India Sends Up the Monetary Helicopters

The gamble aims to make the country a manufacturing powerhouse, but it risks risks a spurt in inflation and a weak rupee.

(Bloomberg Opinion) -- India is making a second big fiscal gamble. The first – a switch from sales to consumption taxes – has failed to achieve revenue targets. The government, which two months ago was trying in desperation to tax everything that moved, has suddenly changed tack and is slashing levies on company profits.

Will this revive animal spirits and sputtering GDP growth, and at what cost to stability? That’s what investors want to know. But another crucial question, one whose answer will resonate globally, is whether the tax cut is going to be financed by newly printed currency rather than debt. In other words: Is this helicopter money?

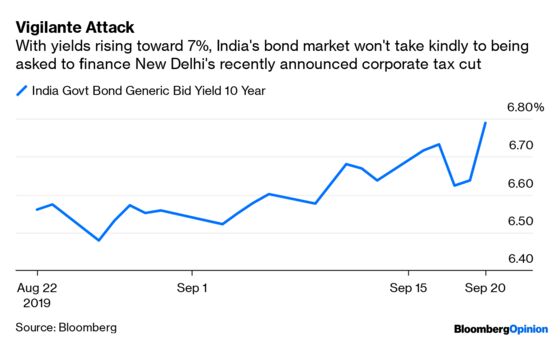

Slashing the government’s take from corporate profits to 25.2% from 34.9% has given a boost to stock-market sentiment, while simultaneously seeding fresh doubts about fiscal profligacy in the bond market.

Equity investors are basing their judgment on a combination of optics and arithmetic. Thanks to exemptions, most Indian firms can keep their tax rate below 30%. Even so, Friday’s cut will mean a 5%-6% earnings lift for firms in the benchmark Nifty 50 index, according to Kotak Securities Ltd. However, it’s only banks and financial firms that may choose to reap the full earnings harvest. They need higher equity prices to raise more capital, expand their loan books and outgrow their bad-debt problem.

Non-financial sectors may respond differently. At 5%, India’s GDP growth is at a six-year low. Manufacturers such as auto and steel companies may opt to cut prices instead of retaining the entire advantage of the lower tax rates.

This is where the equity market’s hopes of a demand stimulus collide with the bond market’s misgivings over fiscal slippage. Even if New Delhi has exaggerated the 1.45 trillion rupees ($20.5 billion) estimated cost of its largess, the government might need to cut spending sharply for a second year to retain any claim to fiscal rectitude. Finance Minister Nirmala Sitharaman has said there are no plans for that. Belt-tightening would hurt final demand more than any stimulus from price cuts would help. Spending cuts could destabilize the economy further, especially if state governments also hit the brakes on expenditure.

Friday’s tax package also offered a 17% profit tax rate for new manufacturing companies. That compares favorably even with low-tax jurisdictions like Hong Kong and Singapore, and gives Prime Minister Narendra Modi a chance to market India – at shindigs like last weekend’s “Howdy Modi” event in Houston – as an alternative to China for export-oriented investments in textile, electronics and autos, especially electric cars and components.

However, for big payoffs, both global demand and the ease of doing business in India must improve. Until then, who will pay for the tax breaks? The printing press.

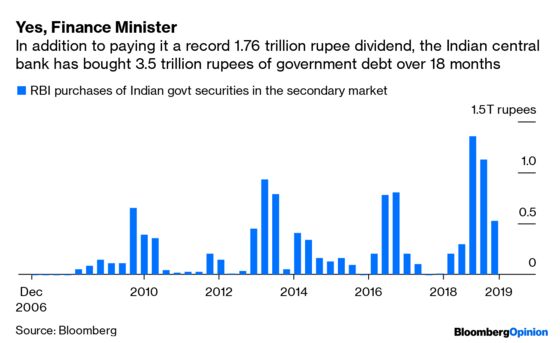

Not only has the Reserve Bank of India bought government bonds worth a record 3.5 trillion rupees in the past 18 months, it has also changed its accounting policy to manufacture a supersize 1.76 trillion rupee dividend for New Delhi. Given how similar that latter amount is to the just-announced tax bonanza, it’s reasonable to ask whether India’s new growth strategy is predicated on tax cuts financed by money creation. As Ananth Narayan, a former Standard Chartered Plc banker-turned-finance-professor has shown, the government could get an even bigger dividend of 2.5 trillion rupees from the RBI if the rupee were to weaken by 5% against major currencies this fiscal year. India is in the middle of an “uncharted print-and-spend cycle,” Narayan wrote before the tax cut.

A money-financed tax cut risks damaging the independence of the central bank by turning it into a junior partner in a fiscal adventure. Helicopter money is a last resort in economies where nominal interest rates have hit rock bottom, and even with quantitative easing the threat of outright deflation lingers. At 5.4%, the policy rate in India is nowhere near the zero lower bound. The problem is a lower-than-targeted inflation of 3.2% because of which real interest rates are too high.

By announcing a splashy tax cut even after the central bank governor said fiscal space to spur the economy was “limited,” New Delhi has unilaterally sent up the helicopter. Keeping it afloat will implicitly become the RBI’s job. If the gamble works, the central bank will be left to cope with a spurt in inflation and a weak rupee. If it fails to revive growth, there’s bound to be renewed clamor to level the playing field between corporate profit and personal incomes with a flat tax.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2019 Bloomberg L.P.