the highest levels.

“The balance between debt and growth is a task that Chinese policy makers will need to address over the longer term, for 10 years or more, unless there can be fundamental structural reform to get rid of some of it,” said George Wu, chief economist at Changjiang Securities Co in Beijing, who served 12 years in the PBOC’s monetary policy department. “Otherwise, the debt will just be rolled over, not removed, like an ostrich burying its head in the sand.”

From his office at the bank’s headquarters -- a squat office block at the gateway to Beijing’s financial district covered in bronze reflective glass -- Yi is also trying to continue Zhou’s decade-and-a-half quest to modernize the institution from its roots as the only bank in Maoist China to one of the must-watch monetary guardians of the world.

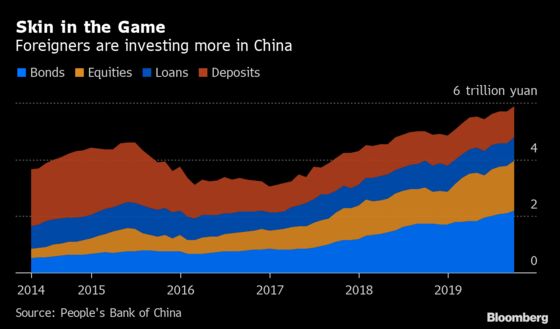

Foreigners are already more invested in China’s economic future than ever before, and that’s only set to deepen as its financial barriers come down. In September, executives from JPMorgan Chase & Co., and Goldman Sachs Group Inc. were among outsiders that met with Yi and other regulators at the Ritz-Carlton Hotel about a kilometer from the PBOC headquarters -- evidence that the trade war has done little to derail the rush to gain a share of an estimated $9 billion in annual profits.

International investors are already directly exposed to the ups and downs of its stock market through indexes like MSCI Inc’s and are set to own as much as 20% of its sovereign bonds by 2023 according to Citigroup Inc. As those asset prices swing around on PBOC actions, global investors will demand more transparency from Yi, and he’ll need to provide it if he wants to keep the money pouring in.

Hampering Yi’s ability to explain his policies and pave the way for any change in direction is the fact that he doesn’t have the formal independence enjoyed by the world’s other major central banks. While day-to-day operations such as liquidity management in money markets are assumed to be at the PBOC’s discretion, it’s the State Council that has the final word on benchmark interest-rate settings.

Indeed, opacity is a feature of the policy-making process in China, not a bug. Unlike the formally independent Fed or European Central Bank, the PBOC must painstakingly build consensus for its proposed course of action with a range of other ministries, and then win approval from the top leadership.

For now, the leadership is on his side. Yi’s boss is the silver-haired Liu He, who’s been leading the nation’s trade negotiations with the U.S. Liu is widely believed to have been the “authoritative person” interviewed in a landmark piece in the nation’s flagship People’s Daily back in 2016 arguing policy makers should prioritize de-leveraging ahead of short-term economic growth. In a somewhat complex structure, Guo Shuqing, a high-profile banking regulator, is the Communist Party’s secretary for the PBOC.

The bureaucratic system of policy making, known as “countersignature,” means that debates with the rest of government are just as important as those within the central bank. To maintain room for negotiating, very little is let into the public domain about how policy makers think before an initial consensus is reached. Where investors can pick over the details of the ECB or Bank of Japan’s economic modeling and the viewpoints of officials, the PBOC’s internal procedures are confidential like those of any Chinese government ministry.

As a result, investors can be wrong-footed, sometimes dramatically. Like the botched yuan devaluation of 2015 that sent global markets plunging. Or, to a lesser extent, a bond rout this year due to dashed expectations of larger stimulus that has yet to arrive.

“For China to properly make its financial markets more international, the PBOC ought to take the lead to adopt a more proactive and international posture in communicating with their ‘clients,’” said Stephen Jen, founder and co-chief investment officer of Eurizon Slj Capital. “Sometimes the timing and the nature of the actions taken by the central bank confuse the market as they are not accompanied by any statements or explained in speeches.”

The PBOC, NDRC and State Council declined to comment on the content of the cabinet meeting. The PBOC did not grant a request for comment on monetary policy and transparency issues. Governor Yi conducted his first interview with foreign media with Bloomberg Television in June.

A sliver of light is beginning to penetrate the black box. The central bank widely consulted and spoke publicly about a reform of the interest-rate system introduced this year and its daily liquidity operations are now accompanied by commentary on the PBOC’s view of the market. More press conferences with foreign media attending have been held this year than before, and more information is also released in English.

But market participants still have to guess the timing and content of major liquidity operations. There are no regular policy meetings that decide on official interest rates. And the interest-rate reform has added to the complexity of the central bank toolkit and left observers with even more policy levers to keep an eye on without any single one being decisive.

When Yi has spoken publicly, investors would have done well to listen. In an interview with Bloomberg News in June, Yi warned against that “flood” of liquidity and signaled officials weren’t wedded to defending any particular level of the yuan. The nation’s currency weakened past 7 per dollar about two months later and he’s kept his word on stimulus restraint.

Barring some unforeseen crisis, like a marked worsening in the trade standoff with the U.S. or a blow-up in the property market, Yi appears set to continue his tightrope walk.

“Starting with Governor Zhou and continuing with Yi Gang, they have convinced the top leadership that it is very important to reduce financial risks,” said Nicholas Lardy, a senior fellow at the Peterson Institute for International Economics in Washington. “It would appear President Xi Jinping has bought the idea.

| This is the third in a series of stories on the challenges facing Asia’s biggest central banks. CLICK HERE to read about the Reserve Bank of India’s struggle to juggle its multiple roles. CLICK HERE for a story on the Bank of Japan’s struggle to reflate the economy. |

|---|

To contact Bloomberg News staff for this story: Yinan Zhao in Beijing at yzhao300@bloomberg.net;Jeffrey Black in Hong Kong at jblack25@bloomberg.net

To contact the editors responsible for this story: Malcolm Scott at mscott23@bloomberg.net, James Mayger, Jeffrey Black

©2019 Bloomberg L.P.

With assistance from Bloomberg