(Bloomberg Opinion) -- China’s $12 trillion bond market is like a push-up bra – one wonders how much support there really is.

Corporate defaults have flared up again. China Minsheng Investment Group Corp., with interests in real estate and renewable energy, is the latest basket case. Coal miner Wintime Energy Co., one of China’s largest defaulters last year, missed interest payments again this month.

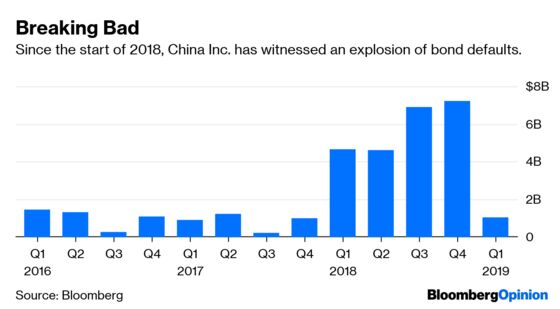

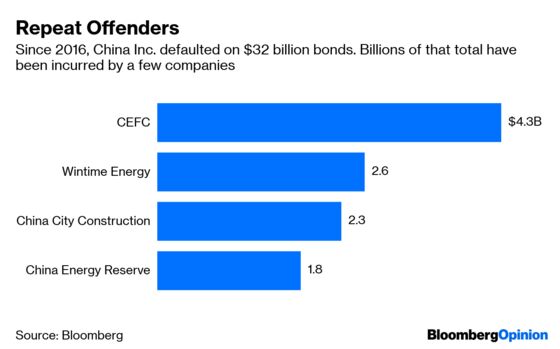

Are they just the tip of the iceberg? Since 2016, $32 billion worth of bonds have gone bad.

That number is far more benign than meets the eye though, because we’re witnessing a wave of repeat offenders. Energy trader CEFC China Energy Co. alone accounts for 13 percent of the total defaults, while Wintime follows with a 8 percent share.

I’m not saying China’s onshore bonds are safe. But when it comes to financial support, Beijing has a clear pecking order.

First, private firms are on their own. As my colleague Anjani Trivedi and I wrote recently, their financing conditions haven’t improved despite Beijing’s recent pledges to help tide them over. Companies such as Beijing Orient Landscape & Environment Co., an active player in China’s public-private partnership drive that rattled investors with a payment delay this month, are on their own.

Second, be wary of any investment conglomerate that has an ugly balance sheet but seemingly strong political ties. China Minsheng is the newest kid on the block. It’s now carrying out a firesale of assets to service short-term liabilities, even though some of its investors include member firms of the All-China Federation of Industry and Commerce, which operates under the auspices of the Communist Party.

We’ve seen cases of politically connected conglomerates unravel in recent years. I warned our readers in a 2017 column that CEFC was heading down the same path as HNA Group Co., even though the Shanghai-based energy trader looked flush then, boasting a 34 billion yuan ($4.7 billion) credit line from quasi-sovereign policy lender China Development Bank alone. In 2018, CEFC defaulted on over $4 billion of bonds.

There’s also China Energy Reserve & Chemicals Group Co., which courted state oil behemoth China National Petroleum Corp. as a key shareholder and is ultimately part-owned by the Communist Party itself. When China Energy Reserve became the controlling shareholder of the consortium that bought billionaire Li Ka-shing’s skyscraper The Center for a record $5.2 billion, I warned our readers about its investors – China City Construction Holding Group Co., its second-largest shareholder, was a serial defaulter. And sure enough, China Energy Reserve also went bad six months after the skyscraper splash.

With corporate debt mounting to 160 percent of GDP, Beijing can’t save everyone. As early as 2015, the government was already allowing some state-owned enterprises to default. So don’t pin false hopes on businesses that merely seem state-affiliated.

There’s one area that has been protected so far: municipal debt, including the off-balance-sheet variety. Last August, Xinjiang Production Construction 6th Shi State-Owned Asset Management Co. came close to being the first default among local government financing vehicles. But the firm managed to repay the bond only two days after its “technical” default: Just like Beijing Orient, the company blamed its missing payments on the clearing house’s operating hours.

There’s a good reason for this forbearance. With a fast-dwindling current account surplus, China may fall into twin deficits as soon as this year – a big no-no for global investors. The Ministry of Finance knows this, and is reluctant to increase its fiscal deficit. Instead, it demands infrastructure projects are financed by local governments by issuing bonds.

Last August, the Ministry of Finance set off a frenzy for municipal bonds by “guiding” that these notes need to pay coupons at least 40 basis points above sovereign issues of the same tenor, far higher than was hitherto the case. Banks and insurers rushed in, because under the current capital adequacy rules, municipals are considered as safe as sovereigns provided they offer a 36 basis-point spread.

Already, municipal debt paid for more than 80 percent of the incremental increase in infrastructure spending last year, up from only 5 percent in 2015. Issuance will only be higher this year. Beijing won’t want to kill a goose laying so many golden eggs, so deleveraging in this segment will only be pushed further out.

Normally, the interests of debt and equity investors are somewhat opposed. In China’s bond market, however, it’s a good idea for investors to align themselves with the majority shareholder – as long as it’s the Ministry of Finance.

To contact the editor responsible for this story: David Fickling at dfickling@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.