India Holds Rates Amid Dissent on Lower-for-Longer Stance

Bond yields rise as RBI steps up variable reverse repo rate auctions.

(Bloomberg) -- Sign up for the New Economy Daily newsletter, follow us @economics and subscribe to our podcast.

India’s central bank kept interest rates unchanged at a record low to support the economy, even as a split appeared among policy makers on continuing with the lower-for-longer stance.

The Reserve Bank of India’s six-member Monetary Policy Committee retained its main repurchase rate at 4% on Friday, as predicted by all 29 economists in a Bloomberg survey. Policy makers voted 5-1 in favor of keeping the stance accommodative, a departure from the past when they were unanimous on the need to support growth amid an impending third wave of the pandemic.

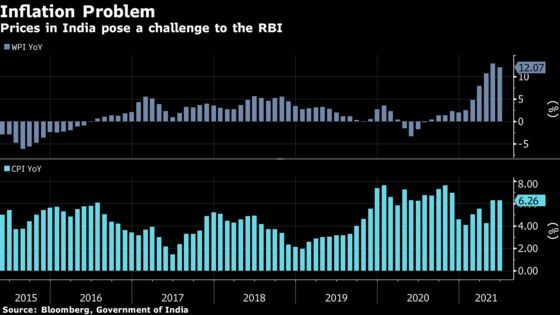

That follows the pace of inflation breaching the RBI’s upper tolerance limit of 6% in the past two months, a trend attributed mainly to supply side disruptions caused by the coronavirus pandemic. While the dissent from MPC member Jayanth Rama Varma isn’t the first, it comes at a time when markets are particularly edgy about any hints on unwinding of the ultra-easy monetary policy.

Read: Bonds in India Decline as Traders See RBI Turning Less Dovish

Last year, Varma opposed a decisive lower-for-longer-rate stance, citing a steep bond yield curve, which, he said, indicated doubts about the RBI’s ability to target inflation in a credible manner. Governor Shaktikanta Das on Friday told reporters to wait for the meeting’s minutes on Aug. 20 for details of Varma’s reservations.

Shorter-dated bonds declined after the dissent vote. The yield on the 5.63% bond maturing in 2026 rose as much as 10 basis points to 5.81%, before paring gains as the RBI said it would also buy government bonds worth 500 billion rupees ($6.74 billion) in August. The benchmark 10-year yield was up three basis points to 6.24%.

Despite the inflationary pressures, Das said the time now was to nurture the “nascent” economic growth, given the recent high-frequency indicators from purchasing managers’ surveys to jobless data showing the recovery was muted.

This “policy meeting finally saw some implicit acknowledgment that continued disregard for inflation ultimately comes at the cost of policy credibility and markets eventually exacting higher risk premia,” said Aurodeep Nandi, an economist with Nomura Holdings Inc. in Mumbai.

While Das raised the inflation forecast to 5.7% for the current financial year, from 5.1% previously, he still maintained that the trend was transitory and the economy needed continued support from all sides -- fiscal and monetary. The RBI was in the “whatever it takes mode” and the government too would step in with support, if needed, he told reporters.

‘May Kill’

“The supply-side drivers could be transitory while demand-pull pressures remain inert, given the slack in the economy,” Das said about inflation. “A pre-emptive monetary policy response at this stage may kill the nascent and hesitant recovery that is trying to secure a foothold in extremely difficult conditions.”

The central bank retained its own growth forecast for the current financial year at 9.5% -- the same pace predicted by the International Monetary Fund. There are risks to that outlook from an impending wave of the pandemic, with forecasters warning a surge in outbreak as soon as this month.

“The major dampener was the one dissent,” said Vijay Sharma, executive vice president for fixed income at PNB Gilts Ltd. “Now it’s 5-1, but the feeling among traders would be that this could be the start of the process, and in future it could become 4-2,” he said.

The central bank also announced enhancing the amount of the so-called variable rate reverse repos to drain liquidity from the banking system in stages, from the current 2 trillion rupees. Still, Das clarified that it shouldn’t be read as a reversal of the accommodative bias.

Das also announced the following measures:

- Extends an on-tap Targeted Longer-Term Refinancing Operations program by three months, allowing more time to banks to lend to stressed businesses

- RBI decided to amend some guidelines on export credit in foreign currencies

- Extends by six months the deadline to hit targeted milestones under debt recast plans to help businesses impacted by the pandemic

©2021 Bloomberg L.P.