How the Savings Glut Still Sways U.S. Bonds

How the Savings Glut Still Sways U.S. Bonds

(Bloomberg) -- The “global saving glut” that former Federal Reserve Chairman Ben Bernanke famously blamed for depressing U.S. interest rates more than a decade ago hasn’t gone away. And if the appetite of Taiwanese investors is any guide, it’s here to stay.

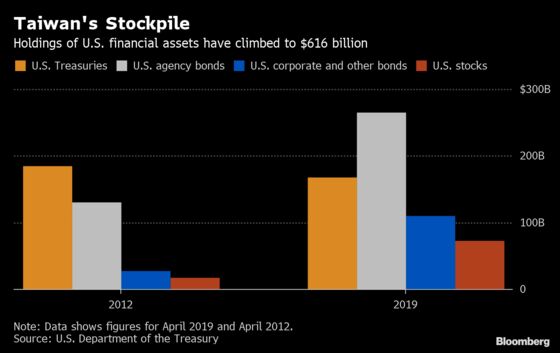

While its economy is smaller than that of New Jersey, Taiwan’s holdings of U.S. financial assets amount to the equivalent of all of the state and local government debt from New Jersey, California and Michigan combined. Put another way, Taiwan’s dollar portfolio -- $616 billion of stocks, bonds and credit in April -- exceeded all U.S. long-term securities held by Latin America.

This appetite for dollar assets spurred cycles of regulatory action and financial innovation:

- Taiwan capped the exposure that its insurance companies, with their $900 billion worth of assets, can run up overseas.

- When the insurers piled into foreign-currency bonds issued in Taiwan to get around those caps, they made that harder too.

- Finance being ever-inventive, local firms created exchange-traded funds denominated in Taiwan dollars but mostly made up of U.S. corporate bonds. And now they’ve become a huge hit with the insurers.

It’s easy enough to see why dollar assets are a big lure -- Taiwanese government bonds yield less than half the 2% on 10-year Treasury notes. And with a 20% savings rate in a wealthy and still-expanding economy, there’s more money that needs deploying each year. It’s a piece of the same puzzle that includes mega investors like Japan Post Bank Co. and Europeans pushed abroad by negative yields.

“Taiwanese and Japanese investors are just playing the game everyone plays,” said Michael Pettis, a professor of finance at the Guanghua School of Management at Peking University who has served as a financial consultant for governments in emerging markets. “Regulators will try to prevent them from taking on the kinds of risk that caused the last crisis, but inevitably they take on risk in new forms.”

As a Fed board member in 2005, Bernanke flagged how a lack of development of local financial markets had made savers less willing to deploy their money in some economies. That left them sending capital instead to places less in need of it, such as the U.S.

That irony continues to apply today.

Taiwan is on the doorstep of the biggest emerging market of them all -- mainland China -- and one that still needs plenty of capital to lift the living standards of hundreds of millions of rural poor. Political tensions between the two of course pose a hurdle, and regulators have a cap on Taiwanese insurers’ investments crossing the Taiwan Strait, at 10% of all foreign holdings.

There are broader reasons why China, despite its $14 trillion economy, isn’t more of a draw for global savings. Corporate governance standards and capital controls remain a concern, even as Chinese authorities move to address them and get domestic bonds and stocks included into benchmark global indexes.

“We’ll wait a very long time before China becomes a sustainable mop” for global savings, said Freya Beamish, chief Asia economist at research group Pantheon Macroeconomics Ltd. She pointed out that China for now is also focused on structural deleveraging, and unlikely to run the kind of current-account deficits that are the flip side of big capital inflows.

‘Unsustainable’ Situation

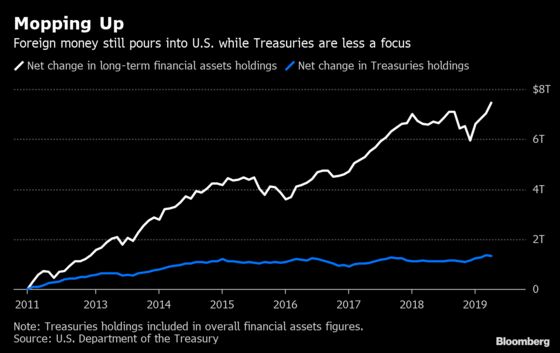

Part of the glut that Bernanke identified has crested. Back in 2005, China and other east Asian nations were ramping up their foreign-exchange reserve stockpiles, years after the late 1990s Asian financial crisis. That impetus has waned: the share of Treasuries held by overseas investors fell to about 36% as of March from 44% in late 2008, according to data compiled by Bloomberg.

“Increasingly, Treasury issuance has been absorbed by U.S. households,” David Adams, head of foreign-exchange research for North America at Morgan Stanley in New York, wrote in a July 25 note. Given the swelling federal borrowing requirement, “the U.S.’s ability to finance its deficits domestically as foreign investor participation has slowed appears unsustainable,” he concluded.

That would, net-net, send American yields higher. But Taiwanese insurers’ demand for American corporate bonds shows the foreign craving for U.S. assets remains, and may contribute to holding down U.S. borrowing costs.

Further evidence is seen in the voracious Japanese appetite for collateralized debt obligations, with Norinchukin Bank amassing some $68 billion, the bulk of which analysts regard to be in dollars. And considering how European and Japanese central bank policies have contributed to negative yields on their government bonds, it’s hard to see the bid for Treasuries fading.

“The ‘global savings glut’ has much evolved from the one described by Ben Bernanke, given key central banks’ overzealous actions,” said Jerome Jean Haegeli, chief economist at the Swiss Re Institute in Zurich, who previously served at the International Monetary Fund. “It’s hard to see in this context the attractiveness for Asian institutional investors on dollar assets weakening. For Europe, the case is even stronger.”

After he became chairman of the Fed in 2007, Bernanke returned to the saving-glut discussion. Toward the end of his speech came a perhaps underappreciated forecast:

It would take a “few decades” for the glut to dissipate.

--With assistance from Eric Lam and Miaojung Lin.

To contact the reporters on this story: Christopher Anstey in Tokyo at canstey@bloomberg.net;Enda Curran in Hong Kong at ecurran8@bloomberg.net;Cindy Wang in Taipei at hwang61@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Will Davies, Ravil Shirodkar

©2019 Bloomberg L.P.