How Bank of Japan’s Massive Market Operations Make and Break Investors

How Bank of Japan’s Massive Market Operations Make and Break Investors

(Bloomberg) -- Just when it seemed impossible to do more, along came the coronavirus, spurring the Bank of Japan to double-down on its already massive market operations.

The BOJ’s presence is now felt in virtually every corner of Japan’s financial markets and its actions continue to shape global money flows. The first quarter of 2020 saw the central bank add a staggering 30 trillion yen ($278 billion) of bonds, stocks and other assets to its balance sheet, on top of which it pumped 35 trillion yen of liquidity into the financial system via operations such as repurchase agreements and dollar loans.

As the Topix index went into free-fall in March, the BOJ ratcheted up stock purchases to a record, helping arrest the plunge. And when funding markets started to seize last month, the monetary authority funneled hundreds of billions of dollars toward commercial banks.

Keeping up with these ever-expanding market operations -- and their impact -- is becoming increasingly important for investors. Here’s a rundown of what the BOJ is doing and how the measures affect markets.

Bonds Bully

Seven years of aggressive bond buying under Governor Haruhiko Kuroda has seen the BOJ suck up 47% of Japan’s sovereign debt as it fights to rekindle inflation. While the pace of purchases eased with yield-curve control in recent years, the central bank shifted up a gear again as the coronavirus outbreak cast a shadow over markets.

It shows no sign of abandoning a guideline to increase JGB holdings by 80 trillion yen a year, even though it added just under 16 trillion yen worth in 2019. Anchoring 10-year yields around zero has erased the market’s function for pricing risk and leaves banks, life insurers and pension funds with scant room to eke out returns to meet their liabilities.

Monthly purchase plans announced a day or two before they take effect tend to knock yields around when they contain unexpected changes in the size or frequency of buying, as do unscheduled operations.

There were 20 scheduled and 10 unscheduled operations in March, including two for inflation-indexed notes, as a rush for cash sparked selling of debt. The central bank also buys T-bills and floating-rate bonds.

Big Stick

The BOJ made sweeping changes to its April plan, giving itself more flexibility to buy debt maturing up to 10 years while allowing room for yields on longer-date bonds to steepen.

If all else fails, policy makers can whack yields back in line by offering to buy an unlimited amount of JGBs at fixed rates, a measure it has turned to on only eight occasions.

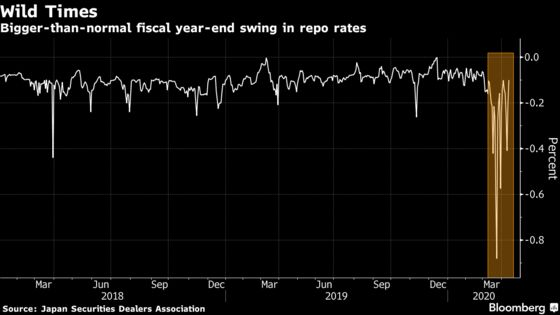

Repo Man

Having removed half of the country’s government bonds from the market through its buying, the BOJ has been forced to lend trillions of yen of debt securities back to financial companies through repurchase agreements.

It channeled 5.6 trillion yen of bonds to them last month amid sharp swings in the benchmark repo rate, which tumbled to a record minus 0.88%.

Ironically, it was the BOJ’s efforts in another part of the market that upended repo rates.

Doling Dollars

Through a foreign-exchange swap with the Federal Reserve, the BOJ lends billions of dollars at low rates to Japanese financial institutions, who typically offer up JGBs and blue-chip corporate debt as collateral.

The BOJ had $192 billion in swap borrowing outstanding as of April 9, the largest of any central bank, based on operations undertaken, according to Bloomberg calculations.

Last month as Japanese policy makers encouraged local banks to take up the Fed offer and stock up on dollars, it led to a scarcity of JGBs, sending repo rates on a wild ride.

The BOJ also offers huge amounts of collateralized yen loans. In March, supply totaled 2.11 trillion yen with an average term of 14 days.

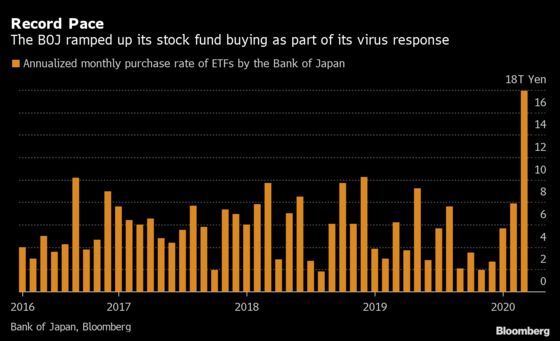

Stocks Savior

The BOJ in March doubled its annual target for buying exchange-traded funds of Japanese stocks to 12 trillion yen. It has also pledged to buy as much as 180 billion yen of Japanese real-estate investment trusts, helping to bolster the property market.

Purchases of ETFs and J-REITs touched 1.58 trillion yen in March, and analysts who closely watch the central bank’s purchase program expect it to maintain the pace until the Nikkei 225 Stock Average exceeds 20,000.

After losing almost a third of its value from a high in January, the Nikkei 225 has gained almost 19% since its March 19 low, closing Tuesday at 19,638.81.

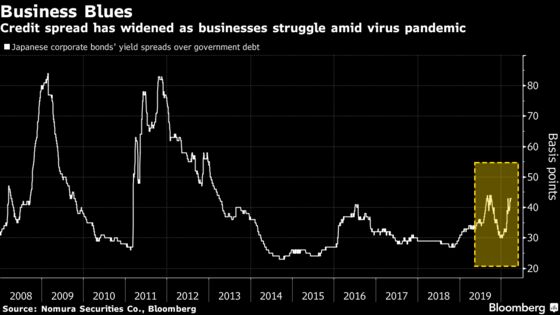

Corporate Debt

The BOJ also helps to shape the price of company debt and is ramping up buying through September to push its holdings of commercial paper to 3.2 trillion yen and corporate bonds to 4.2 trillion yen. It is doing this through monthly purchase plans similar to its JGB operations.

Yield premiums that Japanese corporate debt offer over government bonds, which have come down sharply from levels seen during the global financial crisis, are rising sharply again as the coronavirus hits business.

The BOJ’s decision to boost the upper limit of its corporate bond purchases shows its resolve to constrain the rise in spreads on these notes, and to reduce the risk of defaults by big companies, according to BNP Paribas SA.

That has encouraged companies that rarely sold short-term debt, including power companies and railway operators, to issue bonds as investors buy the notes to resell them to the BOJ.

Operations Recap

| Category | Frequency | Annual purchase target | Detail |

|---|---|---|---|

| JGBs | Scheduled / unscheduled. ~30 operations in March | 80t yen | Monthly plans are announced in advance. Unscheduled purchases can take place any time |

| ETF, J-REITs | Unscheduled. ~45 operations in March | 12t yen temporary buying pace for ETFs, 180b yen for J-REITS | No schedule is announced in advance. They tend to be conducted when equities drop |

| Corporate debt | Scheduled. One operation in March | N/A | BOJ aims to maintain holdings at 7.4t yen |

| Yen fund supply | Unscheduled. Four operations in March | N/A | Collateralized yen loans and selling of government debt with repurchase agreements |

| Dollar lending | Scheduled. ~13 operations in March | N/A | BOJ funnels to Japanese institutions collateralized loans of dollars provided by the Federal Reserve |

| Debt selling with repurchase agreements | Unscheduled. Six operations in March | N/A | Effectively short-term lending of Japanese government debt to ease market shortage of these securities |

©2020 Bloomberg L.P.