In High-Yield Revival, Global Funds Prefer Indonesia Over India

The archipelago’s debt is more attractive due to a superior fiscal outlook.

(Bloomberg) -- Indonesian bonds appear more promising than India’s in a contest between Asia’s high-yield heavyweights, according to two of the world’s biggest investment funds.

The archipelago’s debt is more attractive due to a superior fiscal outlook and the greater potential for currency strength, says JPMorgan Asset Management, which oversaw $1.9 trillion globally at the end of March. Indonesia’s bonds also have more upside than India’s after suffering more heavily in the virus sell-off, according to BNP Paribas Asset Management.

“We favor Indonesian debt since we reckon that fiscal challenges are less severe there,” said Julio Callegari, lead fund manager for Asia local rates and currencies at JPMorgan Asset in Hong Kong. “We hold a small position in India debt that we don’t intend to increase. In Indonesia we hold a larger position and our bias is to increase it.”

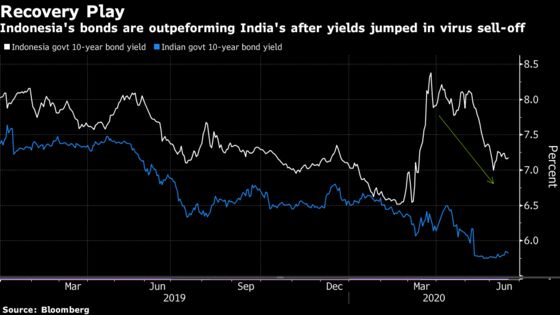

The debate among investors over the relative merits of Indonesian and Indian bonds illustrates the shift in markets that has taken place in recent weeks. Risk assets largely rallied across the board in April and May as sentiment rebounded from coronavirus sell-off. That period has now given way to one of greater caution where buyers are more discerning about where they put their money.

One of those places is Indonesia. The nation’s local bonds have returned 22% this quarter in dollar terms, reversing the 17% decline from January to March, according to Bloomberg Barclays indexes. Indian securities have gained just 3.3% in the current quarter, following a 1.4% loss in the prior three months. Indonesia’s rupiah has rallied almost 15% since the start of April, while India’s rupee has lost 0.4%.

JPMorgan Asset already had an existing bias in favor of Indonesian bonds over Indian debt, and this was reinforced by the impact of the virus pandemic, Callegari said.

“The recession in India is likely to be deeper than in Indonesia and the fiscal deterioration larger,” he said. “Given India’s already larger debt and fiscal deficit and lower credit ratings, this contributes to our relative preference for Indonesian debt.”

| Key Metrics | Indonesia | India |

|---|---|---|

| Public debt as % of GDP (Source: DBS) | 36.9% | 74.3% |

| Monetary policy rate | 4.25% | 4% |

| Annual inflation rate | 2.2% (May) | 5.8% (March) |

| FX reserves | $130.5 billion (May) | $507.6 billion (June 12) |

| Foreign ownership in bonds | 30% | 1.8% |

Some investors still see value in both Indian and Indonesian bonds.

India’s high foreign-exchange reserves bode well for its bonds during times of risk aversion, while its efforts to gain inclusion in JPMorgan Chase & Co.’s global indexes will attract more investors, according to Emso Asset Management, a $5.5 billion asset management firm focused on emerging markets fixed income

“Indonesia has strong risk-on properties, whilst India has strong risk-off buffers,” said Shikeb Farooqui, a senior economist and macro strategist at Emso Asset in London. “It is encouraging that India is looking to diversify its investor base with JPMorgan index inclusion.”

Hit Harder

At the start of the pandemic crisis, Indonesian bonds fell further than India’s amid concern the Southeast Asian nation would be more vulnerable due to its reliance on foreign flows. With the Federal Reserve and other global central banks providing extraordinary support, the crisis has eased and the trend is now turning in favor of Indonesia.

Indonesia’s debt has attracted $1.1 billion of overseas funds this quarter, while India has lost $4.8 billion, according to data released by the two nations. Combined net withdrawals from both markets totaled $18.4 billion in the first quarter, data compiled by Bloomberg show.

BNP Paribas Asset said it’s hard to be positive about Indian bonds because a recovery in oil prices is likely to boost inflation. The South Asian nation relies on imports for about 80% of its crude requirements.

“We now think that real rates are more appealing in Indonesia,” said Jean-Charles Sambor, head of emerging-market debt in London at BNP Paribas Asset, which oversaw the equivalent of $457 billion at the end of March.

©2020 Bloomberg L.P.