HSBC Manager Warns Extreme Bond Prices Are at Risk of Shock

HSBC Manager Warns Extreme Bond Prices Are at Risk of Shock

(Bloomberg) -- The record surge of investors into bonds increases the risk of a sudden sell-off that could reverberate across asset classes, according to HSBC’s $500 billion global asset management unit.

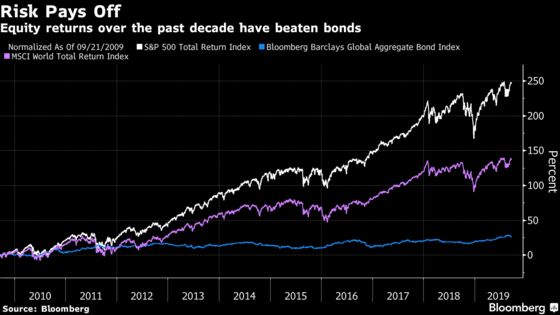

Instead of paying a “very high price” for negative returns in fixed income, Joseph Little, who helps run multi-asset teams at the U.K. firm, says clients should buy global equities. The economic pessimism priced into bonds is so high that even if the growth outlook improves modestly, the reversal in defensive assets could be dramatic, he said.

“The gap between equity and bond valuations is pretty extreme at the moment,” Little, the London-based global co-chief investment officer of multi-asset at HSBC Global Asset Management, said in a phone interview. “There’s an awful lot of bad news that is being currently reflected in the pricing today of long-term government bonds. It doesn’t take that much to really cause a bit of a shock to current pricing.”

Little isn’t alone in being worried about the excessive positioning in debt instruments and widespread risk aversion. Just last week, Goldman Sachs Private Wealth Management’s Sharmin Mossavar-Rahmani said it’s “remarkable” that geopolitical concerns have driven record inflows into bonds this year, while shunning equities. Even as the S&P 500 trades near a record high, positioning remains modest after traders pulled $198 billion from stock funds in 2019 amid late-cycle concerns that growth will falter.

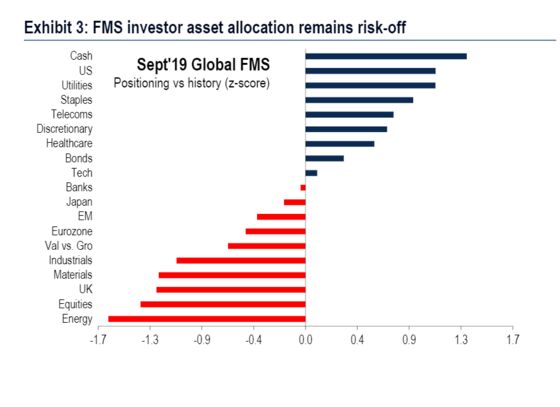

Investors are on high alert as U.S. and China trade talks continue and global growth shows signs of weakness. The latest Bank of America Corp. fund manager survey showed that they remain overweight safer assets, such as cash and bonds, and underweight equities.

At the same time, the $14-trillion pile of negative-yielding debt globally is growing and asset managers are being forced to become more bold and creative in procuring returns for their clients.

HSBC GAM’s multi-asset team favors cyclical and cheaper so-called value shares and steers away from longer-duration government bonds, such as German bunds, U.K. gilts and Japanese debt. But it doesn’t avoid fixed income completely and looks at shorter-term instruments in rates and credit, like Asian high-yield debt, Little said.

U.K. equities are another way for investors to access a high dividend yield and the pound’s weakness as well as low valuations make British assets “really quite attractive,” according to Little, whose team is overweight U.K. stocks despite the political risks. According to the BofA survey, the Brexit-torn nation’s equities are the most disliked globally.

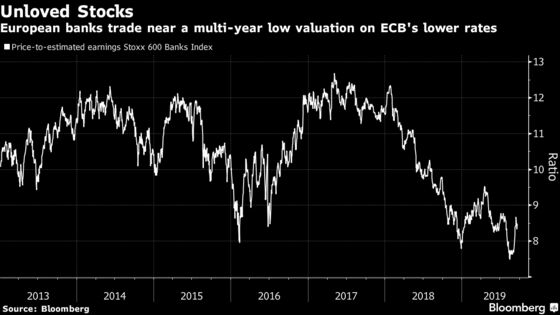

European banking stocks have also caught the attention of the co-chief investment officer, as they’ve been shunned by the market because of the European Central Bank’s easing measures. Little believes that the ECB needs to expand the money supply, increase liquidity and reduce the cost of equity in the banking sector to help resuscitate the European economy.

“If they do, then for the first time, you’ve got a combination of a monetary liquidity injection and cost of equity falling in European banks, and then there’s really good odds on a significant and sustained improvement in terms of European economic performance,” he said.

The risk of asset bubbles as a result of global quantitative easing isn’t keeping Little up at night because, he says, the central banks need to stop and turn around the slowdown in economic growth and corporate earnings.

However, a possible abrupt plunge in bonds could ricochet across various asset classes, he said.

“The principal risk for investors at the moment is a meaningful challenge to bond pricing at the longer part of the yield curve,” Little said. “If we were to see a significant sell-off in global bonds, driven by inflation concerns, driven by more fiscal easing, that potentially becomes a problem for how a whole range of asset classes are set in terms of pricing. But we aren’t really at that point yet."

--With assistance from Sid Verma.

To contact the reporter on this story: Ksenia Galouchko in London at kgalouchko1@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Jon Menon, John Viljoen

©2019 Bloomberg L.P.