How One or Two Stock Blowups Could Ruin Your Week: Taking Stock

How One or Two Stock Blowups Could Ruin Your Week: Taking Stock

(Bloomberg) -- Macro is clearly trumping micro at the moment. Apple’s uncharacteristic forecast cut could have had a devastating and lasting impact on the stock market, and probably would have if it were the only show in town.

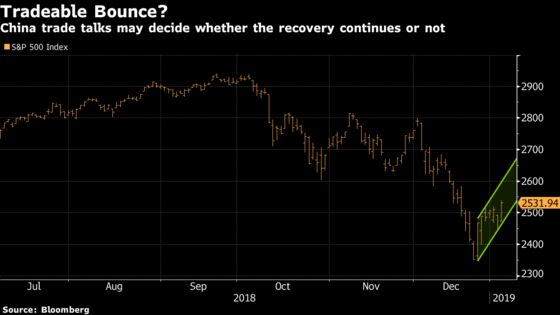

But Powell’s dovish tone from Friday, China’s central bank taking action to prop up their weakening economy, and optimism that a trade deal will get hammered out sooner than later is extending the sharp bounce that started in late December.

And so even with Apple’s punch to the gut, the major benchmark indices are all up anywhere from 7.5% to 8.8% since Christmas.

The top gainers in the S&P 500 within that time frame are below; notice that the list is littered with energy stocks, a couple of FAANGs (Netflix and Amazon), one semiconductor (Applied Materials), China-exposed gaming stocks, and the always exciting General Electric.

The Dec. 21 edition of Taking Stock focused on how Wall Streeters are "priming for a tradeable bounce," and man did they get one just days later. The Jan. 2 column warned about fakeout rallies in the beginning of the year, like we saw with General Electric in early 2018 (which looks to be playing out again in fine fashion this year). So are we in the midst of this tradeable bounce, and if so, when is the trade over?

Next Single-Stock Domino to Fall

The shutdown is an ugly shrugfest (steel barriers? national emergency? "months or even years"?) that could make a noticeable difference if it gets drawn out much longer, but the big wildcard that could change everything remains the U.S.-China trade negotiations, which are heating up as talks between both sides resume for the next two days.

If it starts to look like things aren’t progressing further than where we’ve been, I’d have to think that that recent momentum in equities stalled out. But that goes both ways, because if major ground is broken in these meetings that signifies a deal is on the cusp of being reached (a top Xi aide unexpectedly showing up should help that case), how does a fund that sees Apple as deeply undervalued not pull the trigger on for what could be a once in a lifetime buying opportunity?

Regardless, given the impact that the trade frictions have had on Apple and FedEx, I assume that added focus will be on the next single-stock domino to fall i.e. which company with relatively high exposure to China may cut their outlook with earnings or give cautious comments on the region at a conference.

Morgan Stanley chief U.S. equity strategist Michael Wilson, who was talking about a rolling bear market last year well before anyone else, talks about this micro risk in his update from this morning where he says there are still a few more hurdles to clear before we can blow the all clear signal:

"We need to get past some incrementally negative data points that we suspect are still lingering (the weak PMI and AAPL’s miss last week are unlikely isolated incidents) such that negative earnings revision breadth troughs. This last point means that risk is now highest at the single stock level and one must be particularly aware of valuation levels."

With that thinking, let’s take a look at which companies reporting earnings this week that might signal weakness from China operations: Tech names EXFO Inc. and SMART Global (both have almost 20% of revenues tied to Asia), lubricant seller WD-40 (~16% Asia-Pacific), hair dryer maker Helen of Troy (~5% Asia-Pacific), and steel company Commercial Metals (4.6% Asia), which is trading lower in the pre-market after just-released earnings.

There’s plenty of other China-exposed firms taking the stage at various sell-side events, like AMD at CES and ON Semi at Citi (China accounts for about one-third of total revenue for each firm), Intel at a JPMorgan tech forum (24% China), and Universal Display at Citi (Apple supplier with almost all of its sales out of Asia, though mostly South Korea).

Big Week for Healthcare

This is the week when the financial community tends to spend more time on healthcare stocks than probably any other time of the year.

The reason being the JPMorgan annual conference, which gets underway today in San Francisco. One of the biggest topics will no doubt be biotech M&A with the Celgene/Bristol-Myers $74 billion mega-deal fresh in everyone’s minds, and now Eli Lilly buying Loxo Oncology for $8 billion (a 68% premium to the Friday close) -- the IBB has almost doubled the S&P’s outstanding performance over the past seven sessions (up 14.4% vs up 7.7%, respectively) -- in addition to drug data, price increases, and gene editing.

Our industry reporters have done a ton of lead-up work to get everyone up to speed on what to expect at the event, so I’ll just drop a link to this spectacular tick-by-tick preview of which companies to watch and why.

Something New for Pot Investors

Volatility among pot stocks has quieted down over the past few weeks, relatively, though that should return this week with a number of catalysts.

The highlight will most likely be Aphria’s earnings on Friday. The company remains in the doghouse after an attack from the shorts last month, though the bears may be wincing a bit (shares are indicated up at the moment) after reading our weekend story that counters some of the claims by Quintessential Capital and Hindenburg Research.

