Indonesian Bonds Get Further Ahead of India Debt With Policy Gap

Indonesian Bonds Get Further Ahead of India Debt With Policy Gap

(Bloomberg) -- The fortunes of two high-yielding emerging Asian bonds are set to diverge further, with Indonesian notes set to outperform Indian peers driven by central banks’ deviating policies.

The spread between 5-year Indonesia and India sovereign bonds is set to widen from 63 basis points, which is already the highest in more than three years. While Indonesia continues to buy bonds with targeted purchases of 224 trillion rupiah ($16 billion) for 2022, India halted the scheduled bond purchase program last year and has been mopping up excess liquidity.

With inflation a threat and the Federal Reserve forecast to raise rates this year, investors are expected to become more selective of their emerging-market exposure. Indonesian debt, a benchmark for risk appetite, also benefits from more benign price pressures, whereas India has seen a surge to a three-decade high.

Indonesia government bonds will outperform due to the superior real yield buffer, higher nominal yield cushion against rising core rates and improved external balances, according to Duncan Tan, a Singapore-based strategist at DBS Bank Ltd. Meanwhile, India rates will see increased volatility as the central bank withdraws liquidity and as markets price in the pace of rate hikes, he said.

Macro Divergence

Inflationary pressures in the South Asian nation remain higher compared to Indonesia. India’s retail inflation has been rising for two straight months, while the November wholesale price inflation for the country unexpectedly surged to a three-decade high. Investors will get a chance to assess the state of inflation when December retail and wholesale price growth data is released next week.

In comparison, price rises in Indonesia have remained below the central bank’s 2%-4% target for 18 straight months. These two countries offer the highest-yielding debt in major Asian markets.

Treasury 10-year yields have jumped around 30 basis points to above 1.6% since a December low. Markets are pricing in three rate hikes this year by the Fed, while analysts surveyed by Bloomberg see the benchmark yield hitting more than 2% by the fourth quarter.

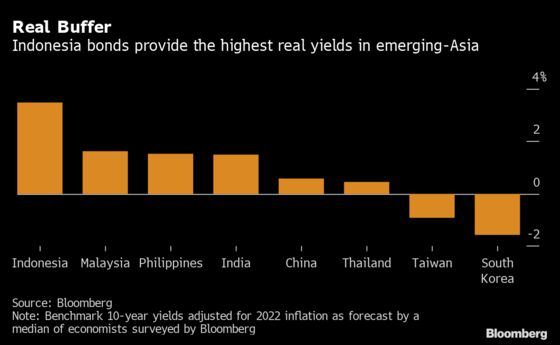

As a result, the Southeast Asian nation offers the highest real yield in emerging Asia, with the 10-year benchmark offering 3.5% after adjusting for 2022 projected inflation, according to a median of economists surveyed by Bloomberg. This provides some buffer against rising U.S. yields.

To be sure, rapid transmission of the omicron variant, which results in more lockdowns, could lead to a more accommodative stance from the Reserve Bank of India. India’s overnight indexed swaps are currently pricing-in around 55 basis points of hikes in the next six months.

The Reserve Bank of India requested primary dealers to rescue a bond sale on Dec. 24, a first in five months, reflecting its uneasiness with rising yields. However, unless there is excessive yield volatility that is disruptive for government financing, the central bank would be comfortable staying on the sidelines, DBS’ Tan said.

©2022 Bloomberg L.P.