The Case for QE in India Is Getting Stronger

(Bloomberg Opinion) -- With India’s nominal GDP growing at its slowest pace in 17 years, it’s a given that the central bank will cut interest rates again this Thursday.

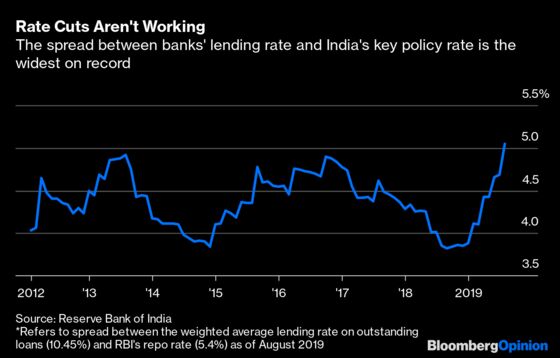

What’s the point, though? Commercial bank lending rates have turned immune to monetary policy, so much so that a sixth reduction this year in the benchmark price of money will make hardly any difference. The only medicine that can work is quantitative easing, a remedy authorities aren’t even discussing. QE may not cure the patient, but it may well succeed in bringing India’s economy out of a coma.

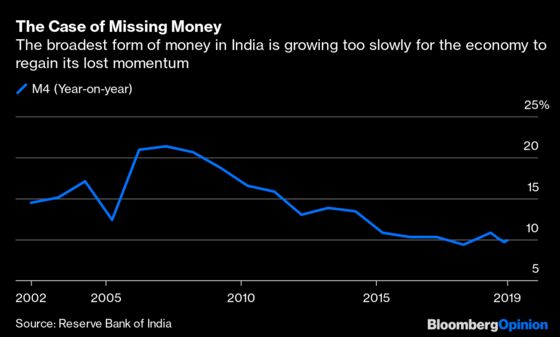

To see why the quantity of money is a bigger problem than its price, consider M4. The growth rate of India’s broadest measure of money supply has collapsed to single-digit levels for some time now, and is refusing to budge. New loans automatically create new deposits in the banking system. But until there are creditworthy takers for fresh advances, deposits won’t revive. Time and demand deposits at banks account for 84% of money supply, so it’s hard for the latter to get a boost without an uptick in the former.

Unconventional asset purchases can make a difference, though not the vanilla Japanese variety in which the central bank buys government bonds from banks for cash, which they stuff into their current accounts with the monetary authority.

This kind of QE does have a couple of advantages. One, it lowers the long-term government bond yield. That reduces loan costs for risky borrowers, since government bond yields act as a benchmark. Two, a more liquid banking system with more low-yielding cash than higher-yielding bonds will be impatient to lend — at least in theory. Yet this type of QE relies on loans being made. If the demand side of the economy is struggling, the impact may be limited because of the one thing it doesn’t do: lift money supply in the broader economy. That’s a point Invesco Asset Management chief economist John Greenwood has made in Japan’s case.

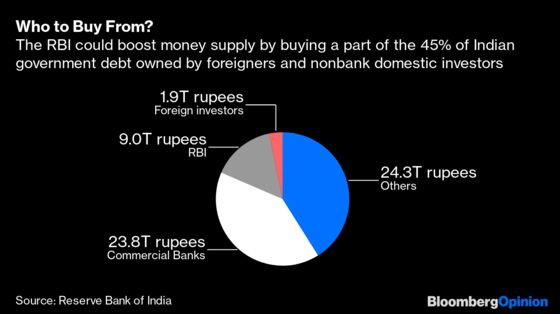

For India, it would help much more for the central bank to buy government bonds from nonbanks, following in the footsteps of the U.S. Federal Reserve, which primarily purchased securities from hedge funds, broker-dealers and insurance companies. Since nonbank sellers of bonds don’t have accounts at the Reserve Bank of India, they’ll deposit any cash they receive with commercial lenders. Money supply would accelerate even without new loans being made.

That may be quite useful in India’s current circumstances. Banks, shadow lenders and India Inc. are all suffering from what Nomura Holdings Inc. economist Sonal Varma calls the “triple balance sheet problem.” The Indian government is already helping itself to practically all of the household sector’s savings. It doesn’t have more scope for deficit spending. In any case, borrowing at a higher cost than the nominal GDP growth rate would only swell the national debt.

If nothing else, a more liquid nonbank sector would want to buy new government debt to earn a yield. New Delhi’s financing constraints would ease, allowing for a round of fiscal pump-priming that hopefully would create new machinery and project orders for the private sector, ending years of gloom around investment.

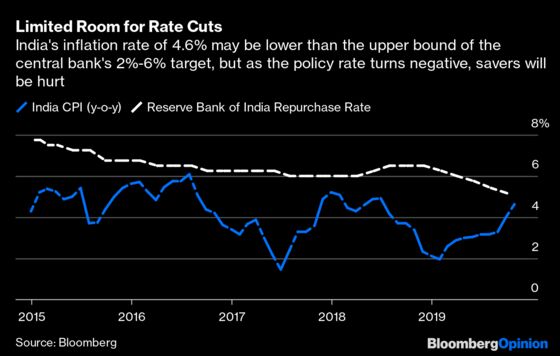

If the RBI thinks of asset purchases as a way to further reduce the price of money, then it will want to wait until it has exhausted its conventional firepower by cutting the 5.15% policy rate further. Given the primacy of food and fuel in India's inflation, which is currently hovering at 4.6%, policymakers have some limited elbow room. But if the central bank views asset purchases as a way to influence the waning quantity of money, then it should act now. Doing so may well save the day.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2019 Bloomberg L.P.