(Bloomberg Opinion) -- Congratulations, New Zealand. Your Reserve Bank owns its message and, just as importantly, follows through. There's a lesson there for other central banks wrestling with squishy growth and inflation consistently short of target.

As painful as this is for me to admit as an Australian, the Reserve Bank of New Zealand made the right call Wednesday by lowering interest rates. The Aussie central bank, by comparison, held its benchmark a day earlier, releasing a statement that struck some as more upbeat than easing-friendly.

New Zealand clearly flagged a cut in its March statement and delivered it promptly at this week's conclave. The step is all the more noteworthy given this was the first decision from a proper monetary-policy panel. Until now, the RBNZ governor essentially ruled as a monarch. While the Kiwis were late to decision-by-committee, it was an impressive debut.

The Reserve Bank of Australia has been edging toward a trim since the start of the year without fully owning it rhetorically. The central bank’s projections, the trajectory of inflation and overall economic activity pointed to a cut.

Yet Governor Philip Lowe demurred even as a majority of economists – albeit a thin one – tipped lower borrowing costs. The RBA's statement makes you wonder if it was even seriously considered. None of the usual signals were sent to warn off those forecasts in the lead-up to Tuesday.

As intense as the trans-Tasman rivalry can be, there's more at stake here than fraternal competition. The decisions have real world consequences; the currencies of the Antipodean two are among the most actively traded and both central banks have won plaudits at various stages for innovation, in the case of New Zealand, or the durability of that (yawn) 28-year run of growth in Australia.

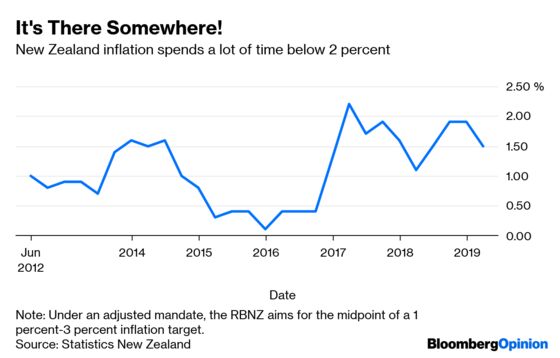

Inflation has been consistently below target in both economies, as it has in much of the world. What to do about it has been a hot topic in monetary salons. The deliberations have added tension given global economic activity appears to be at an inflection point: Things slowed significantly at the end of last year into the first quarter, but lately have been looking a bit rosier, particularly in China and the U.S. The question of whether to cut rates has a “should I stay or should I go” quality to it.

Throw in official rates that are already at or close to historically low levels and you have quite the pickle. If you have an inflation target, must you adhere to it? Or do you hesitate, mindful of how to deploy the limited ammunition you have – all the while conscious that Japan and Europe could have been bolder sooner in combating stagnation?

You can hear the chords of this dilemma in Federal Reserve Chairman Jerome Powell's halting efforts to describe the too-low inflation phenomenon. One day it's an existential challenge; the next it's a passing shower.

In Australia's case, some observers pointed to a national election next week as a reason to hold off. I don't entirely buy that, given the RBA has acted during political seasons in the past. We'll get more information when the RBA publishes commentary and forecasts on Friday and minutes of Tuesday's deliberations in a few weeks.

In the meantime, New Zealand can take some time in the sun.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Daniel Moss is a Bloomberg Opinion columnist covering Asian economies. Previously he was executive editor of Bloomberg News for global economics, and has led teams in Asia, Europe and North America.

©2019 Bloomberg L.P.