IMF Urges Post-Pandemic Stimulus to Avoid Depression Mistake

A premature rollback in expansionary policies ended up prolonging the Great Depression in the 1930s.

(Bloomberg) -- The International Monetary Fund wants policy makers to avoid repeating the Depression-era mistake of ratcheting back budget deficits. Instead, it’s urging them to ramp up fiscal stimulus when the coronavirus contagion starts to abate.

“Once the recovery has happened and we are past the pandemic phase, for advanced economies it would be essential to undertake a broad-based stimulus,” IMF chief economist Gita Gopinath told reporters on Tuesday. “This would be even more effective if it were coordinated across all the advanced economies.”

That would mark a major break from the 1930s, when a premature rollback in expansionary policies ended up prolonging the Great Depression. It’s also quite a change for the IMF -- an institution that former U.S. Treasury Secretary Lawrence Summers once dubbed “It’s Mostly Fiscal” for its obsession with budget austerity.

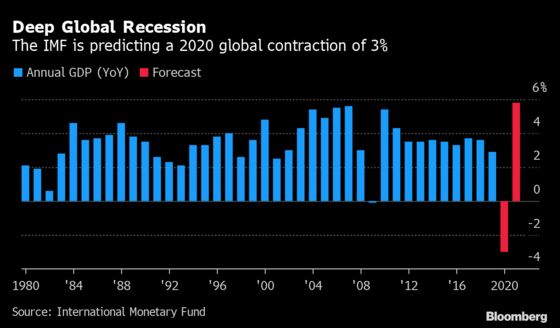

Such a strategy would help speed a global recovery from what the IMF predicts will be the deepest recession in almost a century this year as economic activity shuts down to contain the spread of the virus.

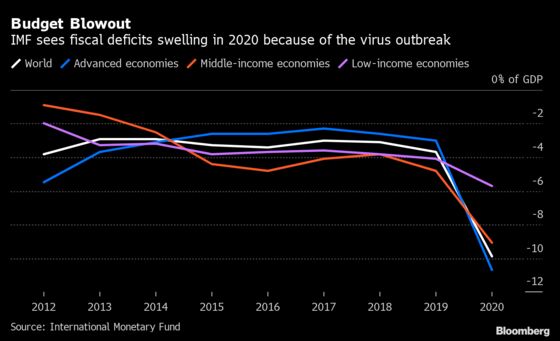

The IMF is expecting severe deterioration in global budget balances and public debt ratios based on spending to contain the health and economic impact of the pandemic, according to the fund’s semi-annual Fiscal Monitor report released on Wednesday.

Global fiscal deficits will more than double to 9.9% of gross domestic product this year from 3.7% in 2019, the fund said. Global debt will jump 13.1 percentage points to 96.4% of GDP, with the figure jumping to 122.4% of GDP in advanced economies from 105.2% in 2019, the IMF said.

The lending organization calculates that governments around the world have taken fiscal actions amounting to about $8 trillion, including more than $2 trillion in the U.S.

This has led to concern that major industrial nations are building up unsustainable levels of debt that will act as a drag on future growth, or even worse, sow the seeds of an eventual sovereign-debt crisis, unless concerted action is taken to reduce the red ink once recovery has begun.

Don’t Worry

Gopinath played down such worries. “As long as interest rates remain very low, as we’ve seen, and we get the recovery we’ve projected, then the combination should help in bringing debt levels down slowly over time.”

She also had some advice for central banks. While their decisions should be driven by the economic data, “if inflation stays well below target, interest rates should also stay low for that period of time.”

In downplaying deficit concerns, Gopinath is taking a page from one of her IMF predecessors, Olivier Blanchard, who argues that with interest rates low and likely to stay that way, government debt needn’t be a bogeyman for the world’s richest countries.

This doesn’t sound all that different from the prescription of Modern Monetary Theory proponents -– a heterodox economic school that contends countries such as the U.S. can run bigger budget shortfalls without worrying about going broke because they print their own money.

Budget Wrangle

U.S. lawmakers already are wrangling over another budget package, with Republicans pushing for a bare-bones program confined to topping up support for small businesses while Democrats press for something bigger.

No matter what they decide, however, the result is likely to be a plan designed to ensure the economy survives its near shutdown relatively intact, rather than to spur growth per se.

Such a package, possibly via stepped-up spending on infrastructure, may have to wait until after the November elections. “Our hunch is the next president will write the recovery package,” said Andy Laperriere, partner at Cornerstone Macro LLC.

After much wrangling, European Union finance ministers agreed last week on a 540 billion-euro ($593 billion) package of measures to combat the economic fallout of the coronavirus pandemic, including money for a joint employment program.

Kickstart Recovery

They also agreed to work on a temporary fund that would help kickstart the recovery and support the hardest-hit countries, while leaving open how it will be paid for. French Finance Minister Bruno Le Maire said a decision on the fund, which may total 500 billion euros, could come in the next six months.

Jacob Kirkegaard, a senior fellow at the Peterson Institute for International Economics in Washington, said there’s a good chance the EU will decide to earmark some money for public infrastructure to help promote an investment-led recovery.

Japan unveiled its own fiscal package last week, a record 108.2 trillion yen ($1 trillion) blueprint to shield the economy from the coronavirus’ widening. Much of it is targeted at stopping job and business losses after Prime Minister Shinzo Abe declared a state of emergency in the world’s third largest economy.

Once the virus is brought under control, a second phase of stimulus will aim to support a quick recovery, with steps to increase tourism and consumer spending along with subsidies for regional economies, according to a draft of the plan.

Some economists contend it isn’t necessary to hark all the way back to the 1930s to see the risks of prematurely tightening budgets. In the aftermath of the 2008-09 financial crisis, the U.S., Europe and Japan all moved to become more fiscally frugal -- hurting growth in the process.

“After the global financial crisis, they definitely took their foot off the accelerator and even began putting their foot on the brake from a fiscal-policy standpoint too quickly,” said Joseph Lupton, global economist at JPMorgan Chase & Co.

It’s that fixation on budget austerity that the IMF seemingly wants to avoid. As long as economies recover and interest rates stay low, “we should see these debt levels coming down,” Gopinath said.

©2020 Bloomberg L.P.