Other actionable events over the next five days, from sell-side conferences to retail lotteries, are explored further in the inaugural edition of our weekly pot newsletter that is spearheaded by Toronto-based equities reporter Kristine Owram. The focus will be on the trader, like Taking Stock, but geared towards the cannabis companies, their share performance, and the investors who are either heavily involved or looking to dip their toe in.

The industry remains a polarizing one -- just look at this splashy Reefer Madness-esque WSJ op-ed from over the weekend, titled "Marijuana Is More Dangerous Than You Think: As legalization spreads, more Americans are becoming heavy users of cannabis, despite its links to violence and mental illness," or a feature in this week’s New Yorker written by "The Tipping Point" author Malcolm Gladwell titled, "Is Marijuana as Safe as We Think?: Permitting pot is one thing; promoting its use is another."

It’s also rife with noise and legislative misconceptions that may it hard to make a sound investment decision on a consistent basis, but we’re aiming to do our best to filter out what’s important, stay ahead of the curve in regards to actionable events, and be an arbiter of truth throughout the process.

If you like what you see or have any feedback on what we should be covering in the newsletter on a weekly basis, please feel free to drop us a line.

Your 63-Hour ICYMI

Here’s some stuff you might have missed since Friday’s close:

An NYT op-ed about impeaching the President ("The People vs Donald J. Trump") went viral over the weekend; a cartoon graphic of Jamie Dimon and Jeff Bezos arm wrestling graced the front page of a WSJ section this weekend attached to an article that dives into the "special relationship" between JPMorgan and Amazon; Barron’s had a feature on Ron Johnson ("The Inventor of the Apple Store on Retail Revolutions") and a Q&A with Muddy Waters’s Carson Block ("Blame the Bankers for Bad Corporate Behavior"); CNBC wrote a piece on how Salesforce’s Marc Benioff "unplugged for two weeks" and had a revelation that could change the tech industry; and here are your lines for next week’s NFL matchups: Chiefs favored by 6 over the Colts, Rams by a touchdown over the Cowboys, Pats by 4.5 over the Chargers, and the Saints by a whopping 9 over the Eagles.

Notes From the Sell Side

Goldman lowered its oil price deck for 2019, though sees current prices as undervalued at the moment. They expect Brent to average $62.50/bbl this year and WTI $55.50/bbl (currently ~$58.20 and ~$49, respectively). Equity analysts led by Brian Singer recommend "quality stocks on sale" like buy-rated Chevron, Phillips 66, Pioneer Natural, Diamondback Energy, and Kinder Morgan, while highlighting both Valero and CNX Resources as top sells.

Keybanc is out positive on the homebuilders and building product space, noting that the first half of 2019 is likely to mirror prior trading cycles when the builders surged 28% over six months on fed policy optimism. Previously cautious last year on rate hikes, the anlyasts are now doing a 180 and upgrading Lennar, PulteGroup, Masco, and Gibraltar Industries all to overweight.

Pivotal Research is making a bunch of rating changes ahead of tech earnings: Upgrading Alphabet, Salesforce, and Adobe all to buy; initiating Amazon with a buy (PT $1,920 is actually a couple hundred points below the Street average); and downgrading Snap to hold on valuation. A bear on Facebook for almost a couple years now, analyst Brian Wieser is holding tight and even cutting his target further to a Street low $113 ("downside risks on higher costs and management changes are more pronounced now vs. before, and revenue growth also faces risks").

And a couple of upgrades from BMO should make some noise: 1) Upgrading General Motors to an outperform on a brighter spotlight being placed on GM Cruise in 2019 and positive impacts from restructuring, and 2) Upgrading Micron to outperform as shares have likely bottomed out on valuation and FCF generation.

Tick-by-Tick Guide to Today’s Actionable Events

- Today -- U.S./China trade talks resume in Beijing

- Today -- UBS Greater China Conference (Jan. 7-11) kicks off in Shanghai

- 8:00am -- Schumer speaks at Association for Better New York event

- 10:00am -- ISM Non-Manufacturing, Factory Orders, Durable Goods

- 10:30am -- CELG at JPMorgan healthcare conference

- 11:00am -- CMC earnings call

- 11:30am -- PFE at JPMorgan healthcare conference

- 12:30pm -- TEVA, GILD at JPMorgan healthcare conference

- 12:40pm -- Fed’s Bostic speaks to Rotary Club of Atlanta

- 1:00pm -- GSK CEO Emma Walmsley on Bloomberg TV

- 1:40pm -- CNC CEO Michael Neidorff on Bloomberg TV

- 3:30pm -- JPM CEO Jamie Dimon keynote at JPMorgan healthcare conference

- 4:40pm -- AKAM CEO Tom Leighton on Bloomberg TV

- 5:00pm -- BHC, HUM at JPMorgan healthcare conference

- 5:30pm -- JNJ at JPMorgan healthcare conference

- 6:00pm -- XON investor meeting

- 6:30pm -- AGN, BIIB at JPMorgan healthcare conference

- 7:30pm -- Samsung earnings

- 7:30pm -- MRK at JPMorgan healthcare conference

- 8:00pm -- CFP National Championship: Clemson vs Alabama (-5.5)

To contact the reporter on this story: Arie Shapira in New York at ashapira3@bloomberg.net

To contact the editors responsible for this story: Chris Nagi at chrisnagi@bloomberg.net, Steven Fromm

©2019 Bloomberg L.P.