(Bloomberg Opinion) -- The chipmaker that sounded the starting gun for the industry’s $200 billion run of dealmaking has finally found the sort of transformative takeover that many of its rivals have already realized. The question is whether its patience has paid off.

Infineon Technologies AG agreed a $10 billion deal on Monday to buy Cypress Semiconductor Corp to form the largest supplier of semiconductors to the automotive industry. The Munich-based company’s $2.3 billion acquisition of International Rectifier Corp. in 2014 heralded the subsequent deluge of deals, but was smaller than many of those that followed.

Infineon is paying a generous 46 percent more than Cypress’s average market value over the past 30 days. The stated cost synergies are 180 million euros ($201 million) by 2022. It’s hard to see how their present value covers the $2.8 billion premium to Cypress’s recent average market capitalization. To make it work, the combined entity will need to achieve significant revenue synergies, a factor that’s harder to predict given fluctuations in demand.

Management expects the sales uplift to be a little under 1 billion euros by 2025. That makes it distinctly possible to boost synergies to a level at which the deal would start to make sense financially. But it’s still asking for a leap of faith from investors.

Given the track record of Chief Executive Reinhard Ploss and his team, it’s a leap of faith that might warrant taking. He paid a similar 48 percent premium for International Rectifier, but both Infineon’s share price and Ebitda have doubled in the intervening years.

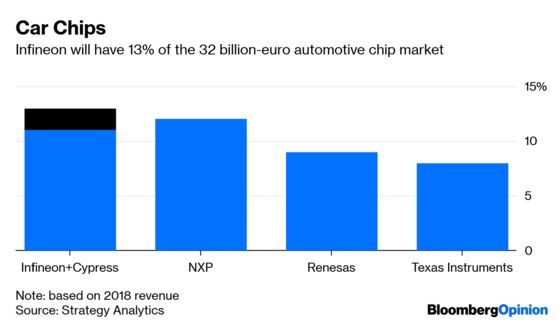

The two firms’ businesses are complementary. Cypress will add automotive capabilities for self-driving car systems and vehicle communications, making the new Infineon the world’s largest automotive semiconductor supplier, based on 2018 sales. It will also diversify the purchaser’s product offering away from the power management chips which are its traditional strength.

A lot is being asked of investors here. The shares fell 8% on Monday, largely because Infineon has said it partially plans to fund the deal with a sizable equity issue. The need for equity funding means the buyer is draining its M&A firepower for the time being, potentially costing it other opportunities.

The biggest sticking point might be the Chinese regulator. Beijing’s Ministry of Commerce will have to green light the deal. That decision is likely to be more political than economic – U.S.-Chinese trade tensions underpinned its failure to approve Qualcomm Inc.’s acquisition of NXP Semiconductor NV, which killed the transaction last year.

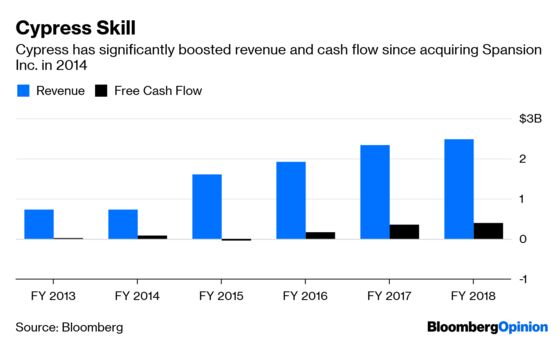

The Chinese factor is tough to predict. Management clearly think the deal warrants the effort of coping with such an imponderable. Now they have to ensure they can deliver on those ambitious revenue growth goals. By waiting, Infineon is buying an asset which is performing far better than it was three years ago, when Cypress’s profitability was pitiful. But it’s paying a significant premium for the privilege.

--With assistance from Chris Hughes.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Alex Webb is a Bloomberg Opinion columnist covering Europe's technology, media and communications industries. He previously covered Apple and other technology companies for Bloomberg News in San Francisco.

©2019 Bloomberg L.P.