Italy at Risk: Massive Debt, Sluggish Growth Unnerve Investors

Huge Debt, Wary Investors Put Italy at Risk When Growth Falters

(Bloomberg) -- Italy’s failure to get its fiscal house in order may leave the economy prone to a major crisis when the next downturn rolls around.

The new populist administration has targeted next year’s budget deficit at 2.4 percent of output rather than lowering it as the European Union demanded. The spending gap may in turn add to the nation’s crushing debt burden, and investors responded negatively, sending stocks and bonds plunging.

The new target is “likely to put Italy’s debt-to-GDP ratio on an increasingly unstable equilibrium,” said Barclays senior European economist Fabio Fois in Milan. “The risks of the ratio taking an upward sloping path are non-negligible over the medium term.”

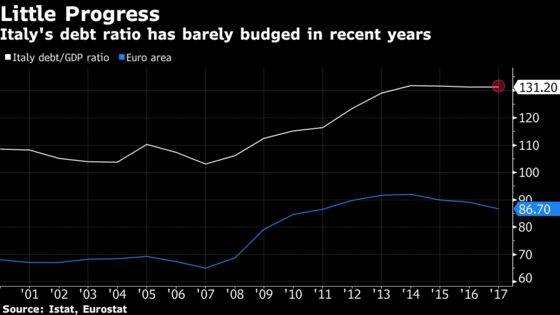

At more than 130 percent of GDP, the ratio remains the second-highest in the euro area after crisis-stricken Greece, and totals 2.3 trillion euros ($2.7 trillion) in absolute terms.

The pessimistic future scenario is simple. A slump in growth, along with higher interest costs, could seriously impair the government’s ability to pay off its obligations. Rising bond yields can also make it more difficult for Italian banks to sell their non-performing loans.

The expansion in Italy, and the wider euro area, has already cooled after 2017’s strong performance, and downside risks have increased, including an escalating U.S.-China trade battle, tighter monetary policy and emerging market turmoil.

Read more:

|

Matteo Salvini of the League and Luigi Di Maio of the Five Star Movement see things differently in the plan approved Thursday night in Rome.

The coalition leaders say the 2.4 percent 2019 deficit -- which may be penciled in for 2020 and the following year as well -- will help domestic demand, boosting the broader economy and trimming the debt ratio. Some economists agree there’ll be a short-term boost, with Commerzbank lifting its projection for growth next year.

Tria Focus

Much of the focus has been on Finance Minister Giovanni Tria, who reportedly had been seeking to hold the 2019 deficit to 1.6 percent of GDP but eventually yielded to populist pressure to raise it to 2.4 percent. During the weeks of tense negotiations, there were several news media reports saying he may have been ready to resign.

On Saturday, newspaper Il Messaggero said Tria was “embittered” by the budget process and may quit after the package is approved later this year. Tria has been seen by investors as a steadying influence over the populist leaders’ spending plans.

To further their point, the Italian populists can look to the austerity efforts of previous administrations. Those led to minimal results, with the public debt-to-GDP ratio barely moving lower since 2014.

‘Under Pressure’

But there are other implications to consider. While the government has yet to publish all details, Goldman Sachs said in an initial response that public debt “will be on a rising trajectory again.”

“Such an expansionary fiscal policy stance will put the Italian economy and Italian assets under pressure,” said strategist Silvia Ardagna.

Italy’s benchmark FTSE MIB stock index 3.7 percent on Friday. The yield on the country’s 10-year bonds rose 25 basis points to break through 3 percent again.

In the short term, Italy can probably work through any market turmoil, with the deficit under 3 percent -- the EU limit -- and the economy still growing. But the global economy looks past its best period, the current cycle is well advanced, and some say the next downturn isn’t very far away.

| What our economists say: “With the economy growing and inflation perking up, that’s still high enough to chip away at Italy’s huge stock of debt. However, the European Commission would like Italy to pay off the debt at a faster pace next year.” --David Powell, Bloomberg Economics,. Read the full INSIGHT |

For years Italy has been racking up primary surpluses -- the budget balance excluding interest on its debt. But those interest payments are a burden, and could worsen if investors continue to view the sovereign as a riskier prospect. The EU already predicts that Italy will have the slowest growth pace in the 19-nation euro area this year and next.

In the growth versus austerity debate, the government’s decision to lean on the former is no surprise given the pledges they made during this year’s election campaign to help the less well off and reduce the tax burden on some workers.

Investors have already made their view known, but all of this will also draw the attention of the European Commission.

“The commission and Italy’s partners would have been willing to make a gesture, to give the new government some leeway to implement some of its campaign promises,” said Isabelle Mateos y Lago at BlackRock Investment. But if its plans involve “breaking the rule book for the next three years in a massive way, and getting the debt on upward trajectory, that’s completely unacceptable.”

--With assistance from Giovanni Salzano.

To contact the reporter on this story: Lorenzo Totaro in Rome at ltotaro@bloomberg.net

To contact the editors responsible for this story: Fergal O'Brien at fobrien@bloomberg.net, Kevin Costelloe

©2018 Bloomberg L.P.